You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Agreement To Demolish/Remove and Reconstruct Improvement (Adri)Document3 pagesAgreement To Demolish/Remove and Reconstruct Improvement (Adri)PANGINOON LOVE100% (1)

- Donor's Tax: Answer: DDocument6 pagesDonor's Tax: Answer: DAngela Miles DizonNo ratings yet

- Page 174 FigureDocument1 pagePage 174 Figureadiba10mktNo ratings yet

- 1 s2.0 S1877042814039688 MainDocument9 pages1 s2.0 S1877042814039688 MainLightgrey DimitryNo ratings yet

- Form 21 - Automobile Ownership Transfer Related Buyer's Announcement - BRTA 2023Document1 pageForm 21 - Automobile Ownership Transfer Related Buyer's Announcement - BRTA 2023adiba10mktNo ratings yet

- Marketing Strategy - Cravens Piercy BookDocument21 pagesMarketing Strategy - Cravens Piercy BookMd. Mashud Hossain TalukderNo ratings yet

- Gender Alchohol and The Media - The Portrayal of Men and Women in Alcohol CommercialsDocument15 pagesGender Alchohol and The Media - The Portrayal of Men and Women in Alcohol Commercialsadiba10mktNo ratings yet

- ECS Gilrs On Presentations and PHD ProposalDocument12 pagesECS Gilrs On Presentations and PHD ProposalazhafizNo ratings yet

- My Take On Chapter 8 Principles of MarketingDocument35 pagesMy Take On Chapter 8 Principles of Marketingadiba10mktNo ratings yet

- Flexible Wide Area Consistency Management: Sai SusarlaDocument24 pagesFlexible Wide Area Consistency Management: Sai Susarlablack smithNo ratings yet

- Lastovicka Fernandez 2005 JCRDocument12 pagesLastovicka Fernandez 2005 JCRadiba10mktNo ratings yet

- Emerging Pattern of Global Change in The Upper Atmosphere and IonosphereDocument15 pagesEmerging Pattern of Global Change in The Upper Atmosphere and Ionosphereadiba10mktNo ratings yet

- Discussion On Presenting Various Seminars PDFDocument39 pagesDiscussion On Presenting Various Seminars PDFadiba10mktNo ratings yet

- ECS Gilrs On Presentations and PHD ProposalDocument12 pagesECS Gilrs On Presentations and PHD ProposalazhafizNo ratings yet

- Answers of The Research Questions Assignment 1Document8 pagesAnswers of The Research Questions Assignment 1adiba10mktNo ratings yet

- Lecture Sheet For SPSSDocument29 pagesLecture Sheet For SPSSadiba10mkt100% (1)

- Answers of The Research Questions Assignment 1Document8 pagesAnswers of The Research Questions Assignment 1adiba10mktNo ratings yet

- PHD 2019 Survey BUPDocument10 pagesPHD 2019 Survey BUPadiba10mktNo ratings yet

- Assignment 1 AdibaDocument18 pagesAssignment 1 Adibaadiba10mktNo ratings yet

- Assign 1Document3 pagesAssign 1adiba10mktNo ratings yet

- Assignment 1 AdibaDocument18 pagesAssignment 1 Adibaadiba10mktNo ratings yet

- Assignment 1: Class Work: 1 Case Study: A Job Satisfaction SurveyDocument2 pagesAssignment 1: Class Work: 1 Case Study: A Job Satisfaction Surveyadiba10mktNo ratings yet

- Soluton Assign 3Document24 pagesSoluton Assign 3adiba10mktNo ratings yet

- Spada 1st AssignmentDocument10 pagesSpada 1st Assignmentadiba10mktNo ratings yet

- Quantitativedataanalysis 131122004449 Phpapp01Document30 pagesQuantitativedataanalysis 131122004449 Phpapp01adiba10mktNo ratings yet

- Personal BrandingDocument37 pagesPersonal BrandingJohn RadcliffeNo ratings yet

- Example How To Write A ProposalDocument9 pagesExample How To Write A ProposalSpoorthi PoojariNo ratings yet

- Quantitativedataanalysis 131122004449 Phpapp01Document30 pagesQuantitativedataanalysis 131122004449 Phpapp01adiba10mktNo ratings yet

