You might also like

- Chapter # 21Document58 pagesChapter # 21Adil AliNo ratings yet

- Lecture 21CAs20Document21 pagesLecture 21CAs20mzNo ratings yet

- Business Magaizne Issue 56Document81 pagesBusiness Magaizne Issue 56Saad SheikhNo ratings yet

- Lecture 10 Relevant Costing PDFDocument49 pagesLecture 10 Relevant Costing PDFAira Kristel RomuloNo ratings yet

- Udu Franchise Fees & CostDocument3 pagesUdu Franchise Fees & Costtinditi123No ratings yet

- Car Rental 9-12 To 9-16Document2 pagesCar Rental 9-12 To 9-16Scott RanieriNo ratings yet

- TMC Insurance ProposalDocument6 pagesTMC Insurance ProposalmamathapraveenNo ratings yet

- October 8th, 2019 County Line ShopperDocument6 pagesOctober 8th, 2019 County Line ShopperMineral Wells Index/Weatherford DemocratNo ratings yet

- REALTY WEALTH ADVISORS 2 Story Rockport and Roll 1Document1 pageREALTY WEALTH ADVISORS 2 Story Rockport and Roll 1Oliver ProctorNo ratings yet

- The Confident Car Buyer Presentation Outline: This Seminar Will Review The Key Car Buying StagesDocument17 pagesThe Confident Car Buyer Presentation Outline: This Seminar Will Review The Key Car Buying Stagessudheerthota1225No ratings yet

- Specification Guide: Effective June 2, 2014Document83 pagesSpecification Guide: Effective June 2, 2014Vincent De GuzmanNo ratings yet

- International Travel Insurance Brochur9-1Document12 pagesInternational Travel Insurance Brochur9-1Samsu NishaNo ratings yet

- Arketeer: Wake Up With A Beautiful SmileDocument20 pagesArketeer: Wake Up With A Beautiful SmileCoolerAdsNo ratings yet

- Standard Cost & VarianceDocument26 pagesStandard Cost & VarianceWaqar AhmadNo ratings yet

- Annual Horse Expense Sheet: StablingDocument4 pagesAnnual Horse Expense Sheet: StablingAnonymous UwYVMOMxANo ratings yet

- All Amounts Are Listed in American Dollars (USD) .: Estimated Tuition and Living Expenses Breakdown Only ForDocument1 pageAll Amounts Are Listed in American Dollars (USD) .: Estimated Tuition and Living Expenses Breakdown Only ForKksbNo ratings yet

- October 1st, 2019 County Line ShopperDocument6 pagesOctober 1st, 2019 County Line ShopperMineral Wells Index/Weatherford DemocratNo ratings yet

- Poult Budg1Document22 pagesPoult Budg1Marcelito MorongNo ratings yet

- Adjusting Accounts and Preparing Financial Statements: © The Mcgraw-Hill Companies, Inc., 2005 Mcgraw-Hill/IrwinDocument47 pagesAdjusting Accounts and Preparing Financial Statements: © The Mcgraw-Hill Companies, Inc., 2005 Mcgraw-Hill/IrwinALDON NACUNo ratings yet

- Course Title: Estate Planning and Risk ManagementDocument10 pagesCourse Title: Estate Planning and Risk ManagementSahil MitraNo ratings yet

- 0523 County LineDocument8 pages0523 County LineMineral Wells Index/Weatherford DemocratNo ratings yet

- Weekly Budget Planner - 0Document6 pagesWeekly Budget Planner - 0Nabila ArifannisaNo ratings yet

- Personalbudget AbrilpereztorresDocument2 pagesPersonalbudget Abrilpereztorresapi-337682376No ratings yet

- Quote 1Document11 pagesQuote 1jchichoni1No ratings yet

- CRUISEFEST2009 InsuranceDocument3 pagesCRUISEFEST2009 InsurancegregggNo ratings yet

- 0801 County LineDocument8 pages0801 County LineMineral Wells Index/Weatherford DemocratNo ratings yet

- Breeding Costs SpreadsheetDocument2 pagesBreeding Costs Spreadsheetgerardo montiel gonzalezNo ratings yet

- Kia Build & Price Kia CanadaDocument1 pageKia Build & Price Kia CanadabssssmithNo ratings yet

- Media KIT: Arens CorporationDocument12 pagesMedia KIT: Arens CorporationGaryNo ratings yet

- Betriebskosten AvantIIDocument1 pageBetriebskosten AvantIITest ScribdNo ratings yet

