You might also like

- Amazon's Main Business Units Analyzed Using BCG MatrixDocument11 pagesAmazon's Main Business Units Analyzed Using BCG MatrixManhNo ratings yet

- Dampak Penerapan PSAK 72 Terhadap Kinerja Keuangan Perusahaan Telekomunikasi Di Masa Pandemi Covid-19Document17 pagesDampak Penerapan PSAK 72 Terhadap Kinerja Keuangan Perusahaan Telekomunikasi Di Masa Pandemi Covid-19rani adilahNo ratings yet

- AUDIT BAB 7 FixDocument10 pagesAUDIT BAB 7 FixGusNo ratings yet

- Lie Dharma Putra-Audit EngagementDocument3 pagesLie Dharma Putra-Audit EngagementDarma SparrowNo ratings yet

- Tugas Hukum PajakDocument18 pagesTugas Hukum Pajakdicky putraNo ratings yet

- Upaya Melawan Pandemi Covid-19 Di Indonesia, Studi Kasus Fasilitas Kepabeanan Dan Perdagangan InternasionalDocument9 pagesUpaya Melawan Pandemi Covid-19 Di Indonesia, Studi Kasus Fasilitas Kepabeanan Dan Perdagangan InternasionalFEGIYA ARINDI Ilmu EkonomiNo ratings yet

- Analisis Perbandingan Tax Amnesty Jilid I Dan Jilid IIDocument11 pagesAnalisis Perbandingan Tax Amnesty Jilid I Dan Jilid IIMurphy HeideggerNo ratings yet

- Basics of International Tax RegimeDocument17 pagesBasics of International Tax RegimeAbhishek RaiNo ratings yet

- Pajak Internasional 181112019Document87 pagesPajak Internasional 181112019ekaNo ratings yet

- 3 Pengaruh Insentif Pajak Dan Faktor Nonpajak Terhadap Konservatisme Akuntansi Perusahaan Manufaktur Terdaftar Di BeiDocument15 pages3 Pengaruh Insentif Pajak Dan Faktor Nonpajak Terhadap Konservatisme Akuntansi Perusahaan Manufaktur Terdaftar Di BeiServitalleNo ratings yet

- Program Pendidikan Khusus Praktisi Pajak: Pengaruh Omnibus Law PerpajakanDocument62 pagesProgram Pendidikan Khusus Praktisi Pajak: Pengaruh Omnibus Law PerpajakanlarryNo ratings yet

- Art 2 Oecd MCDocument161 pagesArt 2 Oecd MCMihaela CtsNo ratings yet

- Analisis Yuridis Mekanisme Penyelesaian Sengketa PDocument12 pagesAnalisis Yuridis Mekanisme Penyelesaian Sengketa P17. M. Taqwa Syach AlamNo ratings yet

- Peranan Penyidik Bea Cukai Dalam Pemberantasan Tindak Pidana Penyelundupan Narkotika Pada Kantor Pengawasan Dan Pelayanan Bea Dan Cukai KualanamuDocument53 pagesPeranan Penyidik Bea Cukai Dalam Pemberantasan Tindak Pidana Penyelundupan Narkotika Pada Kantor Pengawasan Dan Pelayanan Bea Dan Cukai KualanamuAfa Ranggita PrasticasariNo ratings yet

- Penerapan Metode Cup Pada Transaksi Cpo Antara Pihak-Pihak Yang Memiliki Hubungan IstimewaDocument16 pagesPenerapan Metode Cup Pada Transaksi Cpo Antara Pihak-Pihak Yang Memiliki Hubungan Istimewakhunaina il khafa ainul NazilatulNo ratings yet

- Losses Vis-A-Vis Transfer PricingDocument10 pagesLosses Vis-A-Vis Transfer PricingChirag ShahNo ratings yet

- Topic 1 Introduction To TaxationDocument28 pagesTopic 1 Introduction To TaxationZebedee Taltal0% (1)

- Anzelika Cintana - Tugas Minggu Ke-9 - AM-S1 ManajemenDocument9 pagesAnzelika Cintana - Tugas Minggu Ke-9 - AM-S1 ManajemenApes Together Strongs ATSNo ratings yet

