You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- LT5 A Chinese-United States Joint Venture Business Ethics Model and Its Implications For Multi-National FirmsDocument9 pagesLT5 A Chinese-United States Joint Venture Business Ethics Model and Its Implications For Multi-National Firmsnwcbenny337No ratings yet

- 220hp Caterpillar 3306 Gardner Denver SSP Screw Compressor DrawingsDocument34 pages220hp Caterpillar 3306 Gardner Denver SSP Screw Compressor DrawingsJVMNo ratings yet

- SSP 465 12l 3 Cylinder Tdi Engine With Common Rail Fuel Injection SystemDocument56 pagesSSP 465 12l 3 Cylinder Tdi Engine With Common Rail Fuel Injection SystemJose Ramón Orenes ClementeNo ratings yet

- LT 6 - 7 National Culture and The Values of Organizational Employees - A Dimensional Analysis Across 43 NationsDocument35 pagesLT 6 - 7 National Culture and The Values of Organizational Employees - A Dimensional Analysis Across 43 Nationsnwcbenny337No ratings yet

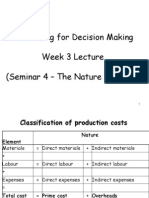

- Accounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)Document51 pagesAccounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)nwcbenny337No ratings yet

- Accounting For Decisiom Making Week 4 Lecture (Seminar 5 - Calculating The Unit Cost and Pricing The Product or Service)Document38 pagesAccounting For Decisiom Making Week 4 Lecture (Seminar 5 - Calculating The Unit Cost and Pricing The Product or Service)nwcbenny337No ratings yet

- Probni Test 1. Godina - Ina KlipaDocument4 pagesProbni Test 1. Godina - Ina KlipaMickoNo ratings yet

- L Addison Diehl-IT Training ModelDocument1 pageL Addison Diehl-IT Training ModelL_Addison_DiehlNo ratings yet

- Rajivgandhi University of Health Sciences Bangalore, KarnatakaDocument19 pagesRajivgandhi University of Health Sciences Bangalore, KarnatakaHUSSAINA BANONo ratings yet

- Case Report 3 MukokelDocument3 pagesCase Report 3 MukokelWidychii GadiestchhetyaNo ratings yet

- Careerride Com Electrical Engineering Interview Questions AsDocument21 pagesCareerride Com Electrical Engineering Interview Questions AsAbhayRajSinghNo ratings yet

- Onuaguluchi1996 1Document10 pagesOnuaguluchi1996 1IkaSugihartatikNo ratings yet

- Tiếng AnhDocument250 pagesTiếng AnhĐinh TrangNo ratings yet

- Biology 1st Term PaperDocument2 pagesBiology 1st Term PapershrirahulambadkarNo ratings yet

- Complaint: Employment Sexual Harassment Discrimination Against Omnicom & DDB NYDocument38 pagesComplaint: Employment Sexual Harassment Discrimination Against Omnicom & DDB NYscl1116953No ratings yet

- 4EVC800802-LFEN DCwallbox 5 19Document2 pages4EVC800802-LFEN DCwallbox 5 19michael esoNo ratings yet

- Desigo PX SeriesDocument10 pagesDesigo PX SeriestemamNo ratings yet

- OKRA Standards For UKDocument8 pagesOKRA Standards For UKabc111007100% (2)

- What Has The Government and The Department of Health Done To Address To The Issues of Reproductive and Sexual Health?Document5 pagesWhat Has The Government and The Department of Health Done To Address To The Issues of Reproductive and Sexual Health?Rica machells DaydaNo ratings yet

- 21A Solenoid Valves Series DatasheetDocument40 pages21A Solenoid Valves Series Datasheetportusan2000No ratings yet

- OM Hospital NEFTDocument1 pageOM Hospital NEFTMahendra DahiyaNo ratings yet

- Hamraki Rag April 2010 IssueDocument20 pagesHamraki Rag April 2010 IssueHamraki RagNo ratings yet

- White Vaseline: Safety Data SheetDocument9 pagesWhite Vaseline: Safety Data SheetHilmi FauziNo ratings yet

- BR Interlock Pallet Racking System 2009 enDocument8 pagesBR Interlock Pallet Racking System 2009 enMalik Rehan SyedNo ratings yet

- Prof. Madhavan - Ancient Wisdom of HealthDocument25 pagesProf. Madhavan - Ancient Wisdom of HealthProf. Madhavan100% (2)

- Biomedical Admissions Test 4500/12: Section 2 Scientific Knowledge and ApplicationsDocument20 pagesBiomedical Admissions Test 4500/12: Section 2 Scientific Knowledge and Applicationshirajavaid246No ratings yet

- Building and Environment: Nabeel Ahmed Khan, Bishwajit BhattacharjeeDocument19 pagesBuilding and Environment: Nabeel Ahmed Khan, Bishwajit Bhattacharjeemercyella prasetyaNo ratings yet

- Hospital - Data Collection & Literature StudyDocument42 pagesHospital - Data Collection & Literature StudyNagateja MallelaNo ratings yet

- Glycolysis Krebscycle Practice Questions SCDocument2 pagesGlycolysis Krebscycle Practice Questions SCapi-323720899No ratings yet

- Figure 1: Basic Design of Fluidized-Bed ReactorDocument3 pagesFigure 1: Basic Design of Fluidized-Bed ReactorElany Whishaw0% (1)

- Butt Weld Cap Dimension - Penn MachineDocument1 pageButt Weld Cap Dimension - Penn MachineEHT pipeNo ratings yet

- Đề ANH chuyên 5Document7 pagesĐề ANH chuyên 5Phạm Ngô Hiền MaiNo ratings yet

- General Session Two - Work Life BalanceDocument35 pagesGeneral Session Two - Work Life BalanceHiba AfandiNo ratings yet

- G.R. No. 178741Document1 pageG.R. No. 178741Jefferson BagadiongNo ratings yet