- Airbnb Fina CalculatorDocument12 pagesAirbnb Fina CalculatorBagus Oka100% (1)

- Envy Rides Case DecisionDocument4 pagesEnvy Rides Case DecisionMikey MadRatNo ratings yet

- Daily Budget Spreadsheet: Week 1: ParticularsDocument9 pagesDaily Budget Spreadsheet: Week 1: ParticularsRafleah RiojaNo ratings yet

- 1107 County LineDocument8 pages1107 County LineMineral Wells Index/Weatherford DemocratNo ratings yet

- Make or BuyDocument51 pagesMake or BuySitaramanjaneyulu ManthaNo ratings yet

- Compare Needs VsDocument4 pagesCompare Needs Vsapi-5848438970% (1)

- GA Travel QuoteDocument2 pagesGA Travel Quoteidum brotherNo ratings yet

- 0606 County LineDocument8 pages0606 County LineMineral Wells Index/Weatherford DemocratNo ratings yet

- 5 Days MDP Course: Fabrikam ResidencesDocument19 pages5 Days MDP Course: Fabrikam ResidencesParnika JainNo ratings yet

- Week 7 - Bond Prices and YieldsDocument47 pagesWeek 7 - Bond Prices and YieldsshanikaNo ratings yet

- All Amounts Are Listed in American Dollars (USD) .: Estimated Tuition and Living Expenses Breakdown Only ForDocument1 pageAll Amounts Are Listed in American Dollars (USD) .: Estimated Tuition and Living Expenses Breakdown Only ForqwertyNo ratings yet

- Summary of Plan Benefits: ImportantDocument18 pagesSummary of Plan Benefits: ImportantYukonCorneliousNo ratings yet

- FB Med Supp BrochDocument2 pagesFB Med Supp BrochRegina AllenNo ratings yet

- Business Statistics Communicating With Numbers 3rd Edition Jaggia Solutions ManualDocument35 pagesBusiness Statistics Communicating With Numbers 3rd Edition Jaggia Solutions Manualabutter.dappledrep5100% (29)

- Estimated Closing Costs and Terminology Buyers 01-03-2018Document4 pagesEstimated Closing Costs and Terminology Buyers 01-03-2018Shay HataNo ratings yet

- TOMORROW - National Day CalendarDocument1 pageTOMORROW - National Day Calendar-fiz-No ratings yet

- BRRRR v2Document5 pagesBRRRR v2SujitKGoudarNo ratings yet

- Poult BudgDocument18 pagesPoult BudgSHAHUL HAMEEDNo ratings yet

- Group 4 Entrepreneur Chap 1 DraftDocument6 pagesGroup 4 Entrepreneur Chap 1 DraftTerence TamayoNo ratings yet

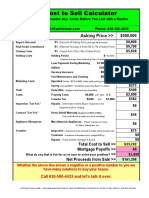

- Cost To Sell CalculatorDocument2 pagesCost To Sell CalculatorAjay SinghNo ratings yet

- Victa Split Roller Mower Lawn Mowers Gumtree Australia Stirling Area - Carine 1314348654Document1 pageVicta Split Roller Mower Lawn Mowers Gumtree Australia Stirling Area - Carine 1314348654w.mardonNo ratings yet

- What Does A Year Cost?: 2017-2018 TUITION AND FEESDocument4 pagesWhat Does A Year Cost?: 2017-2018 TUITION AND FEESYashrajsing LuckkanaNo ratings yet

- Dwnload Full Business Statistics Communicating With Numbers 3rd Edition Jaggia Solutions Manual PDFDocument18 pagesDwnload Full Business Statistics Communicating With Numbers 3rd Edition Jaggia Solutions Manual PDFtracicrawford2fwv100% (12)

- Individual Product - RatesTOB - V7Document3 pagesIndividual Product - RatesTOB - V7Hanifa MohammedNo ratings yet

- Baby On A Budget - SpreadsheetsDocument8 pagesBaby On A Budget - SpreadsheetsDya ZaiNo ratings yet

- How to Choose and Buy an RV: Here's how to get it right first and every timeFrom EverandHow to Choose and Buy an RV: Here's how to get it right first and every timeNo ratings yet

- BR2MJDocument1 pageBR2MJTravelwise VacationsNo ratings yet

- Draw A Diagram Similar To Exhibit 17-8 To Depict Edmonton Chemical Company's Joint Production ProcessDocument9 pagesDraw A Diagram Similar To Exhibit 17-8 To Depict Edmonton Chemical Company's Joint Production ProcessGillu BilluNo ratings yet

