You might also like

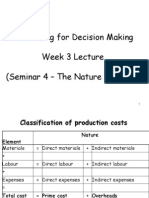

- Accounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)Document51 pagesAccounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)nwcbenny337No ratings yet

- LT 6 - 7 National Culture and The Values of Organizational Employees - A Dimensional Analysis Across 43 NationsDocument35 pagesLT 6 - 7 National Culture and The Values of Organizational Employees - A Dimensional Analysis Across 43 Nationsnwcbenny337No ratings yet

- LT5 A Cross-Cultural Assessment of Attitudes of Business Students Toward Business Thics A Comparison of China and The USADocument15 pagesLT5 A Cross-Cultural Assessment of Attitudes of Business Students Toward Business Thics A Comparison of China and The USAnwcbenny337No ratings yet

- LT5 A Chinese-United States Joint Venture Business Ethics Model and Its Implications For Multi-National FirmsDocument9 pagesLT5 A Chinese-United States Joint Venture Business Ethics Model and Its Implications For Multi-National Firmsnwcbenny337No ratings yet

- Accounting For Decisiom Making Week 4 Lecture (Seminar 5 - Calculating The Unit Cost and Pricing The Product or Service)Document38 pagesAccounting For Decisiom Making Week 4 Lecture (Seminar 5 - Calculating The Unit Cost and Pricing The Product or Service)nwcbenny337No ratings yet

- AFD W5 Lecture Power PointDocument64 pagesAFD W5 Lecture Power Pointnwcbenny337No ratings yet

- AFD W6 Lecture Power PointDocument35 pagesAFD W6 Lecture Power Pointnwcbenny337No ratings yet

- W1 Lecture Power PointDocument30 pagesW1 Lecture Power Pointnwcbenny337No ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Grade 11 Test On AdjustmentsDocument6 pagesGrade 11 Test On AdjustmentsENKK 25No ratings yet

- Suon Bai S WDocument1 pageSuon Bai S WNgoc ThanhNo ratings yet

- Swift C Sharp PosterDocument1 pageSwift C Sharp PosterJoshua Shalom Cherkes100% (1)

- Salerno TEACHING SOCIAL SKILLS Jan 2017Document86 pagesSalerno TEACHING SOCIAL SKILLS Jan 2017LoneWolfXelNo ratings yet

- 19-20 Math Section A1 Answer KeyDocument5 pages19-20 Math Section A1 Answer KeyChad Aristo CHIMNo ratings yet

- Is 3427-1997 (Iec 298-1990) - Switch Gear &contrl GearDocument68 pagesIs 3427-1997 (Iec 298-1990) - Switch Gear &contrl Gearjerinmathew2220No ratings yet

- Student Pain Management Fundamental ReasoningDocument7 pagesStudent Pain Management Fundamental ReasoningSharon TanveerNo ratings yet

- Basic Probability Part 6 PDFDocument7 pagesBasic Probability Part 6 PDFboss BossNo ratings yet

- Castle Leasing Corporation Which Uses Ifrs Signs A Lease Agreement PDFDocument1 pageCastle Leasing Corporation Which Uses Ifrs Signs A Lease Agreement PDFFreelance WorkerNo ratings yet

- Animal ProjectDocument1 pageAnimal Projectapi-377110324No ratings yet

- Risk Assessment Garage 1Document2 pagesRisk Assessment Garage 1api-246928698No ratings yet

- BEA 242 Introduction To Econometrics Group Assignment (Updated On 10 May 2012: The Change in Highlighted)Document4 pagesBEA 242 Introduction To Econometrics Group Assignment (Updated On 10 May 2012: The Change in Highlighted)Reza Riantono SukarnoNo ratings yet

- Sports Management Masters Thesis TopicsDocument7 pagesSports Management Masters Thesis Topicsaflnwcaabxpscu100% (2)

- Social Issues and The EnvironmentDocument8 pagesSocial Issues and The EnvironmentRahul100% (6)

- Curriculum Vitae Jivan Govind Tidake: Career ObjectiveDocument2 pagesCurriculum Vitae Jivan Govind Tidake: Career Objectivejivan tidakeNo ratings yet

- Anthony Giddens Sociology 6 TH Anthony Giddens Sociology 6 TH Editionpdf FreeDocument2 pagesAnthony Giddens Sociology 6 TH Anthony Giddens Sociology 6 TH Editionpdf FreeAnushree AyanavaNo ratings yet

- Hul Wacc PDFDocument1 pageHul Wacc PDFutkNo ratings yet

- 3 CD Rom Microscope MaintenanceDocument26 pages3 CD Rom Microscope MaintenanceJosé EstradaNo ratings yet

- Student Assignment Analyzes Statistics ProblemsDocument2 pagesStudent Assignment Analyzes Statistics ProblemsKuberanNo ratings yet

- Finite Element Modelling and Simulation of Gun Dynamics Using ANSYS'Document5 pagesFinite Element Modelling and Simulation of Gun Dynamics Using ANSYS'Yousaf SaidalaviNo ratings yet

- 03 Silenziatori PVT-HELIX-S EN-Rev.08Document16 pages03 Silenziatori PVT-HELIX-S EN-Rev.08alNo ratings yet

- Adpie LecturioDocument5 pagesAdpie LecturioPauline PascuaDNo ratings yet

- The Tamil Nadu Dr. M.G.R. Medical University - MSC Nursing Second YrDocument10 pagesThe Tamil Nadu Dr. M.G.R. Medical University - MSC Nursing Second YrNoufal100% (1)

- RM Question and AnswerDocument19 pagesRM Question and AnswerPadmavathiNo ratings yet

- Perma (Permanent) Culture: The Prime Directive of PermacultureDocument13 pagesPerma (Permanent) Culture: The Prime Directive of Permaculturebulut83No ratings yet

- Metro Service Schedule InsightsDocument16 pagesMetro Service Schedule InsightsAtul KumarNo ratings yet

- CraneDocument27 pagesCranemsk7182No ratings yet

- Benny Lim Kian Heng ResumeDocument3 pagesBenny Lim Kian Heng ResumeMichael MyintNo ratings yet

- Measures to Control Inflation in IndiaDocument9 pagesMeasures to Control Inflation in IndiaLangalia KandarpNo ratings yet

- The CoverDocument1 pageThe CoverRichard RaquelNo ratings yet