You might also like

- UEU Akuntansi Biaya Pertemuan 12Document54 pagesUEU Akuntansi Biaya Pertemuan 12Sofyan AliNo ratings yet

- Joint Cost NewDocument54 pagesJoint Cost NewHadii SadjjaNo ratings yet

- Cost Allocation: Joint Products and ByproductsDocument54 pagesCost Allocation: Joint Products and ByproductsNoga RoseNo ratings yet

- UEU Akbi Pertemuan 12Document55 pagesUEU Akbi Pertemuan 12jhayciepunzalanNo ratings yet

- Cost Allocation: Joint Products and Byproducts: 2009 Foster School of Business Cost Accounting L.Ducharme 1Document35 pagesCost Allocation: Joint Products and Byproducts: 2009 Foster School of Business Cost Accounting L.Ducharme 1alancarlogalvezNo ratings yet

- Cost Allocation: Joint Products and Byproducts: 2009 Foster School of Business Cost Accounting L.DucharmeDocument35 pagesCost Allocation: Joint Products and Byproducts: 2009 Foster School of Business Cost Accounting L.DucharmeDarryl LeeNo ratings yet

- Intermediate Financial Accounting - I-1-1Document9 pagesIntermediate Financial Accounting - I-1-1natinaelbahiru74No ratings yet

- Lecture 7Document14 pagesLecture 7marwanfathy002No ratings yet

- F 5 Progressssjune 2016 SOLNDocument12 pagesF 5 Progressssjune 2016 SOLNAnisahMahmoodNo ratings yet

- UNIT-V-Joint-and-By-product-costingDocument12 pagesUNIT-V-Joint-and-By-product-costingEross Jacob SalduaNo ratings yet

- Unit 5. Accounting For Joint Products & Byproducts: 5.1 OverviewDocument9 pagesUnit 5. Accounting For Joint Products & Byproducts: 5.1 OverviewAmanuel TesfayeNo ratings yet

- Managerial accounting techniques for cost analysisDocument3 pagesManagerial accounting techniques for cost analysisLeah Jane Tablante EsguerraNo ratings yet

- Joint Product and by Product TestDocument10 pagesJoint Product and by Product Testthatfuturecpa100% (1)

- Week 6-7 joint costs allocationDocument5 pagesWeek 6-7 joint costs allocationFebemay LindaNo ratings yet

- Certificate in Management Accounting Level 3/series 3-2009Document15 pagesCertificate in Management Accounting Level 3/series 3-2009Hein Linn Kyaw100% (2)

- At Wid SolDocument4 pagesAt Wid SolglamfactorsalonspaNo ratings yet

- Unit 7: Joint and By-Product Costing SystemDocument8 pagesUnit 7: Joint and By-Product Costing SystemCielo PulmaNo ratings yet

- Management Accounting: Level 3Document16 pagesManagement Accounting: Level 3Hein Linn KyawNo ratings yet

- Joint Product L7 UpdatedDocument14 pagesJoint Product L7 Updatedviony catelinaNo ratings yet

- Exercise-1 (A) : Joint and by Product Costing (Sales Value at Split Off Method)Document15 pagesExercise-1 (A) : Joint and by Product Costing (Sales Value at Split Off Method)Sky SoronoiNo ratings yet

- Institute of Certified General Accountants of Bangladesh (ICGAB) Performance Management (P13) LC-3: CVP AnalysisDocument5 pagesInstitute of Certified General Accountants of Bangladesh (ICGAB) Performance Management (P13) LC-3: CVP AnalysisMozid RahmanNo ratings yet

- F5 RevDocument69 pagesF5 Revpercy mapetereNo ratings yet

- CVP Analysis F5 NotesDocument7 pagesCVP Analysis F5 NotesSiddiqua KashifNo ratings yet

- Acc123 J&BPDocument20 pagesAcc123 J&BPCali SiobhanNo ratings yet

- At 3Document8 pagesAt 3Ley EsguerraNo ratings yet

- Achievement Test 3: Chapters 5-6 Managerial AccountingDocument8 pagesAchievement Test 3: Chapters 5-6 Managerial AccountingJoshua GibsonNo ratings yet

- Mid Term PracticeDocument12 pagesMid Term PracticeOtabek KhamidovNo ratings yet