- Travel Single PagerDocument2 pagesTravel Single PagerArunava SahaNo ratings yet

- Estimated Panamax Dre: Item SBT Est. Dre $/DAY (365 Days)Document4 pagesEstimated Panamax Dre: Item SBT Est. Dre $/DAY (365 Days)George KanellakisNo ratings yet

- Microeconomics ProjectDocument5 pagesMicroeconomics ProjectRakesh ChoudharyNo ratings yet

- Neelam ReportDocument86 pagesNeelam Reportrjjain07100% (2)

- Key Findings 2004Document4 pagesKey Findings 2004aqua01No ratings yet

- Double Taxation Relief: Tax SupplementDocument5 pagesDouble Taxation Relief: Tax SupplementlalitbhatiNo ratings yet

- Algorithmic Market Making StrategiesDocument34 pagesAlgorithmic Market Making Strategiessahand100% (1)

- Terms and Conditions of Carriage enDocument32 pagesTerms and Conditions of Carriage enMuhammad AsifNo ratings yet

- Travel and Expense Policy: PurposeDocument9 pagesTravel and Expense Policy: Purposeabel_kayelNo ratings yet

- U.S. Customs Form: CBP Form 7552 - Delivery Certificate For Purposes of DrawbackDocument2 pagesU.S. Customs Form: CBP Form 7552 - Delivery Certificate For Purposes of DrawbackCustoms FormsNo ratings yet

- Simple GST Invoice Format in ExcelDocument2 pagesSimple GST Invoice Format in ExcelsadnNo ratings yet

- Contoh Curriculum Vitae Dokter UmumDocument2 pagesContoh Curriculum Vitae Dokter UmumPeter HoNo ratings yet

- Grant of IR17JulDocument2 pagesGrant of IR17JulAshwani BhallaNo ratings yet

- Steger Cooper ReadingGuideDocument2 pagesSteger Cooper ReadingGuideRicardo DíazNo ratings yet

- TYS 2007 To 2019 AnswersDocument380 pagesTYS 2007 To 2019 Answersshakthee sivakumarNo ratings yet

- Salary Slip (31920472 October, 2017) PDFDocument1 pageSalary Slip (31920472 October, 2017) PDFMuhammad Ishaq SonuNo ratings yet

- West Jet Encore Porter 5 Forces AnalysisDocument4 pagesWest Jet Encore Porter 5 Forces Analysisle duyNo ratings yet

- Rethinking Foreign Aid, SetaDocument5 pagesRethinking Foreign Aid, SetaAteki Seta CaxtonNo ratings yet

- 2023 - Forecast George FriedmanDocument17 pages2023 - Forecast George FriedmanGeorge BestNo ratings yet

- Extrajudicial Settlement With SaleDocument2 pagesExtrajudicial Settlement With SalePrince Rayner RoblesNo ratings yet

- Acct Statement XX1924 01122022Document10 pagesAcct Statement XX1924 01122022Yakshit YadavNo ratings yet

- February-14 Rural Development SchemesDocument52 pagesFebruary-14 Rural Development SchemesAnonymous gVledD7eUGNo ratings yet

- Prem BahadurDocument3 pagesPrem BahadurAditya RajNo ratings yet

- Tata Vistara - Agency PitchDocument27 pagesTata Vistara - Agency PitchNishant Prakash0% (1)

- 托福阅读功能目的题1 0Document59 pages托福阅读功能目的题1 0jessehuang922No ratings yet

- Chapter 7Document6 pagesChapter 7jobhihtihjrNo ratings yet

- Sample Fryer Rabbit Budget PDFDocument2 pagesSample Fryer Rabbit Budget PDFGrace NacionalNo ratings yet

- Ethiopia Profile Enhanced Final 7th October 2021Document6 pagesEthiopia Profile Enhanced Final 7th October 2021sarra TPINo ratings yet

- 7 Costs of ProductionDocument24 pages7 Costs of Productionakshat guptaNo ratings yet

- 82255BIR Form 1701Document12 pages82255BIR Form 1701Leowell John G. RapaconNo ratings yet

- Acceptance Payment Form: Tax Amnesty On DelinquenciesDocument1 pageAcceptance Payment Form: Tax Amnesty On DelinquenciesJennyMariedeLeonNo ratings yet

- Green Coffee FOB, C & F, CIF Contract: Specialty Coffee Association of AmericaDocument4 pagesGreen Coffee FOB, C & F, CIF Contract: Specialty Coffee Association of AmericacoffeepathNo ratings yet