You might also like

- How to Handle Goods and Service Tax (GST)From EverandHow to Handle Goods and Service Tax (GST)Rating: 4.5 out of 5 stars4.5/5 (4)

- GST in India - An IntroductionDocument96 pagesGST in India - An Introductionkinnar2013No ratings yet

- GST Implication 17Document14 pagesGST Implication 17Priyadarshan KrishnaNo ratings yet

- GST MSOP Project FinalDocument19 pagesGST MSOP Project FinalAnjli SampatNo ratings yet

- Goods & Services Act FinalDocument78 pagesGoods & Services Act FinalParvesh AghiNo ratings yet

- Agt GSTDocument28 pagesAgt GSTAmit GuptaNo ratings yet

- Calender of EventsDocument89 pagesCalender of EventsShankar ReddyNo ratings yet

- GST Ebook sk-1Document89 pagesGST Ebook sk-1KunalKumarNo ratings yet

- GST in India: An overview of the Goods and Services TaxDocument57 pagesGST in India: An overview of the Goods and Services Taxmurali140No ratings yet

- GST Oct 17Document23 pagesGST Oct 17himanNo ratings yet

- PHD Research Bureau PHD Chamber of Commerce and IndustryDocument33 pagesPHD Research Bureau PHD Chamber of Commerce and IndustrySUNIL PUJARINo ratings yet

- GST Unit 1 ADocument39 pagesGST Unit 1 AMukul BhatnagarNo ratings yet

- GST - PersonalDocument62 pagesGST - PersonalSri NiNo ratings yet

- Overview GSTDocument56 pagesOverview GSTrahulNo ratings yet

- GST PPT June19Document65 pagesGST PPT June19yash bhushanNo ratings yet

- (Goods and Services Tax) : by Hirak ParmarDocument36 pages(Goods and Services Tax) : by Hirak ParmarSUDHIRNo ratings yet

- Goods and Services Tax (GST) in IndiaDocument30 pagesGoods and Services Tax (GST) in IndiarupalNo ratings yet

- Basics of GSTDocument40 pagesBasics of GSTsportnik.in100% (1)

- Goods and Services Tax (GST) : Simplified byDocument14 pagesGoods and Services Tax (GST) : Simplified bypushpendra singh sodhaNo ratings yet

- GSTDocument42 pagesGSTSwarga Santosh Mohanty100% (1)

- GST BasicsDocument56 pagesGST BasicsrahulNo ratings yet

- Gstcomplete 150201015617 Conversion Gate02 PDFDocument23 pagesGstcomplete 150201015617 Conversion Gate02 PDFShahinsha HcuNo ratings yet

- (Goods and Services Tax) : Biggest Tax Reform Since Independence .Document23 pages(Goods and Services Tax) : Biggest Tax Reform Since Independence .Pranav ChandranNo ratings yet

- CS Exe GST New PDFDocument238 pagesCS Exe GST New PDFArundhati PawarNo ratings yet

- (Goods and Services Tax) : Biggest Tax Reform Since Independence .Document80 pages(Goods and Services Tax) : Biggest Tax Reform Since Independence .isha patilNo ratings yet

- Ghanshyam 1813 PPT Public FinanceDocument64 pagesGhanshyam 1813 PPT Public FinanceShivansh JhaNo ratings yet

- Issues and Challanges of GSTDocument20 pagesIssues and Challanges of GSTshaik nazneenNo ratings yet

- Goods and Services Tax - 2021Document43 pagesGoods and Services Tax - 2021gsvighneshnairNo ratings yet

- Goods and Service TaxDocument35 pagesGoods and Service Taxaditya2110No ratings yet

- Goods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLADocument30 pagesGoods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLAKrishna ShuklaNo ratings yet

- Screenshot 2023-11-07 at 11.04.39 AMDocument18 pagesScreenshot 2023-11-07 at 11.04.39 AMrohit jainNo ratings yet

- Ca Inter GST Question Bank 1 1 PDFDocument63 pagesCa Inter GST Question Bank 1 1 PDFTreesa DevasiaNo ratings yet

- GST FrameworkDocument21 pagesGST FrameworkExecutive EngineerNo ratings yet

- Indirect Taxes: Assignment-2Document27 pagesIndirect Taxes: Assignment-2Arpita ArtaniNo ratings yet

- Goods and Services Tax (GST) in India: Ca R.K.BhallaDocument27 pagesGoods and Services Tax (GST) in India: Ca R.K.BhallaAditya V v s r kNo ratings yet

- 1 GST-OverviewDocument60 pages1 GST-OverviewAccounts - ParallaxNo ratings yet

- Goods and Service Tax (GST) : Biggest Indirect Tax Reform in IndiaDocument26 pagesGoods and Service Tax (GST) : Biggest Indirect Tax Reform in Indiafal_engNo ratings yet