- Joint Products and by Notes For HND 2022-2023Document6 pagesJoint Products and by Notes For HND 2022-2023TolaNo ratings yet

- GNB13 e CH 07 ExamDocument4 pagesGNB13 e CH 07 ExamWendors WendorsNo ratings yet

- 08 Costing By-Products & Joint ProductsDocument15 pages08 Costing By-Products & Joint ProductsDenise Villanueva40% (5)

- Management Accounting Exam Practice KitDocument405 pagesManagement Accounting Exam Practice Kittshepiso msimanga100% (4)

- Name: Roll Number: Class: Submitted To:: Riphah International CollegeDocument4 pagesName: Roll Number: Class: Submitted To:: Riphah International CollegePathanNo ratings yet

- Ch7 CVPDocument26 pagesCh7 CVPbekbek12No ratings yet

- Marginal Costing and CVP Analysis: Group 4Document31 pagesMarginal Costing and CVP Analysis: Group 4Aiman Farhan100% (1)

- 6 Joint AND By-Product Costing: Lecture Notes - 12/13 Jan 2015Document27 pages6 Joint AND By-Product Costing: Lecture Notes - 12/13 Jan 2015XNo ratings yet

- CH # 8 (By Product)Document10 pagesCH # 8 (By Product)Rooh Ullah KhanNo ratings yet

- Summary of The Chapter: Joint ProductsDocument3 pagesSummary of The Chapter: Joint ProductsSaad QureshiNo ratings yet

- Ch.5 Abc & MGMT: Emphasis. New York: Mcgraw-Hill Irwin (5-4)Document15 pagesCh.5 Abc & MGMT: Emphasis. New York: Mcgraw-Hill Irwin (5-4)Winter SummerNo ratings yet

- Ch08TB PDFDocument15 pagesCh08TB PDFMico Duñas CruzNo ratings yet

- 2014 Bep Analysis ExercisesDocument5 pages2014 Bep Analysis ExercisesaimeeNo ratings yet

- Cost Volume Profit Analysis Lecture NotesDocument27 pagesCost Volume Profit Analysis Lecture NotesbiggykhairNo ratings yet

- Topic 7 Lecture Slides SharedDocument39 pagesTopic 7 Lecture Slides SharedSonam Dema DorjiNo ratings yet

- Example 3 On Joint CostDocument9 pagesExample 3 On Joint CostJessicaTheLazy PlayerNo ratings yet

- S (RS.) 200 200 Rs. 40,00,000Document51 pagesS (RS.) 200 200 Rs. 40,00,000raandkadeewanaNo ratings yet

- Revision 2Document37 pagesRevision 2percy mapetereNo ratings yet

- RVU CMA Work Sheet March 2019Document12 pagesRVU CMA Work Sheet March 2019Henok FikaduNo ratings yet

- C8 (MC) - Cost Accounting by Carter (Part1)Document3 pagesC8 (MC) - Cost Accounting by Carter (Part1)AkiNo ratings yet

- Example Single Product LTD: Required: (A) Calculate The FollowingDocument3 pagesExample Single Product LTD: Required: (A) Calculate The FollowingHamza0% (1)

- Answers Homework # 13 Cost MGMT 2Document6 pagesAnswers Homework # 13 Cost MGMT 2Raman ANo ratings yet

- Process Costing - ContinuedDocument8 pagesProcess Costing - ContinuedUnique GadtaulaNo ratings yet

- Kumpulan Kuis Akmen 2Document13 pagesKumpulan Kuis Akmen 2IstiqomahNo ratings yet

- Cost 4Document5 pagesCost 4Aschenaki MebreNo ratings yet

- Gls University'S Faculty of Commerce Semester - Iv Cost Accounting - 2 Objective Questions 2017-2018Document12 pagesGls University'S Faculty of Commerce Semester - Iv Cost Accounting - 2 Objective Questions 2017-2018Archana0% (1)

- Joint Products and Byproduct 2Document10 pagesJoint Products and Byproduct 2shai santiagoNo ratings yet

- CH 4 Job Costing PDFDocument11 pagesCH 4 Job Costing PDFMohamed DiabNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

- Student Factors Affecting Retention Rate of Bachelor of Science in AccountancyDocument29 pagesStudent Factors Affecting Retention Rate of Bachelor of Science in AccountancyMicka EllahNo ratings yet

