You might also like

- TenancyDocument2 pagesTenancyIbrahim Dibal0% (2)

- PREC Comments On FOMB CTO Motion 11-03-17Document19 pagesPREC Comments On FOMB CTO Motion 11-03-17Gavin BadeNo ratings yet

- R.A. No. 11976 - Ease of Paying TaxesDocument18 pagesR.A. No. 11976 - Ease of Paying TaxesBeaNo ratings yet

- Auditing Theory Answer Key (2011) by Salosagcol, Tiu, and HermosillaDocument1 pageAuditing Theory Answer Key (2011) by Salosagcol, Tiu, and HermosillaRJ Diana0% (1)

- Briefing On RA 10963: Tax Reform For Acceleration and Inclusion (TRAIN) - Power and Authority ofDocument4 pagesBriefing On RA 10963: Tax Reform For Acceleration and Inclusion (TRAIN) - Power and Authority ofanon galNo ratings yet

- Tax Reform for Acceleration and Inclusion (TRAIN) Act SummaryDocument61 pagesTax Reform for Acceleration and Inclusion (TRAIN) Act SummaryRose LeeNo ratings yet

- Safari - 24 Apr 2019 at 2:35 PMDocument1 pageSafari - 24 Apr 2019 at 2:35 PMStephany PolinarNo ratings yet

- Bir Train Vs Nirc FullDocument177 pagesBir Train Vs Nirc FullliANo ratings yet

- Train RT PDFDocument158 pagesTrain RT PDFYen AcederaNo ratings yet

- Comparative Analysis 8424 and 10963Document31 pagesComparative Analysis 8424 and 10963Rizza Angela Mangalleno100% (2)

- Republic Act No. 10963: Summon, Examine, and Take Testimony of Persons. - in Ascertaining TheDocument55 pagesRepublic Act No. 10963: Summon, Examine, and Take Testimony of Persons. - in Ascertaining TheAra LimNo ratings yet

- TRAIN Comparative Table 20170111 11AMDocument33 pagesTRAIN Comparative Table 20170111 11AMButch kevin adovasNo ratings yet

- Other Matters PDFDocument29 pagesOther Matters PDFEunice Jean AquinoNo ratings yet

- Senate Bill On Tax Reform For Acceleration and Inclusion: in BriefDocument26 pagesSenate Bill On Tax Reform For Acceleration and Inclusion: in BriefSeung-Ho YooNo ratings yet

- Tax Reform For Acceleration and Inclusion - Package 1: in BriefDocument27 pagesTax Reform For Acceleration and Inclusion - Package 1: in BriefAngel JuanNo ratings yet

- Republic Act No. 8424 National Internal Revenue Code of 1997Document37 pagesRepublic Act No. 8424 National Internal Revenue Code of 1997dave_88opNo ratings yet

- Republic Act No. 10963Document46 pagesRepublic Act No. 10963Wilson MoranoNo ratings yet

- RTI Recommendations to Strengthen Transparency and AccountabilityDocument10 pagesRTI Recommendations to Strengthen Transparency and Accountabilityawadhesh008No ratings yet

- Train Law Ra 10953Document32 pagesTrain Law Ra 10953IanaNo ratings yet

- TRAIN (Changes) ???? Pages 2, 3, 5, 7Document4 pagesTRAIN (Changes) ???? Pages 2, 3, 5, 7blackmail1No ratings yet

- BIR TRAIN BriefingDocument223 pagesBIR TRAIN BriefingRealliance PHNo ratings yet

- Guidance For Agencies On Transfers From The Spectrum Relocation Fund For Certain Pre-Auction CostsDocument4 pagesGuidance For Agencies On Transfers From The Spectrum Relocation Fund For Certain Pre-Auction CostsPeggy W SatterfieldNo ratings yet

- Republic Act No. 10963 (TRAIN Law)Document54 pagesRepublic Act No. 10963 (TRAIN Law)gerardmcastilloNo ratings yet

- TRAIN (Changes) ???? Pages 1, 3, 7Document3 pagesTRAIN (Changes) ???? Pages 1, 3, 7blackmail1No ratings yet

- SEC Report on Real-Time Short Position ReportingDocument149 pagesSEC Report on Real-Time Short Position ReportingTobiasNo ratings yet

- 365722-2023-Bataan Revenue Code of 202320230911-25-m5b4p0Document43 pages365722-2023-Bataan Revenue Code of 202320230911-25-m5b4p0Ren Mar CruzNo ratings yet

- TRAIN (Changes) ???? Pages 2, 3, 14, 15 PDFDocument4 pagesTRAIN (Changes) ???? Pages 2, 3, 14, 15 PDFblackmail1No ratings yet

- Train Law PDFDocument27 pagesTrain Law PDFLanieLampasaNo ratings yet

- General Guidelines - State Controlled EnterprisesDocument39 pagesGeneral Guidelines - State Controlled EnterprisestechnicalvijayNo ratings yet

