You might also like

- CRR & SLRDocument3 pagesCRR & SLRSwathy SidharthanNo ratings yet

- Cash Reserve Ratio (CRR) & Statutory Liquidity Ratio (SLR) Cash Reserve Ratio (CRR)Document4 pagesCash Reserve Ratio (CRR) & Statutory Liquidity Ratio (SLR) Cash Reserve Ratio (CRR)Sushil KumarNo ratings yet

- CRR-SLR - StudentsDocument4 pagesCRR-SLR - StudentsBabul YumkhamNo ratings yet

- CRR-SLR in BanksDocument25 pagesCRR-SLR in BanksPrashant GargNo ratings yet

- NDTLDocument13 pagesNDTLPradeep PoojariNo ratings yet

- Changes Made in Master Circular - Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR)Document4 pagesChanges Made in Master Circular - Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR)P'avan PatelNo ratings yet

- Fund Front Office: Definition: Cash Reserve Ratio (CRR) in Terms of Section 42 (1) of The Reserve Bank of India ActDocument17 pagesFund Front Office: Definition: Cash Reserve Ratio (CRR) in Terms of Section 42 (1) of The Reserve Bank of India ActSouravMalikNo ratings yet

- Master Circular - CRR and SLR - 2010Document24 pagesMaster Circular - CRR and SLR - 2010prathi05No ratings yet

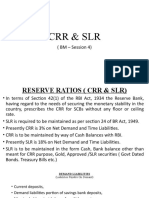

- Session. 4. CRR & SLRDocument15 pagesSession. 4. CRR & SLRArbazuddin shaikNo ratings yet

- Important Acts Revised CTFC 2 Nov 16Document44 pagesImportant Acts Revised CTFC 2 Nov 16Ankith BNo ratings yet

- Treasury Management in Banks - CAIIBDocument157 pagesTreasury Management in Banks - CAIIBAparnaBhattNo ratings yet

- SLR CRRDocument25 pagesSLR CRRSaketGiriNo ratings yet

- Commercial Banks and Their FunctionsDocument34 pagesCommercial Banks and Their Functionspash12345No ratings yet

- CRR SLRDocument25 pagesCRR SLRSamhitha KandlakuntaNo ratings yet

- AssignmentDocument13 pagesAssignmentMonir HossainNo ratings yet

- BFM Module C Chapter 18 Part IiDocument10 pagesBFM Module C Chapter 18 Part IifolinesNo ratings yet

- CRR - The Cash Reserve Ratio: SLR - Statutory Liquidity RatioDocument11 pagesCRR - The Cash Reserve Ratio: SLR - Statutory Liquidity RatioLovlesh RubyNo ratings yet

- CRR & SLRDocument17 pagesCRR & SLRParag Jain100% (1)

- Cash Reserve Ratio (CRR) : Computation of Demand and Time LiabilitiesDocument4 pagesCash Reserve Ratio (CRR) : Computation of Demand and Time LiabilitiesRitika JainNo ratings yet

- CRR-Analysis EcmDocument3 pagesCRR-Analysis Ecmrajeshre2No ratings yet

- RBI GUIDELINES ON Working CapitalDocument57 pagesRBI GUIDELINES ON Working Capitalashwini.krs80No ratings yet

- Jan 192014 Dos 01 eDocument11 pagesJan 192014 Dos 01 erakhalbanglaNo ratings yet

- Export Credit RefinancingDocument2 pagesExport Credit RefinancingSushantNo ratings yet

- Asset, Liability, Cash Reserves and Credit InfoDocument3 pagesAsset, Liability, Cash Reserves and Credit InfoPrachi GoelNo ratings yet

- MAY 5TH, 2018 Chandigarh: Presenter: CA Akesh VyasDocument109 pagesMAY 5TH, 2018 Chandigarh: Presenter: CA Akesh Vyassukumar basuNo ratings yet

- CRR, SLR: Dr.S.C.BihariDocument16 pagesCRR, SLR: Dr.S.C.BihariAbhi2636100% (1)

- Recollected Promotion Q 0ADocument13 pagesRecollected Promotion Q 0Akannan PNo ratings yet

- Sunita FA ProjectDocument10 pagesSunita FA ProjectsunitaNo ratings yet

- IIBF Vision September 2014 FINALDocument8 pagesIIBF Vision September 2014 FINALVinod YadavNo ratings yet