- Philippines 1987 PDFDocument67 pagesPhilippines 1987 PDFSomaya BasareNo ratings yet

- Itlogan Sa Dabaw FarmDocument15 pagesItlogan Sa Dabaw FarmMicka EllahNo ratings yet

- Finding A Cryptocurrency Transaction ID (TXID) : What Is A Bitcoin Account?Document3 pagesFinding A Cryptocurrency Transaction ID (TXID) : What Is A Bitcoin Account?Micka EllahNo ratings yet

- Audit of liabilities quiz problemsDocument4 pagesAudit of liabilities quiz problemsEarl Donne Cruz100% (4)

- Questions BroodingDocument5 pagesQuestions BroodingMicka EllahNo ratings yet

- Chicken Ipr Jan Jun2015Document21 pagesChicken Ipr Jan Jun2015Micka EllahNo ratings yet

- Sample ReferencesDocument5 pagesSample ReferencesMicka EllahNo ratings yet

- Reference FinalDocument4 pagesReference FinalMicka EllahNo ratings yet

- Independent Auditor'S Report: Responsibilities For The Audit of The Consolidated Financial Statements Section of OurDocument10 pagesIndependent Auditor'S Report: Responsibilities For The Audit of The Consolidated Financial Statements Section of OurMicka EllahNo ratings yet

- RRLDocument3 pagesRRLMicka EllahNo ratings yet

- Implementing Strategies: Management & Operations IssuesDocument33 pagesImplementing Strategies: Management & Operations IssuesMicka EllahNo ratings yet

- NameDocument1 pageNameMicka EllahNo ratings yet

- RRLDocument3 pagesRRLMicka EllahNo ratings yet

- Student Satisfaction and Persistence: Factors Vital To Student RetentionDocument18 pagesStudent Satisfaction and Persistence: Factors Vital To Student RetentionAsti HaryaniNo ratings yet

- RRLDocument3 pagesRRLMicka EllahNo ratings yet

- Concept Paper Hideout Book CafeDocument2 pagesConcept Paper Hideout Book CafeBump ThreadsNo ratings yet

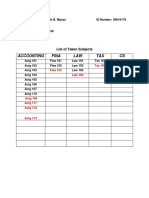

- Accounting Fina LAW TAX CS: List of Taken SubjectsDocument3 pagesAccounting Fina LAW TAX CS: List of Taken SubjectsMicka EllahNo ratings yet

- 3-1. Discussion Questions / ProblemsDocument4 pages3-1. Discussion Questions / Problemscoleen paraynoNo ratings yet

- Nfjpia Nmbe MS 2017 AnsDocument9 pagesNfjpia Nmbe MS 2017 AnsMicka EllahNo ratings yet

- Pɒnzi/ Fraud Investors Profits Funds: Martin Chuzzlewit Little DorritDocument1 pagePɒnzi/ Fraud Investors Profits Funds: Martin Chuzzlewit Little DorritMicka EllahNo ratings yet

- Madoff Securities Written Report2Document1 pageMadoff Securities Written Report2Micka EllahNo ratings yet

- RELATE TO PHILIPPINE SETTING-written ReportDocument2 pagesRELATE TO PHILIPPINE SETTING-written ReportMicka EllahNo ratings yet

- RR No. 12-2018: New Consolidated RR on Estate Tax and Donor's TaxDocument20 pagesRR No. 12-2018: New Consolidated RR on Estate Tax and Donor's Taxjune Alvarez100% (1)

- Abraham MaslowDocument3 pagesAbraham MaslowMicka EllahNo ratings yet

- Sample3 SolDocument8 pagesSample3 SolRhoda Mae AlbaNo ratings yet

- Madoff Ponzi SchemeDocument7 pagesMadoff Ponzi SchemeMicka EllahNo ratings yet

- Budget ProcessDocument42 pagesBudget ProcessMicka EllahNo ratings yet

- The Estate's orDocument2 pagesThe Estate's orMicka EllahNo ratings yet

- 2017 Internal Auditor ReportDocument3 pages2017 Internal Auditor ReportMicka EllahNo ratings yet

- Cantilever Retaining Wall AnalysisDocument7 pagesCantilever Retaining Wall AnalysisChub BokingoNo ratings yet

- Accident Causation Theories and ConceptDocument4 pagesAccident Causation Theories and ConceptShayne Aira AnggongNo ratings yet