- Philippine Communications Satellite Corporation vs. AlcuazDocument23 pagesPhilippine Communications Satellite Corporation vs. AlcuazKentfhil Mae AseronNo ratings yet

- Thirteenth Finance Commission Chapter 10: Annex: Data Collected by The CommissionDocument36 pagesThirteenth Finance Commission Chapter 10: Annex: Data Collected by The CommissionB V KumarNo ratings yet

- Philcomsat rate reduction challengedDocument2 pagesPhilcomsat rate reduction challengedMaan LucsNo ratings yet

- Taxation Law Reviewpower of Cir ReportDocument31 pagesTaxation Law Reviewpower of Cir ReportFiliusdeiNo ratings yet

- Phil. Communications Satellite Corporation vs. AlcuazDocument19 pagesPhil. Communications Satellite Corporation vs. AlcuazRustom IbañezNo ratings yet

- CBDTDocument4 pagesCBDTGaurav RohillaNo ratings yet

- CDD GuidelinesDocument61 pagesCDD GuidelinesFrancescoNo ratings yet

- Taxation Review - Pre-Finals (A.Y. 2015-2016Document37 pagesTaxation Review - Pre-Finals (A.Y. 2015-2016Mary Grace OrdonezNo ratings yet

- PF_CH_5_QUIZ.docxDocument4 pagesPF_CH_5_QUIZ.docxlexfred55No ratings yet

- PHILCOMSAT v. AlcuazDocument20 pagesPHILCOMSAT v. AlcuazJohn FerarenNo ratings yet

- How to Handle Letter of Authority to Examine CooperativesDocument42 pagesHow to Handle Letter of Authority to Examine CooperativesJeanette LampitocNo ratings yet

- Transportation Law ReviewDocument50 pagesTransportation Law Reviewroy rebosuraNo ratings yet

- PHILCOMSAT Vs AlcuazDocument16 pagesPHILCOMSAT Vs AlcuazPJ SLSRNo ratings yet

- Rmo 27-2010 Reinvigorated Rate ProgramDocument7 pagesRmo 27-2010 Reinvigorated Rate ProgramKris CalabiaNo ratings yet

- RMO 46-04 AffidaitDocument9 pagesRMO 46-04 Affidaitnathalie velasquezNo ratings yet

- S 3. Section 5 of The National Internal Revenue Code of 1997 (NIRC), As Amended, Is Hereby FurtherDocument46 pagesS 3. Section 5 of The National Internal Revenue Code of 1997 (NIRC), As Amended, Is Hereby FurtherAthena GarridoNo ratings yet

- Public Service Act Commonwealth Act No. 146 As Amended by RA 11659Document11 pagesPublic Service Act Commonwealth Act No. 146 As Amended by RA 11659May Angelique J. MagbooNo ratings yet

- Oo Policy Briefing Coverage of Corporate Vehicles 2023 04Document31 pagesOo Policy Briefing Coverage of Corporate Vehicles 2023 04Yevhen KurilovNo ratings yet

- Nir Code, 1997Document64 pagesNir Code, 1997benzylicNo ratings yet

- Power Supply Regulation 28.9Document11 pagesPower Supply Regulation 28.9Manoj RanaNo ratings yet

- ACCOUNTING-GOVERNMENTDocument12 pagesACCOUNTING-GOVERNMENTluzespinosa602No ratings yet

- RA 10963 Tax Reform For Acceleration and InclusionDocument54 pagesRA 10963 Tax Reform For Acceleration and Inclusionjpeb100% (2)

- HQ01 - General Principles of TaxationDocument14 pagesHQ01 - General Principles of TaxationJimmyChao100% (1)

- Revenue Memorandum Order No. 23-97: April 7, 1997Document6 pagesRevenue Memorandum Order No. 23-97: April 7, 1997Rieland CuevasNo ratings yet

- RA No. 10963 - Tax Reform For Acceleration and Inclusion (TRAIN Law)Document54 pagesRA No. 10963 - Tax Reform For Acceleration and Inclusion (TRAIN Law)Anostasia NemusNo ratings yet

- TRAI ArticlesDocument4 pagesTRAI ArticlesGaurav RohillaNo ratings yet

- Draft Regulation 24022023Document36 pagesDraft Regulation 24022023arunkvklNo ratings yet

- Mmda VS GarinDocument16 pagesMmda VS GarinVictor Bautista YarciaNo ratings yet

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- Procurement and Supply Chain Management: Emerging Concepts, Strategies and ChallengesFrom EverandProcurement and Supply Chain Management: Emerging Concepts, Strategies and ChallengesNo ratings yet

- ABA - Annual Report 2018Document146 pagesABA - Annual Report 2018Ivan ChiuNo ratings yet