- Banking Report: Interbank Rates: Submitted byDocument12 pagesBanking Report: Interbank Rates: Submitted byAicha XaheerNo ratings yet

- External Commercial BorrowingDocument23 pagesExternal Commercial BorrowingAnshika SharmaNo ratings yet

- Laws Related To Banking in IndiaDocument48 pagesLaws Related To Banking in IndiaRohit Sharma75% (8)

- Takeover - Credit ReportDocument8 pagesTakeover - Credit ReportShantanuMogalNo ratings yet

- 3896IIBF Vision October 2014 15DPIDocument8 pages3896IIBF Vision October 2014 15DPIhvenkiNo ratings yet

- Master Circular On Interest Rates On FCNR (B) Deposits PurposeDocument11 pagesMaster Circular On Interest Rates On FCNR (B) Deposits PurposePradeep MehtaNo ratings yet

- OTS FORMULA Agri Loans Upto 25 Lacs Cir 481 2023 Mobile VersionDocument7 pagesOTS FORMULA Agri Loans Upto 25 Lacs Cir 481 2023 Mobile VersionDigbalaya SamantarayNo ratings yet

- 773531Document38 pages773531Mohammed Khaja MohinuddinNo ratings yet

- Quantitative ToolsDocument14 pagesQuantitative Tools9439223514pNo ratings yet

- Mob NpaDocument44 pagesMob NpaParthNo ratings yet

- FOREX Cir1684 12Document12 pagesFOREX Cir1684 12sunilNo ratings yet

- 22MCDocument63 pages22MCaspimpale1999No ratings yet

- Bill Market SchemesDocument2 pagesBill Market SchemesLeslie DsouzaNo ratings yet

- Guidelines For Compromise Settlement of Dues of Banks and Financial Institutions Through Lok AdalatsDocument3 pagesGuidelines For Compromise Settlement of Dues of Banks and Financial Institutions Through Lok AdalatsMahesh Prasad PandeyNo ratings yet

- Management of Advance by RBI 2005Document53 pagesManagement of Advance by RBI 2005Ramkumar SankerNo ratings yet

- Example of CRR and SLRDocument5 pagesExample of CRR and SLRNagaratnam ChandrasekaranNo ratings yet

- Review Investment PolicyDocument33 pagesReview Investment PolicyRupesh MoreNo ratings yet

- CDR ArticleDocument2 pagesCDR ArticleStuti NayakNo ratings yet

- Guidelines On Asset-Liability Management (ALM) System - AmendmentsDocument8 pagesGuidelines On Asset-Liability Management (ALM) System - AmendmentstorjhaNo ratings yet

- Study Material - Banking & Finance (May-2011)Document4 pagesStudy Material - Banking & Finance (May-2011)AKS_RSNo ratings yet

- Customers' Deposit Accounts: Unit IVDocument26 pagesCustomers' Deposit Accounts: Unit IVShaifaliChauhanNo ratings yet

- 1st Issue E-Gyan, July-2013Document13 pages1st Issue E-Gyan, July-2013mevrick_guyNo ratings yet

- 92MRCD010710 F3Document27 pages92MRCD010710 F3Neelam PatilNo ratings yet

- Master Circular - Bank Finance To Non-Banking Financial Companies (NBFCS)Document10 pagesMaster Circular - Bank Finance To Non-Banking Financial Companies (NBFCS)yogendrachat4057No ratings yet

- RBI Master CircularDocument42 pagesRBI Master CircularDeep Singh PariharNo ratings yet

- CCP Rbi Jul-Dec'23Document21 pagesCCP Rbi Jul-Dec'23RaviTuduNo ratings yet

- Eco by PankajDocument59 pagesEco by PankajShivani SinghNo ratings yet

- Banking Regulations Act, RBI Act, Ni ActDocument65 pagesBanking Regulations Act, RBI Act, Ni ActDeepak GuptaNo ratings yet

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Fundamental Analysis of Banking Industry: Interim Report ONDocument29 pagesFundamental Analysis of Banking Industry: Interim Report ONBalpreet KaurNo ratings yet

- The Leveraged Buyout Deal of TataDocument3 pagesThe Leveraged Buyout Deal of TataBalpreet KaurNo ratings yet