- Analisis Pengaruh Pajak Dan Mekanisme Bonus Terhadap Keputusan Transfer Pricing (3 Files Merged)Document63 pagesAnalisis Pengaruh Pajak Dan Mekanisme Bonus Terhadap Keputusan Transfer Pricing (3 Files Merged)Elsa Kisari PutriNo ratings yet

- Artikel Sistem PerpajakanDocument9 pagesArtikel Sistem PerpajakanfauzanNo ratings yet

- Fundamentals of Transfer Pricing & Associated EnterpriseDocument18 pagesFundamentals of Transfer Pricing & Associated Enterprisemaria felicianaNo ratings yet

- Analisis Kasus Sengketa Perpajakan Di IndonesiaDocument22 pagesAnalisis Kasus Sengketa Perpajakan Di IndonesiaJoshua PlanktonNo ratings yet

- Jurnal PajakDocument8 pagesJurnal PajakSriWahyuniNo ratings yet

- Pajak InternasionalDocument60 pagesPajak InternasionalTutunKasepNo ratings yet

- The Impact of Tax Treaties and EU Law On Group Taxation Regimes PDFDocument665 pagesThe Impact of Tax Treaties and EU Law On Group Taxation Regimes PDFHoa Hướng DươngNo ratings yet

- EY Overview of Transfer PricingDocument39 pagesEY Overview of Transfer PricingChanduNo ratings yet

- Tax Compliance and Tax Sharing Impact on East Java EconomyDocument10 pagesTax Compliance and Tax Sharing Impact on East Java EconomystnrindriyaniNo ratings yet

- Tanggung Jawab Atas Tindakan Ultra Vires Anggota Direksi Dalam Kasus Kasus Kepailitan Perseroan 28 Sept 2012Document23 pagesTanggung Jawab Atas Tindakan Ultra Vires Anggota Direksi Dalam Kasus Kasus Kepailitan Perseroan 28 Sept 2012AlifMuhammadFadliNo ratings yet

- Etika Bisnis Dan Profesi - The Ethics of Tax AccountingDocument15 pagesEtika Bisnis Dan Profesi - The Ethics of Tax AccountingBudsNo ratings yet

- The Decision Usefulness Approach to Financial ReportingDocument27 pagesThe Decision Usefulness Approach to Financial ReportingAyu PuspitasariNo ratings yet

- Tax Compliance and Self-Assessment Models ExploredDocument16 pagesTax Compliance and Self-Assessment Models ExploredarekdarmoNo ratings yet

- Law No. 6 of 1983 On General Tax Provisions and Procedures (English)Document41 pagesLaw No. 6 of 1983 On General Tax Provisions and Procedures (English)Ranny Hadrianto100% (2)

- Jurnal Akuntansi Dan Keuangan Vol 14 No 2Document146 pagesJurnal Akuntansi Dan Keuangan Vol 14 No 2Benedicts100% (5)

- Gayus Holomoan P. TambunanDocument8 pagesGayus Holomoan P. TambunanDhimas Herdhi Yekti WibowoNo ratings yet

- Tax AuditDocument16 pagesTax AuditArifin FuNo ratings yet

- ID Penegakan Hukum Pelaku Tindak Pidana Peredaran Rokok Tanpa Pita Cukai BerdasarkaDocument15 pagesID Penegakan Hukum Pelaku Tindak Pidana Peredaran Rokok Tanpa Pita Cukai BerdasarkaLilis RahmawatiNo ratings yet

- PSAK 73 implementation challengesDocument10 pagesPSAK 73 implementation challengesanalisa akuntansiNo ratings yet

- AKMEN Relevant CostDocument25 pagesAKMEN Relevant Costriadi wolfNo ratings yet

- Urnal Kuntansi Emerintah: Advance Pricing Agreement Dalam KaitannyaDocument12 pagesUrnal Kuntansi Emerintah: Advance Pricing Agreement Dalam KaitannyaIin Mochamad SolihinNo ratings yet

- Receive $1 today or $1 one year from now? Comparing simple and compound interestDocument52 pagesReceive $1 today or $1 one year from now? Comparing simple and compound interestXenopol XenopolNo ratings yet