- 3 - Conceptual FrameworkDocument3 pages3 - Conceptual FrameworkIvan ChiuNo ratings yet

- Month Day Month Day: 526-1212, Extension 2403 / 8231-10-73 (Temporary)Document209 pagesMonth Day Month Day: 526-1212, Extension 2403 / 8231-10-73 (Temporary)Ivan ChiuNo ratings yet

- ABA - Annual Report 2017Document128 pagesABA - Annual Report 2017Ivan ChiuNo ratings yet

- Bachelor of Science in Computer ScienceDocument3 pagesBachelor of Science in Computer ScienceIvan ChiuNo ratings yet

- 4 - MethodologyDocument6 pages4 - MethodologyIvan ChiuNo ratings yet

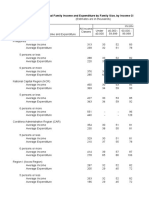

- Table 2 Total and Average Annual Family Income and Expenditure by Income Class and by Region 2018Document8 pagesTable 2 Total and Average Annual Family Income and Expenditure by Income Class and by Region 2018Glenn GalvezNo ratings yet

- ABA - Annual Report 2019Document169 pagesABA - Annual Report 2019Ivan ChiuNo ratings yet

- Table 7 Mean and Median Family Income and Expenditure by Per Capita Income Decile and by Region, 2018Document16 pagesTable 7 Mean and Median Family Income and Expenditure by Per Capita Income Decile and by Region, 2018Ivan ChiuNo ratings yet

- 6 - Summary, Conclusion and RecommendationDocument3 pages6 - Summary, Conclusion and RecommendationIvan ChiuNo ratings yet

- Table 1 Number of Families, Total and Average Annual Family Income and Expenditure by Region 2018Document2 pagesTable 1 Number of Families, Total and Average Annual Family Income and Expenditure by Region 2018Ivan ChiuNo ratings yet

- The Treasury Nominal Coupon-Issue (TNC) Yield Curve: 10-Year Average Spot Rates, PercentDocument9 pagesThe Treasury Nominal Coupon-Issue (TNC) Yield Curve: 10-Year Average Spot Rates, PercentIvan ChiuNo ratings yet

- Table 3 Total and Average Annual Family Income and Expenditure by Expenditure Class and by Region 2018Document8 pagesTable 3 Total and Average Annual Family Income and Expenditure by Expenditure Class and by Region 2018Ivan ChiuNo ratings yet

- Table 5 Average Annual Family Income and Expenditure by Family Size, by Income Class and by Region, 2018Document10 pagesTable 5 Average Annual Family Income and Expenditure by Family Size, by Income Class and by Region, 2018Ivan ChiuNo ratings yet

- 7 - BibliographyDocument4 pages7 - BibliographyIvan ChiuNo ratings yet

- 5 - Results and DiscussionDocument5 pages5 - Results and DiscussionIvan ChiuNo ratings yet

- CSC 121Document8 pagesCSC 121Ivan ChiuNo ratings yet

- Accounting For Branches and Combined FSDocument112 pagesAccounting For Branches and Combined FSMuhammad Fahad100% (2)

- Operating Segment Is The Ppe of The Mother It's About Time On Trying To Hold Deep. IFRS But Not FischerDocument1 pageOperating Segment Is The Ppe of The Mother It's About Time On Trying To Hold Deep. IFRS But Not FischerIvan ChiuNo ratings yet

- CIMA ScenarioDocument10 pagesCIMA ScenarioPerfectionism FollowerNo ratings yet

- Bscs Se v2011 PDFDocument3 pagesBscs Se v2011 PDFBobNo ratings yet

- 47.taxability of Productivity Incentive Bonuses.07.10.08.GACDocument2 pages47.taxability of Productivity Incentive Bonuses.07.10.08.GACEumell Alexis PaleNo ratings yet

- Audit Internal ExternalDocument1 pageAudit Internal ExternalIvan ChiuNo ratings yet

- Operating Segment Is The Ppe of The Mother It's About Time On Trying To Hold Deep. IFRS But Not FischerDocument1 pageOperating Segment Is The Ppe of The Mother It's About Time On Trying To Hold Deep. IFRS But Not FischerIvan ChiuNo ratings yet

- Salosagcol Audit Theory Is The Mean Way To Financial Statement But Black Scholes Is The BestDocument1 pageSalosagcol Audit Theory Is The Mean Way To Financial Statement But Black Scholes Is The BestIvan ChiuNo ratings yet

- Critique of Comtemporary Philippine FilmsDocument1 pageCritique of Comtemporary Philippine FilmsIvan ChiuNo ratings yet

- It's Not About The Thing That Cats and Mouse Are Not in Harmony With Each Other. Alan Peter. and Cuaderno EstebanDocument1 pageIt's Not About The Thing That Cats and Mouse Are Not in Harmony With Each Other. Alan Peter. and Cuaderno EstebanIvan ChiuNo ratings yet