- Safety of High-Rise BuildingsDocument14 pagesSafety of High-Rise BuildingsHananeel Sandhi100% (2)

- Laporan Mutasi Inventory GlobalDocument61 pagesLaporan Mutasi Inventory GlobalEustas D PickNo ratings yet

- Managing operations service problemsDocument2 pagesManaging operations service problemsJoel Christian Mascariña0% (1)

- JIS K 6250: Rubber - General Procedures For Preparing and Conditioning Test Pieces For Physical Test MethodsDocument43 pagesJIS K 6250: Rubber - General Procedures For Preparing and Conditioning Test Pieces For Physical Test Methodsbignose93gmail.com0% (1)

- Request For AffidavitDocument2 pagesRequest For AffidavitGhee MoralesNo ratings yet

- Scenemaster3 ManualDocument79 pagesScenemaster3 ManualSeba Gomez LNo ratings yet

- Software Engineering Modern ApproachesDocument775 pagesSoftware Engineering Modern ApproachesErico Antonio TeixeiraNo ratings yet

- MT R 108 000 0 000000-0 DHHS B eDocument68 pagesMT R 108 000 0 000000-0 DHHS B eRafal WojciechowskiNo ratings yet

- Mesa de Trabajo 1Document1 pageMesa de Trabajo 1iamtheonionboiNo ratings yet

- Broschuere Unternehmen Screen PDFDocument16 pagesBroschuere Unternehmen Screen PDFAnonymous rAFSAGDAEJNo ratings yet

- Payroll Canadian 1st Edition Dryden Test BankDocument38 pagesPayroll Canadian 1st Edition Dryden Test Bankriaozgas3023100% (14)

- Terminología Sobre Reducción de Riesgo de DesastresDocument43 pagesTerminología Sobre Reducción de Riesgo de DesastresJ. Mario VeraNo ratings yet

- Article 4Document31 pagesArticle 4Abdul OGNo ratings yet

- Case Study Infrastructure ProjectsDocument1 pageCase Study Infrastructure ProjectsAnton_Young_1962No ratings yet

- Entrepreneurship and EconomicDocument2 pagesEntrepreneurship and EconomicSukruti BajajNo ratings yet

- Mint Delhi 13-12-2022Document18 pagesMint Delhi 13-12-2022Ayush sethNo ratings yet

- Exam Venue For Monday Sep 25, 2023 - 12-00 To 01-00Document7 pagesExam Venue For Monday Sep 25, 2023 - 12-00 To 01-00naveed hassanNo ratings yet

- ДСТУ EN ISO 2400-2016 - Калибровочный блок V1Document11 pagesДСТУ EN ISO 2400-2016 - Калибровочный блок V1Игорь ВадешкинNo ratings yet

- Perbandingan Sistem Pemerintahan Dalam Hal Pemilihan Kepala Negara Di Indonesia Dan SingapuraDocument9 pagesPerbandingan Sistem Pemerintahan Dalam Hal Pemilihan Kepala Negara Di Indonesia Dan SingapuraRendy SuryaNo ratings yet

- Activate Adobe Photoshop CS5 Free Using Serial KeyDocument3 pagesActivate Adobe Photoshop CS5 Free Using Serial KeyLukmanto68% (28)

- Organization Structure GuideDocument6 pagesOrganization Structure GuideJobeth BedayoNo ratings yet

- Nucleic Acid Isolation System: MolecularDocument6 pagesNucleic Acid Isolation System: MolecularWarung Sehat Sukahati100% (1)

- Green Solvents For Chemistry - William M NelsonDocument401 pagesGreen Solvents For Chemistry - William M NelsonPhuong Tran100% (4)

- Human Resource Management: Chapter One-An Overview of Advanced HRMDocument45 pagesHuman Resource Management: Chapter One-An Overview of Advanced HRMbaba lakeNo ratings yet

- PNW 0605Document12 pagesPNW 0605sunf496No ratings yet

- Macdonald v. National City Bank of New YorkDocument6 pagesMacdonald v. National City Bank of New YorkSecret SecretNo ratings yet

- TicketDocument2 pagesTicketbikram kumarNo ratings yet

- CCTV8 PDFDocument2 pagesCCTV8 PDFFelix John NuevaNo ratings yet