- Jurnal Pajak PDFDocument8 pagesJurnal Pajak PDFJuna Ej EdwardNo ratings yet

- Reactions of Capital Markets To Financial ReportingDocument19 pagesReactions of Capital Markets To Financial ReportingMila Minkhatul Maula MingmilaNo ratings yet

- Transfer Pricing of Intangibles A ComparDocument84 pagesTransfer Pricing of Intangibles A ComparCupid LoveNo ratings yet

- Forensic Accounting - Fraud Examination Sesi 1 Pengertian Akuntansi ForensikDocument31 pagesForensic Accounting - Fraud Examination Sesi 1 Pengertian Akuntansi ForensikBaMbAng HartaDINo ratings yet

- Psak 71 Instrumen Keuangan: Pengakuan Dan PengukuranDocument102 pagesPsak 71 Instrumen Keuangan: Pengakuan Dan PengukuranandriNo ratings yet

- Dual Residence and Solution Under Treaty AgreementDocument25 pagesDual Residence and Solution Under Treaty AgreementEdwin AdriantoNo ratings yet

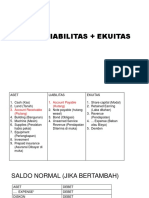

- Persamaan Dasar AkuntansiDocument10 pagesPersamaan Dasar Akuntansiapelina teresia100% (1)

- KPMG Tax Shelter Caymen Islands KPMG Tax Shelter Caymen IslandsDocument4 pagesKPMG Tax Shelter Caymen Islands KPMG Tax Shelter Caymen Islandskpmgtaxshelter_kpmg tax shelter-kpmg tax shelterNo ratings yet

- Comparative Accounting Americas and AsiaDocument23 pagesComparative Accounting Americas and AsiaAlmaliyana BasyaibanNo ratings yet

- Pengaruh Kualitas Pelayanan, Kewajiban Moral Dan Sanksi Perpajakan Terhadap Kepatuhan Wajib Pajak Hotel Dalam Membayar Pajak Hotel (Studi Kasuspada Wajib Pajak Hotel Di Kota Pekanbaru)Document14 pagesPengaruh Kualitas Pelayanan, Kewajiban Moral Dan Sanksi Perpajakan Terhadap Kepatuhan Wajib Pajak Hotel Dalam Membayar Pajak Hotel (Studi Kasuspada Wajib Pajak Hotel Di Kota Pekanbaru)Muhammad Rizal SurbaktiNo ratings yet

- International TaxationDocument8 pagesInternational Taxationsrinivas kolaganiNo ratings yet

- DatabaseDocument61 pagesDatabaseNavneet GulatiNo ratings yet

- Delik-Korupsi - Yudi KristianaDocument76 pagesDelik-Korupsi - Yudi KristianaMutiaNo ratings yet

- Tugas Sipi Kelompok 5 - Turbo, IncDocument14 pagesTugas Sipi Kelompok 5 - Turbo, IncwlseptiaraNo ratings yet

- ch13 Behavioural AccountingDocument32 pagesch13 Behavioural AccountingAdinda Widyastari100% (1)

- National Power Corporation vs. Municipal Government of NavotasDocument11 pagesNational Power Corporation vs. Municipal Government of NavotasEvelyn TocgongnaNo ratings yet

- Legal Ethics DigestsDocument18 pagesLegal Ethics DigestsMiguel AlagNo ratings yet

- CTA upholds taxpayer's right to due process in tax assessment caseDocument4 pagesCTA upholds taxpayer's right to due process in tax assessment caseBelle MaturanNo ratings yet

- Lozada v. BracewellDocument14 pagesLozada v. BracewellIyaNo ratings yet

- Gulf Air Company vs. CirDocument1 pageGulf Air Company vs. CirLisley Gem AmoresNo ratings yet

- 2645 1 3570 1 10 20121113Document28 pages2645 1 3570 1 10 20121113Artika Enggar DwiastutiNo ratings yet

- 390 1607 1 PBDocument16 pages390 1607 1 PBsarasatiwanamiNo ratings yet

- 928 3542 1 PBDocument20 pages928 3542 1 PBsarasatiwanamiNo ratings yet

- Traditional Balinese Food Potential as Superior ProductsDocument7 pagesTraditional Balinese Food Potential as Superior ProductsYudhi Pratama100% (2)