- Apa Stem GuildDocument5 pagesApa Stem GuildJyo RoyNo ratings yet

- Apa Stem GuildDocument5 pagesApa Stem GuildJyo RoyNo ratings yet

- Main Difference - Approach Vs MethodDocument2 pagesMain Difference - Approach Vs Methodadiba10mktNo ratings yet

- Course Outline Marketing ManagementDocument2 pagesCourse Outline Marketing Managementadiba10mktNo ratings yet

- EstateDocument6 pagesEstateJAYAR MENDZNo ratings yet

- Form IR2 4Document3 pagesForm IR2 4khaingshwe wutyiNo ratings yet

- Taxation - Defined - August 22, 2013Document93 pagesTaxation - Defined - August 22, 2013Asdqwe ZaqwsxNo ratings yet

- Form 16: Wipro LimitedDocument8 pagesForm 16: Wipro LimitedpadduNo ratings yet

- InvoiceDocument1 pageInvoicepravin pathadeNo ratings yet

- International Commercial Invoice TemplateDocument3 pagesInternational Commercial Invoice TemplatePhilip WathenNo ratings yet

- Wholesale BB Rates - Shawal Dhul Qe'daDocument2 pagesWholesale BB Rates - Shawal Dhul Qe'daRyan DarmawanNo ratings yet

- Inter Company Invoicing ProcessDocument1 pageInter Company Invoicing Processaj9055537No ratings yet

- KPQooo 001266420000 R 07112758 C846621Document1 pageKPQooo 001266420000 R 07112758 C846621Jonathan GutierrezNo ratings yet

- EF2A2 HDT Budget Indirect Taxes GST PCB7 1661016598246Document44 pagesEF2A2 HDT Budget Indirect Taxes GST PCB7 1661016598246Sikha SharmaNo ratings yet

- Guidelines For Investment Proof PDFDocument2 pagesGuidelines For Investment Proof PDFsamuraioo7No ratings yet

- GST ChallanDocument1 pageGST Challanproject worksNo ratings yet

- Fringe Benefits TaxDocument4 pagesFringe Benefits TaxKathleen Jane SolmayorNo ratings yet

- AK Personal 1Document13 pagesAK Personal 1erniNo ratings yet

- Cash and Accrual Basis ProblemsDocument1 pageCash and Accrual Basis ProblemsCAINo ratings yet

- Philippine Taxation SystemDocument71 pagesPhilippine Taxation SystemKathleen V.No ratings yet

- Tax Structuring Advisory Report: Prepared For China Shandong Industries IncDocument17 pagesTax Structuring Advisory Report: Prepared For China Shandong Industries IncChing, Quennel YoenNo ratings yet

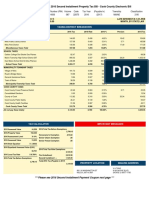

- Cook County Propertytax Bill 2016 Second InstallmentDocument2 pagesCook County Propertytax Bill 2016 Second InstallmentbenNo ratings yet

- Deduction PDFDocument207 pagesDeduction PDFdeepluthra6No ratings yet

- Schedule of Caf DT Reg MN-24 HindiDocument4 pagesSchedule of Caf DT Reg MN-24 Hindisogoja2705No ratings yet

- PdataDocument6 pagesPdataRazor11111No ratings yet

- Capital Gains Section 54 ChartDocument6 pagesCapital Gains Section 54 ChartYamuna GNo ratings yet

- 311970536Document1 page311970536Codrut RadantaNo ratings yet

- ICCT Colleges Foundation, Inc.: - Activity / AssignmentDocument2 pagesICCT Colleges Foundation, Inc.: - Activity / AssignmentDamayan XeroxanNo ratings yet

- Travel by Air ServicesDocument15 pagesTravel by Air ServicesvijaykoratNo ratings yet

- Brief History of Tax LawsDocument9 pagesBrief History of Tax LawsSaad AhmedNo ratings yet

- Final TaxDocument33 pagesFinal TaxAlicia FelicianoNo ratings yet

- Adriano Alessandro Averzano 2019 Tax ReturnDocument21 pagesAdriano Alessandro Averzano 2019 Tax ReturnMucho FacerapeNo ratings yet