- Power of The MassesDocument1 pagePower of The MassesIvan ChiuNo ratings yet

- Law New ReleasesDocument34 pagesLaw New ReleasesPankajNo ratings yet

- DIP 2021-22 - Presentation Schedule & Zoom LinksDocument5 pagesDIP 2021-22 - Presentation Schedule & Zoom LinksMimansa KalaNo ratings yet

- HR 332 CCT PDFDocument3 pagesHR 332 CCT PDFGabriela Women's PartyNo ratings yet

- Sandoval v. Secretary of The California Department of Corrections and Rehabilitation - Document No. 2Document3 pagesSandoval v. Secretary of The California Department of Corrections and Rehabilitation - Document No. 2Justia.comNo ratings yet

- CPDprovider PHYSICALTHERAPY-71818Document7 pagesCPDprovider PHYSICALTHERAPY-71818PRC Board100% (1)

- Imm5406e Final - PDF FamilyDocument1 pageImm5406e Final - PDF FamilyAngela KhodorkovskiNo ratings yet

- Jurnal Kepimpinan Pendidikan - : Kualiti Guru Dan Penguasaan Bahasa Cina Murid Sekolah Kebangsaan Di SelangorDocument19 pagesJurnal Kepimpinan Pendidikan - : Kualiti Guru Dan Penguasaan Bahasa Cina Murid Sekolah Kebangsaan Di SelangorRatieqah NajeehahNo ratings yet

- Erd.2.f.008 Sworn AffidavitDocument2 pagesErd.2.f.008 Sworn Affidavitblueberry712No ratings yet

- Gulliver's Travels to BrobdingnagDocument8 pagesGulliver's Travels to BrobdingnagAshish JainNo ratings yet

- Borders Negative CaseDocument161 pagesBorders Negative CaseJulioacg98No ratings yet

- Tehran Times, 16.11.2023Document8 pagesTehran Times, 16.11.2023nika242No ratings yet

- I of C Globally: VOL 13 No. 4 JUL 10 - MAR 11Document44 pagesI of C Globally: VOL 13 No. 4 JUL 10 - MAR 11saurabhgupta4378No ratings yet

- The Dreyfus AffairDocument3 pagesThe Dreyfus AffairShelly Conner LuikhNo ratings yet

- Disability Embodiment and Ableism Stories of ResistanceDocument15 pagesDisability Embodiment and Ableism Stories of ResistanceBasmaMohamedNo ratings yet

- Monday, May 05, 2014 EditionDocument16 pagesMonday, May 05, 2014 EditionFrontPageAfricaNo ratings yet

- Honorata Jakubowska, Dominik Antonowicz, Radoslaw Kossakowski - Female Fans, Gender Relations and Football Fandom-Routledge (2020)Document236 pagesHonorata Jakubowska, Dominik Antonowicz, Radoslaw Kossakowski - Female Fans, Gender Relations and Football Fandom-Routledge (2020)marianaencarnacao00No ratings yet

- Capital PunishmentDocument3 pagesCapital PunishmentAnony MuseNo ratings yet

- WW 3Document12 pagesWW 3ayesha ziaNo ratings yet

- Analysis of 'Travel and Drugs in Twentieth-Century LiteratureDocument4 pagesAnalysis of 'Travel and Drugs in Twentieth-Century LiteratureMada AnandiNo ratings yet

- Aerial Incident of 27 July 1995Document5 pagesAerial Incident of 27 July 1995Penn Angelo RomboNo ratings yet

- Angan Micro Action PlanDocument5 pagesAngan Micro Action PlanZEETECH COMPUTERSNo ratings yet

- Ra 7941 - Party List System ActDocument5 pagesRa 7941 - Party List System Act文子No ratings yet

- Final Test Subject: Sociolinguistics Lecturer: Dr. H. Pauzan, M. Hum. M. PDDocument25 pagesFinal Test Subject: Sociolinguistics Lecturer: Dr. H. Pauzan, M. Hum. M. PDAyudia InaraNo ratings yet

- People Vs YauDocument7 pagesPeople Vs YauMark DungoNo ratings yet

- Week 7 MAT101Document28 pagesWeek 7 MAT101Rexsielyn BarquerosNo ratings yet

- Gender-Inclusive Urban Planning and DesignDocument106 pagesGender-Inclusive Urban Planning and DesignEylül ErgünNo ratings yet

- Texas Farm Bureau Insurance Arbitration EndorsementDocument2 pagesTexas Farm Bureau Insurance Arbitration EndorsementTexas WatchNo ratings yet

- DETERMINE MEANING FROM CONTEXTDocument2 pagesDETERMINE MEANING FROM CONTEXTKevin SeptianNo ratings yet