- Sa June11 Process2Document8 pagesSa June11 Process2LeoEdeOmoregieNo ratings yet

- No Akun Keterangan Debet KreditDocument1 pageNo Akun Keterangan Debet KreditsarasatiwanamiNo ratings yet

- National Economics Competition Questions 2016Document15 pagesNational Economics Competition Questions 2016BravoUcoNo ratings yet

- Sa June11 Process2Document8 pagesSa June11 Process2LeoEdeOmoregieNo ratings yet

- Understanding Antimicrobial Resistance MechanismsDocument31 pagesUnderstanding Antimicrobial Resistance MechanismssarasatiwanamiNo ratings yet

- History of Technological ChangeDocument14 pagesHistory of Technological ChangesarasatiwanamiNo ratings yet

- Why English is EssentialDocument1 pageWhy English is EssentialsarasatiwanamiNo ratings yet

- Components of The Internal Control ProcessDocument7 pagesComponents of The Internal Control ProcesssarasatiwanamiNo ratings yet

- PDFDocument170 pagesPDFsarasatiwanamiNo ratings yet

- Loloh Cecem - 1Document1 pageLoloh Cecem - 1sarasatiwanamiNo ratings yet

- Student ProjectDocument23 pagesStudent ProjectsarasatiwanamiNo ratings yet

- Lecture 14 PROTOZOA INTESTINAL REVISI 9 JanDocument38 pagesLecture 14 PROTOZOA INTESTINAL REVISI 9 JansarasatiwanamiNo ratings yet

- MODUL 07 - Sarasati Pramudia - 1506305079Document2 pagesMODUL 07 - Sarasati Pramudia - 1506305079sarasatiwanamiNo ratings yet

- Inventory CalculationDocument8 pagesInventory CalculationsarasatiwanamiNo ratings yet

- Lecture 11 Zoonosis FK 2017Document42 pagesLecture 11 Zoonosis FK 2017sarasatiwanamiNo ratings yet

- TaxesDocument8 pagesTaxessarasatiwanamiNo ratings yet

- 2.3 PTUN in EnglishDocument3 pages2.3 PTUN in EnglishsarasatiwanamiNo ratings yet

- Hotel Daily Report Sample1Document2 pagesHotel Daily Report Sample1Hotel Manager Ramada Bengaluru Yelahanka75% (8)

- Cooperative and SME Syllabus BreakdownDocument6 pagesCooperative and SME Syllabus BreakdownsarasatiwanamiNo ratings yet

- Lecture 13 GENERAL - PARASITOLOGYDocument29 pagesLecture 13 GENERAL - PARASITOLOGYsarasatiwanamiNo ratings yet

- MODUL 9 (Cash Flow)Document3 pagesMODUL 9 (Cash Flow)sarasatiwanamiNo ratings yet

- Module 6-Installment-Sarasati Pramudia-1506305079Document9 pagesModule 6-Installment-Sarasati Pramudia-1506305079sarasatiwanamiNo ratings yet

- Paper Pajak Final (PRINT) Income Tax and VATDocument21 pagesPaper Pajak Final (PRINT) Income Tax and VATsarasatiwanamiNo ratings yet

- Koperasi Dapat Berbentuk Koperasi Primer Atau Koperasi SekunderDocument3 pagesKoperasi Dapat Berbentuk Koperasi Primer Atau Koperasi SekundersarasatiwanamiNo ratings yet

- Modul 4 (Aging Schedule)Document6 pagesModul 4 (Aging Schedule)sarasatiwanamiNo ratings yet

- Command Economy Systems and Growth ModelsDocument118 pagesCommand Economy Systems and Growth Modelsmeenaroja100% (1)

- Customs ClearanceDocument35 pagesCustoms ClearanceZhizheng ChenNo ratings yet

- Newcombe 2003Document9 pagesNewcombe 2003Nicolae VedovelliNo ratings yet

- GROUP 2 - The Filipino Is Worth Dying ForDocument2 pagesGROUP 2 - The Filipino Is Worth Dying ForGian DelcanoNo ratings yet