- Role of CS in GSTDocument66 pagesRole of CS in GSThareshmsNo ratings yet

- Overview of GST Model GST Law Meaning Scope of SupplyDocument47 pagesOverview of GST Model GST Law Meaning Scope of SupplyShubham More CenationNo ratings yet

- Prof. Ashish R. Chourasiya: Goods & Service Tax: IntroductionDocument36 pagesProf. Ashish R. Chourasiya: Goods & Service Tax: IntroductionAJAY PHENOMNo ratings yet

- Sip 3 CH AsmaDocument20 pagesSip 3 CH AsmaAsma KhanNo ratings yet

- PC Chart Book + Revision Videos On Youtube Guaranteed SuccessDocument48 pagesPC Chart Book + Revision Videos On Youtube Guaranteed SuccessPallab BaruahNo ratings yet

- Goods and Services Tax (GST) in India: CA. Preeti GoyalDocument30 pagesGoods and Services Tax (GST) in India: CA. Preeti GoyalArvind PalNo ratings yet

- Indirect Tax Notes-CS Exe-June 23 1 Lyst1731Document145 pagesIndirect Tax Notes-CS Exe-June 23 1 Lyst1731tskpestsolutions.chennaiNo ratings yet

- SIP 123 AsmaDocument20 pagesSIP 123 AsmaAsma KhanNo ratings yet

- Revised Model GST LawDocument39 pagesRevised Model GST LawkshitijsaxenaNo ratings yet

- GST With Examples: GST India - Goods & Service TaxDocument4 pagesGST With Examples: GST India - Goods & Service TaxVipul Priya KumarNo ratings yet

- 3 1.2.2 Principal Adg Sushil Solanki GSTDocument23 pages3 1.2.2 Principal Adg Sushil Solanki GSTpradeeperd10011988No ratings yet

- VAT vs GST: Key Differences Between Value Added Tax and Goods and Services TaxDocument7 pagesVAT vs GST: Key Differences Between Value Added Tax and Goods and Services TaxArundhuti RoyNo ratings yet

- 908 - GST E BookDocument63 pages908 - GST E Bookdcsreddy94No ratings yet

- Goods and Service Tax (GST)Document17 pagesGoods and Service Tax (GST)Manav SethiNo ratings yet

- Goods and Service Tax: The Way AheadDocument17 pagesGoods and Service Tax: The Way AheadsaffuNo ratings yet

- GST PPT Intro (1) - MergedDocument47 pagesGST PPT Intro (1) - MergedRahulNo ratings yet

- Overview of GST - PPT For GACDocument57 pagesOverview of GST - PPT For GACRonak DesaiNo ratings yet

- Introduction To GSTDocument22 pagesIntroduction To GSTSowmya KRNo ratings yet

- Presentation On GST by Himanshu and KrishnaDocument21 pagesPresentation On GST by Himanshu and KrishnahimanshuNo ratings yet

- GST framework analysis: Current system vs proposalDocument1 pageGST framework analysis: Current system vs proposalChetan VirkarNo ratings yet

- Understanding GST in India - 20 Common Questions AnsweredDocument20 pagesUnderstanding GST in India - 20 Common Questions AnsweredApoorvaNo ratings yet

- GST Alert 01 Decoding GST Presentation On Promises of GSTDocument73 pagesGST Alert 01 Decoding GST Presentation On Promises of GSTbibhugudu2002No ratings yet

- 3-SIB Infy TemplateDocument8 pages3-SIB Infy TemplateKunal ChawlaNo ratings yet

- HPCL ValuationDocument6 pagesHPCL ValuationKunal ChawlaNo ratings yet

- Presentation by - Hitaksha Gambhir - Archana Ramesh - Kushal Shah - Harshil Bhadra - Suyog KandiDocument25 pagesPresentation by - Hitaksha Gambhir - Archana Ramesh - Kushal Shah - Harshil Bhadra - Suyog KandiKunal ChawlaNo ratings yet

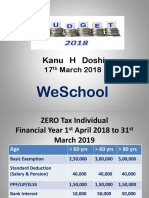

- Kanu H Doshi: 17 March 2018Document16 pagesKanu H Doshi: 17 March 2018Kunal ChawlaNo ratings yet

- Cover Letter InternshipDocument1 pageCover Letter InternshipKunal ChawlaNo ratings yet

- GCL PresentationDocument18 pagesGCL PresentationKunal ChawlaNo ratings yet

- The Mozal ProjectDocument34 pagesThe Mozal ProjectKunal ChawlaNo ratings yet

- ﳷवदेश मं낰ालय भारत सरकार Ministry of External Affairs Government of India Online Appointment ReceiptDocument3 pagesﳷवदेश मं낰ालय भारत सरकार Ministry of External Affairs Government of India Online Appointment ReceiptKunal ChawlaNo ratings yet

