You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Whirlpool SpreadsheetsDocument9 pagesWhirlpool SpreadsheetsBowen QinNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Spreadshit WhrilDocument6 pagesSpreadshit WhrilBowen QinNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Eee 625 P90Document1 pageEee 625 P90Bowen QinNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- LN06-Miller and Modigliani PropositionsDocument27 pagesLN06-Miller and Modigliani PropositionsBowen QinNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Challenger Sale Dixon en 17367Document6 pagesThe Challenger Sale Dixon en 17367Chakib LahfaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Basic Vessel Valuation - Issue No 3Document4 pagesBasic Vessel Valuation - Issue No 3SafoienTuihriNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Cooper Industries Case QuestionsDocument3 pagesCooper Industries Case QuestionsChip choiNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Threat of New EntrantsDocument5 pagesThreat of New EntrantsJAY MARK TANONo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Firestone CaseDocument2 pagesFirestone Caseel060275100% (2)

- Insurance Company Business PlanDocument36 pagesInsurance Company Business PlanS M Hasan Sayeed50% (2)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Grand Theater Is A Movie House in A Medium SizedDocument2 pagesThe Grand Theater Is A Movie House in A Medium Sizedtrilocksp SinghNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Cost Accounting Objective Type QuestionsDocument2 pagesCost Accounting Objective Type QuestionsJoshua Stalin Selvaraj75% (16)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Calculation of Index in FinanceDocument6 pagesCalculation of Index in FinanceAbhiSharmaNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Chapter 3. Financial IntermediariesDocument30 pagesChapter 3. Financial Intermediariesbr bhandariNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Module-5 Recent Trends in Marketing Online MarketingDocument7 pagesModule-5 Recent Trends in Marketing Online Marketingmurshidaman3No ratings yet

- Lembar Jawaban 1-JURNALDocument9 pagesLembar Jawaban 1-JURNALClara Shinta OceeNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- A192 - BEEB 1013 SyllabusDocument9 pagesA192 - BEEB 1013 SyllabusJasmine TehNo ratings yet

- National Stock ExchangeDocument3 pagesNational Stock ExchangeDhiraj AhujaNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Monetary and Fiscal Policy Skyveiw School QuizDocument32 pagesMonetary and Fiscal Policy Skyveiw School QuizHayleyblahblah100% (2)

- Financial Instrument SummaryDocument6 pagesFinancial Instrument SummaryJoshua ComerosNo ratings yet

- "Business Economics-II: "Foreign Exchange Market"Document19 pages"Business Economics-II: "Foreign Exchange Market"Himani ShahNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Recommend Market Entry Strategy For Wildgood Into The Mexico MarketDocument25 pagesRecommend Market Entry Strategy For Wildgood Into The Mexico MarketThiên Phong Trần100% (1)

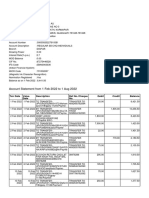

- Account Statement From 1 Feb 2022 To 1 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Feb 2022 To 1 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceFIRDUS ALINo ratings yet

- BIBM Academic 2011Document113 pagesBIBM Academic 2011PaulNo ratings yet

- MarketIntegration 3Document11 pagesMarketIntegration 3Franz Althea BasabeNo ratings yet

- IM Lecture 11Document9 pagesIM Lecture 11sonderNo ratings yet

- Document 6Document2 pagesDocument 6Daniel YaremenkoNo ratings yet

- Ha 3 2023Document3 pagesHa 3 2023xbdrsk6fbgNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- L-1 & 2 Tax Meaning and TypesDocument29 pagesL-1 & 2 Tax Meaning and TypesSamriti NarangNo ratings yet

- 5 6167880689858379820Document31 pages5 6167880689858379820Siva Prakash50% (2)

- Ss 4Document21 pagesSs 4nt.phuongnhu1912No ratings yet

- Bank Failure: What Are The Bank Failures?Document5 pagesBank Failure: What Are The Bank Failures?Aaftab AhmadNo ratings yet

- Theoretical Frame Work 1Document2 pagesTheoretical Frame Work 1Lourd Amethyst OmanaNo ratings yet

- Digital Marketing Approach, Awareness and StrategiesDocument15 pagesDigital Marketing Approach, Awareness and StrategiesEditor IJTSRDNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)