- NATIONAL POLICY FOR WOMEN EMPOWERMENTDocument15 pagesNATIONAL POLICY FOR WOMEN EMPOWERMENTTahesin MalekNo ratings yet

- Empowerment, subsistence and a different view of global economyDocument5 pagesEmpowerment, subsistence and a different view of global economyBruna Romero-MelgarNo ratings yet

- Philippine Association of Certified Tax Technicians, Inc. (Pactt)Document1 pagePhilippine Association of Certified Tax Technicians, Inc. (Pactt)Ralph Christer MaderazoNo ratings yet

- Rizal's Homecoming and Departure (1887-1888Document34 pagesRizal's Homecoming and Departure (1887-1888Sheila G. DolipasNo ratings yet

- CaseDocument22 pagesCaseLex AcadsNo ratings yet

- Fact Sheet: The Need For ICWA ICWA Implementation ConcernsDocument2 pagesFact Sheet: The Need For ICWA ICWA Implementation ConcernsDawn AnaangoonsiikweNo ratings yet

- Emperor of CorruptionDocument128 pagesEmperor of CorruptionRam CharanNo ratings yet

- Cost Benefit Analysis of Reorganization in Public SectorDocument79 pagesCost Benefit Analysis of Reorganization in Public SectorGeorgeNo ratings yet

- US Supreme Court JudgmentDocument2 pagesUS Supreme Court JudgmentPamela FunesNo ratings yet

- Ead-519 - Case Study - Dress CodeDocument7 pagesEad-519 - Case Study - Dress Codeapi-263391699No ratings yet

- JFQ 72Document112 pagesJFQ 72Allen Bundy100% (1)

- Thabo Mbeki's Letter To Jacob Zuma Regarding The ANC VeteransDocument5 pagesThabo Mbeki's Letter To Jacob Zuma Regarding The ANC VeteransBruce Gorton100% (6)

- Introduction To Diya' Al-UmmatDocument10 pagesIntroduction To Diya' Al-UmmatMS1986No ratings yet

- United States Court of Appeals Third CircuitDocument6 pagesUnited States Court of Appeals Third CircuitScribd Government DocsNo ratings yet

- Elphos Erald: Postal Museum Marks Third GalaDocument16 pagesElphos Erald: Postal Museum Marks Third GalaThe Delphos HeraldNo ratings yet

- Manila Standard Today - May 30, 2012 IssueDocument16 pagesManila Standard Today - May 30, 2012 IssueManila Standard TodayNo ratings yet

- Qua Che Gen vs. Deportation BoARDDocument6 pagesQua Che Gen vs. Deportation BoARDdenvergamlosenNo ratings yet

- Introduction To Political SociologyDocument22 pagesIntroduction To Political SociologyNeisha Kavita Mahase100% (1)

- Frantz Fanon and His Blueprint For African Culture(s) - Apeike Umolu - AfricxnDocument12 pagesFrantz Fanon and His Blueprint For African Culture(s) - Apeike Umolu - AfricxnApeike UmoluNo ratings yet

- Https Indiapostgdsonline - in Gdsonlinec3p4 Reg Print - AspxDocument1 pageHttps Indiapostgdsonline - in Gdsonlinec3p4 Reg Print - AspxALWIN JohnNo ratings yet

- Flers-Courcelette - The First Tank Battle - Richard FaulknerDocument5 pagesFlers-Courcelette - The First Tank Battle - Richard Faulknerxt828No ratings yet

- Osmeña vs. Pendatun (Digest)Document1 pageOsmeña vs. Pendatun (Digest)Precious100% (2)

- Stigma & Social Identity - Mini-PresentationDocument12 pagesStigma & Social Identity - Mini-PresentationKarim SheikhNo ratings yet

- Hughes The Weary Blues - A Case of Double ConsciousnessDocument23 pagesHughes The Weary Blues - A Case of Double ConsciousnessKatleen FalvoNo ratings yet

- Entrepreneurship - Technology and Livelihood EducationDocument10 pagesEntrepreneurship - Technology and Livelihood EducationNix Roberts100% (1)

- Presentation Icce 2017 Unp Sumaryati UadiDocument14 pagesPresentation Icce 2017 Unp Sumaryati UadiZaidNo ratings yet