- GCL PresentationDocument18 pagesGCL PresentationKunal ChawlaNo ratings yet

- Flare Fragrance Company Inc SWOT analysis and strategies to increase market shareDocument9 pagesFlare Fragrance Company Inc SWOT analysis and strategies to increase market shareSatish Kumar BurraNo ratings yet

- JJJDocument5 pagesJJJKunal ChawlaNo ratings yet

- LeadsDocument1 pageLeadsKunal ChawlaNo ratings yet

- Uw 19 Phy Bs 059Document1 pageUw 19 Phy Bs 059Afghan LoralaiNo ratings yet

- 3 Cash - Lecture Notes PDFDocument11 pages3 Cash - Lecture Notes PDFJohn Paul EslerNo ratings yet

- Sbi Gauri Oct To Feb19Document26 pagesSbi Gauri Oct To Feb19laxmikantNo ratings yet

- Account statement details for Panyam BalajiDocument4 pagesAccount statement details for Panyam BalajibalajiNo ratings yet

- Vestal 5 ScheduleDocument2 pagesVestal 5 ScheduleRohan ChopraNo ratings yet

- INCOTERMS 2020 Rules Short - TFG - Summary PDFDocument20 pagesINCOTERMS 2020 Rules Short - TFG - Summary PDFaryanNo ratings yet

- ITRDocument1 pageITRpradip_jsr13No ratings yet

- Tax Invoice: Account For Professional FeesDocument1 pageTax Invoice: Account For Professional FeesVinh DuongNo ratings yet

- Bank Reconciliation Statements 5: This Chapter Covers..Document18 pagesBank Reconciliation Statements 5: This Chapter Covers..amal joy0% (1)

- Il Digital July2015Document268 pagesIl Digital July2015NNo ratings yet

- Service Quotation For APC SRT3000RMXLI With Network Card-Prosperity Knitwear LTDDocument1 pageService Quotation For APC SRT3000RMXLI With Network Card-Prosperity Knitwear LTDYe Yan NaingNo ratings yet

- Total Cash 8,050,000: Additional InformationDocument10 pagesTotal Cash 8,050,000: Additional Informationeia aieNo ratings yet

- Customer Satisfaction Towards PAYtm ServicesDocument53 pagesCustomer Satisfaction Towards PAYtm ServicesVignesh Kumar Voleti69% (13)

- Quiz 4 ScenariosDocument2 pagesQuiz 4 ScenariosMatthew PhalanndwaNo ratings yet

- April To May 19 Mobile BillDocument3 pagesApril To May 19 Mobile BillPravin AwalkondeNo ratings yet

- Jul 15 - Aug 14 PDFDocument5 pagesJul 15 - Aug 14 PDFpat orantezNo ratings yet

- Please Detach Coupon and Return Payment Using The Enclosed Envelope - Allow 5 Days For Mail DeliveryDocument4 pagesPlease Detach Coupon and Return Payment Using The Enclosed Envelope - Allow 5 Days For Mail DeliveryAnatoliy PopikNo ratings yet

- Ola Vs Uber Business Research Management QuestionnaireDocument5 pagesOla Vs Uber Business Research Management QuestionnaireAmol NagapNo ratings yet

- Cheque Account Statement: 39 Edwards Road Witfield 1459Document4 pagesCheque Account Statement: 39 Edwards Road Witfield 1459Blackie BlackieNo ratings yet

- TAX 1016 Lesson TWODocument8 pagesTAX 1016 Lesson TWOMonica MonicaNo ratings yet

- Dub 5198522Document1 pageDub 5198522Anand BabuNo ratings yet

- Uqld2915518153052999 Payment SummaryDocument1 pageUqld2915518153052999 Payment SummarylavidisNo ratings yet

- University of Karachi deposit slip titleDocument1 pageUniversity of Karachi deposit slip titletalhaNo ratings yet

- Barge Container PDFDocument6 pagesBarge Container PDFAndreea MunteanuNo ratings yet

- Jawahar Vidya Mandir: ReceiptDocument2 pagesJawahar Vidya Mandir: ReceiptRavindra SahuNo ratings yet

- Authorize hotel charges with CC formDocument2 pagesAuthorize hotel charges with CC formLiza wong100% (1)

- Tax System Explained in 40 CharactersDocument4 pagesTax System Explained in 40 CharactersankitrajeNo ratings yet

- Anderson County's Delinquent Tax SaleDocument3 pagesAnderson County's Delinquent Tax SaleUSA TODAY Network50% (2)

- 1 Tax RatesDocument5 pages1 Tax Ratesvinod nainiwalNo ratings yet

- Assignment Acc106 Jan 2012Document11 pagesAssignment Acc106 Jan 2012irfanzzz75% (8)