You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Backup Withholding - What Is It and How Can I Obtain A RefundDocument35 pagesBackup Withholding - What Is It and How Can I Obtain A RefundAyodeji Badaki100% (1)

- Financial Management and Financial ObjectivesDocument78 pagesFinancial Management and Financial Objectivesnico_777No ratings yet

- INTERNAL AUDIT OF STOCK BROKERSDocument75 pagesINTERNAL AUDIT OF STOCK BROKERSAnmol Kumar0% (1)

- Ratio AnalysisDocument51 pagesRatio AnalysisSeema RahulNo ratings yet

- I003Document3 pagesI003concast_pankajNo ratings yet

- Sharekhan Internship ProjectDocument74 pagesSharekhan Internship Projectayush goyalNo ratings yet

- Chap 022Document44 pagesChap 022jmsmartinsNo ratings yet

- Chapter-1 Basics of Risk ManagementDocument22 pagesChapter-1 Basics of Risk ManagementmmkattaNo ratings yet

- Investment Analysis and Portfolio Management OutlineDocument6 pagesInvestment Analysis and Portfolio Management OutlineHuan EnNo ratings yet

- Central Depository Company of PakistanDocument58 pagesCentral Depository Company of Pakistanmolvi001No ratings yet

- Crisil Report - OMT PDFDocument178 pagesCrisil Report - OMT PDFMarquis HowellNo ratings yet

- Royal Dutch Shell PLC Investor's Handbook 2010-2014: Consolidated Balance Sheet (At December 31)Document1 pageRoyal Dutch Shell PLC Investor's Handbook 2010-2014: Consolidated Balance Sheet (At December 31)Shara ValleserNo ratings yet

- Tax Issues in M A PDFDocument56 pagesTax Issues in M A PDFKhushboo GuptaNo ratings yet

- Interest Rate RiskDocument41 pagesInterest Rate RiskPardeep Ramesh AgarvalNo ratings yet

- 4 Property Plant Equipment Classification Acquisition Govt Grant and Borrowing CostDocument11 pages4 Property Plant Equipment Classification Acquisition Govt Grant and Borrowing CostElvie PepitoNo ratings yet

- Himachal Fertilizer Corporation A An Ethical ConundrumDocument7 pagesHimachal Fertilizer Corporation A An Ethical ConundrumAkash SampathNo ratings yet

- APPENDIX QuestionnaireDocument4 pagesAPPENDIX QuestionnaireNayab KhanNo ratings yet

- Topic - Week 2 Valuation of Bonds MCQDocument6 pagesTopic - Week 2 Valuation of Bonds MCQmail2manshaaNo ratings yet

- Revitalising BrandDocument23 pagesRevitalising Brandzakirno19248No ratings yet

- Yes Securities - Subscribe - TMBDocument28 pagesYes Securities - Subscribe - TMBRojalin SwainNo ratings yet

- SAP Financial Supply Chain ManagementDocument2 pagesSAP Financial Supply Chain ManagementSiber CKNo ratings yet

- Mutual Funds & UITFs in The PhilippinesDocument5 pagesMutual Funds & UITFs in The PhilippinesGeewee Vera FloresNo ratings yet

- Procedure for Initial Public Offering (IPODocument26 pagesProcedure for Initial Public Offering (IPOShweta GuptaNo ratings yet

- BHEL CFODocument3 pagesBHEL CFOShafeeq KadevalappilNo ratings yet

- Ir340 2020 PDFDocument168 pagesIr340 2020 PDFmaria_nikol_3No ratings yet

- Introduction To Financial Management FIN 254 (Assignment) Spring 2014 (Due On 24th April 10-11.00 AM) at Nac 955Document10 pagesIntroduction To Financial Management FIN 254 (Assignment) Spring 2014 (Due On 24th April 10-11.00 AM) at Nac 955Shelly SantiagoNo ratings yet

- Annual Report 2018-19 For Kalyani Steel Limited, HospetDocument155 pagesAnnual Report 2018-19 For Kalyani Steel Limited, Hospetsiddalinganagouda100% (1)

- Financial Accounting A Managerial PerspectiveDocument3 pagesFinancial Accounting A Managerial PerspectiveBir TajpuriyaNo ratings yet

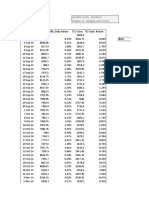

- Beta Calculation: Zerodha Varsity - Module 4 Chapter 11 - Hedging With FuturesDocument4 pagesBeta Calculation: Zerodha Varsity - Module 4 Chapter 11 - Hedging With FuturesPrathamesh NaikNo ratings yet