You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- 1 4 1 12 FFFDocument13 pages1 4 1 12 FFFSatyam RastogiNo ratings yet

- French PDFDocument226 pagesFrench PDFbiroutiNo ratings yet

- Teachers Profile - FinalDocument4 pagesTeachers Profile - FinalSatyam RastogiNo ratings yet

- Profile For Brochrue 2016 (Prof. P.S. Tripathi)Document1 pageProfile For Brochrue 2016 (Prof. P.S. Tripathi)Satyam RastogiNo ratings yet

- Introductory FrenchDocument32 pagesIntroductory FrenchSameh Ahmed Hassan100% (2)

- VC MessageDocument1 pageVC MessageSatyam RastogiNo ratings yet

- What Is The Strategy To Impress ChaudhrainDocument1 pageWhat Is The Strategy To Impress ChaudhrainSatyam RastogiNo ratings yet

- Prof. S.K. SinghDocument1 pageProf. S.K. SinghSatyam RastogiNo ratings yet

- Prof. S.K. SinghDocument1 pageProf. S.K. SinghSatyam RastogiNo ratings yet

- VC MessageDocument1 pageVC MessageSatyam RastogiNo ratings yet

- International Business LawDocument4 pagesInternational Business LawSatyam RastogiNo ratings yet

- Marketing Services Jawed Habib SalonDocument31 pagesMarketing Services Jawed Habib SalonSatyam RastogiNo ratings yet

- WTO SPS Agreement and Dispute SettlementDocument5 pagesWTO SPS Agreement and Dispute SettlementSatyam RastogiNo ratings yet

- MT6582 Android ScatterDocument6 pagesMT6582 Android ScatterSathish KumarNo ratings yet

- Accounting For ManagersDocument286 pagesAccounting For ManagersSatyam Rastogi100% (1)

- DreamDocument249 pagesDreamSatyam RastogiNo ratings yet

- AdasdasdasDocument1 pageAdasdasdasSatyam RastogiNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- All AcDocument32 pagesAll AcVinod KumarNo ratings yet

- Goods - 5% Services - 5%: Water Utilities - 2%Document27 pagesGoods - 5% Services - 5%: Water Utilities - 2%Mari CrisNo ratings yet

- Confident Guidance CG 09-2013Document4 pagesConfident Guidance CG 09-2013api-249217077No ratings yet

- Channel Mapping LTEDocument24 pagesChannel Mapping LTEbadal mishraNo ratings yet

- ADMAS UNIVERSITY BISHOFTU CAMPUS - Docx 3333Document3 pagesADMAS UNIVERSITY BISHOFTU CAMPUS - Docx 3333Kalkidan Mesfin sheferaw0% (1)

- KPMG Ory - Insights - 27 - October - 2023 - Rbi - Issues - Master - Direction - Non - Banking - Company - Scale - Based - RegulationDocument27 pagesKPMG Ory - Insights - 27 - October - 2023 - Rbi - Issues - Master - Direction - Non - Banking - Company - Scale - Based - RegulationRangerNo ratings yet

- Dog Concierges, LLC: Transaction Analysis and Statement of Cash Flows PreparationDocument9 pagesDog Concierges, LLC: Transaction Analysis and Statement of Cash Flows PreparationCristina Elizabeth Portilla BravoNo ratings yet

- Sales Order ProcessingDocument5 pagesSales Order ProcessingSadaab HassanNo ratings yet

- Camtasia Comprehensive Review Problem 4-1Document30 pagesCamtasia Comprehensive Review Problem 4-1AC ConNo ratings yet

- Field Trip Permission SlipDocument1 pageField Trip Permission Slipapi-457788003No ratings yet

- Lichfield Sutton Coldfield Birmingham Long Bridge RedditchDocument4 pagesLichfield Sutton Coldfield Birmingham Long Bridge RedditchLouisMichaelNo ratings yet

- Accounting Information System ReviewDocument5 pagesAccounting Information System ReviewALMA MORENANo ratings yet

- E SCMDocument37 pagesE SCMindu296100% (2)

- Accounting For NADocument126 pagesAccounting For NADiane Christelle Montebon LacsonNo ratings yet

- Agriculture Appendix 32 FundsDocument1 pageAgriculture Appendix 32 FundsKim MonteronaNo ratings yet

- Pay Rates 24Document3 pagesPay Rates 24Mohammad Tayyab KhanNo ratings yet

- Accounts RTP CA Foundation May 2020Document31 pagesAccounts RTP CA Foundation May 2020YashNo ratings yet

- RRN3911 Deployment and O&M Guide (Rural Network Scenario) V3.1Document169 pagesRRN3911 Deployment and O&M Guide (Rural Network Scenario) V3.1Dante Tonzi100% (3)

- Assignment 4 OmDocument8 pagesAssignment 4 OmShafik MasriNo ratings yet

- Chap 12 Home Office Brranch Special Jan 2019Document7 pagesChap 12 Home Office Brranch Special Jan 2019Agatha de CastroNo ratings yet

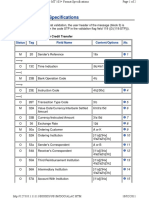

- MT 103+ Format Specifications: MT 103+ Single Customer Credit TransferDocument2 pagesMT 103+ Format Specifications: MT 103+ Single Customer Credit Transferme Nader100% (1)

- Katherine ResumeDocument3 pagesKatherine Resumeapi-272845852No ratings yet

- Mortgage Markets Chapter 11 Multiple Choice QuestionsDocument9 pagesMortgage Markets Chapter 11 Multiple Choice QuestionsSoraLeeNo ratings yet

- Proof of Cash ReconciliationDocument7 pagesProof of Cash ReconciliationReginald ValenciaNo ratings yet

- Inventories - SolutionDocument2 pagesInventories - SolutionKyla De LunaNo ratings yet

- Sports Medicine PhysicianDocument11 pagesSports Medicine Physicianapi-360560383No ratings yet

- Arens Chapter20Document105 pagesArens Chapter20rochielanciolaNo ratings yet

- Karthick Kumar Project - 7878Document109 pagesKarthick Kumar Project - 7878Karthick KumarNo ratings yet

- Unit 5th Herbal Drug Technology B Pharmacy 6th SemesterDocument10 pagesUnit 5th Herbal Drug Technology B Pharmacy 6th SemesterAliNo ratings yet

- Wireless Communication Protocols Comparison TableDocument1 pageWireless Communication Protocols Comparison TableasdNo ratings yet