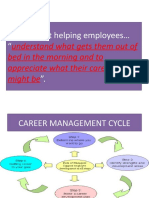

- CM Is About Helping Employees "Document6 pagesCM Is About Helping Employees "Balpreet KaurNo ratings yet

- Perfect Competetion in Laundry MarketDocument26 pagesPerfect Competetion in Laundry MarketBalpreet KaurNo ratings yet

- Kara Smith Resume FinalDocument3 pagesKara Smith Resume Finalapi-396378090No ratings yet

- PWC Top Health Industry Issues of 2014Document17 pagesPWC Top Health Industry Issues of 2014daveawoodsNo ratings yet

- ZONE 12 - Super Markets & GroceryDocument1 pageZONE 12 - Super Markets & GroceryDeepak Saravanan100% (1)

- ICS Form 205Document2 pagesICS Form 205Josanne Wadwadan De Castro100% (1)

- Inventory Control (PPIC)Document15 pagesInventory Control (PPIC)exsiensetyoprini100% (1)

- Hytera-BDA-Brochure 230624 173508Document16 pagesHytera-BDA-Brochure 230624 173508mikeNo ratings yet

- Assignment No 4 - L&S.C. ManagementDocument5 pagesAssignment No 4 - L&S.C. ManagementAhmed E-habNo ratings yet

- LA Metro - 550Document4 pagesLA Metro - 550cartographica100% (2)

- Unit 2 - Sbaa7001 Banking Products and ServicesDocument38 pagesUnit 2 - Sbaa7001 Banking Products and ServicesGracyNo ratings yet

- 2Document2 pages2satheshNo ratings yet

- ASHOKDocument3 pagesASHOKSonu the devotional boyNo ratings yet

- Test PDF 1Document124 pagesTest PDF 1eltsipe100% (1)

- Hitron Modem ManualDocument2 pagesHitron Modem ManualHugo FrancoNo ratings yet

- Answer 2Document5 pagesAnswer 2Yohannes bekeleNo ratings yet

- Project Scope Statement - For A Metro ProjectDocument2 pagesProject Scope Statement - For A Metro ProjectAnindo Chakraborty60% (5)

- Break Even AnalysisDocument2 pagesBreak Even AnalysisYugal Subba YugNo ratings yet

- HardikDocument28 pagesHardikKeyur PatelNo ratings yet

- Outbound Clicks - Pinterest Analytics Overview 20220601-20220626Document3 pagesOutbound Clicks - Pinterest Analytics Overview 20220601-20220626igor.zampolloNo ratings yet

- Family Practice Brochure With TweaksDocument2 pagesFamily Practice Brochure With Tweaksapi-355843078No ratings yet

- Bacc101 Fin Acc Aass 2Document2 pagesBacc101 Fin Acc Aass 2PETRONELLANo ratings yet

- Refresher Module in Freight TransactionsDocument4 pagesRefresher Module in Freight TransactionsPoy GuintoNo ratings yet

- European Distribution and Supply Chain Logistics PDFDocument2 pagesEuropean Distribution and Supply Chain Logistics PDFCharlesNo ratings yet

- Delivering Cloud-Based Solutions For Hospitals, Physicians, Clinics, Patients, and PopulationDocument4 pagesDelivering Cloud-Based Solutions For Hospitals, Physicians, Clinics, Patients, and PopulationsomyaNo ratings yet

- Case StudyDocument6 pagesCase StudyAndrea Romero100% (2)

- The Impact of Pandemic On Digital Payments in India: February 2021Document12 pagesThe Impact of Pandemic On Digital Payments in India: February 2021ShameerNo ratings yet

- Ibs Tangkak 1 31/03/22Document2 pagesIbs Tangkak 1 31/03/22NABIL HAKIMNo ratings yet

- Alternate Revenue Sources Bank IDBI BankDocument35 pagesAlternate Revenue Sources Bank IDBI Bankalkanm75060% (5)

- Early Ipv6 Deployment in A Global Network: Was It Worth The Effort?Document25 pagesEarly Ipv6 Deployment in A Global Network: Was It Worth The Effort?Carlos Andres Pulgarin GomezNo ratings yet

- Apple Pay Payment Method GuideDocument4 pagesApple Pay Payment Method GuideMahadevan VenkatesanNo ratings yet

- Account Number 204250801 Service Address 216 Hardwood TrailDocument2 pagesAccount Number 204250801 Service Address 216 Hardwood TrailLeeNo ratings yet