You might also like

- LCCI 48183 L2 Bookkepping and Accounting May 2017Document44 pagesLCCI 48183 L2 Bookkepping and Accounting May 2017vasoskNo ratings yet

- 2021 June Question Paper L2Document20 pages2021 June Question Paper L2Elena Elena100% (1)

- Pearson LCCI Qualifications Examination Timetable: Date Level 1 Level 2 Level 3 Level 4 Tuesday 12 NovemberDocument1 pagePearson LCCI Qualifications Examination Timetable: Date Level 1 Level 2 Level 3 Level 4 Tuesday 12 NovemberHsu Lai WadeeNo ratings yet

- Corporate Guides MBO RGB 2 PDFDocument24 pagesCorporate Guides MBO RGB 2 PDFvasoskNo ratings yet

- Management Buyouts Efficient Markets Fair Value and Soft Inform PDFDocument51 pagesManagement Buyouts Efficient Markets Fair Value and Soft Inform PDFvasoskNo ratings yet

- Credit Card Company Balance Score CardDocument1 pageCredit Card Company Balance Score Cardps_d12No ratings yet

- Retail Market Feasibility Study For Planned Retail Developments at Potomac Yard Alexandria, VirginiaDocument83 pagesRetail Market Feasibility Study For Planned Retail Developments at Potomac Yard Alexandria, VirginiaJun AlegatoNo ratings yet

- Management Buyouts Efficient Markets Fair Value and Soft Inform PDFDocument51 pagesManagement Buyouts Efficient Markets Fair Value and Soft Inform PDFvasoskNo ratings yet

- Valuation Analysis and StructuredDocument19 pagesValuation Analysis and StructuredvasoskNo ratings yet

- Corporate Guides MBO RGB 2 PDFDocument24 pagesCorporate Guides MBO RGB 2 PDFvasoskNo ratings yet

- Instruments & Aid Modalities in External Actions: DG NearDocument15 pagesInstruments & Aid Modalities in External Actions: DG NearvasoskNo ratings yet

- Sports DiplomacyDocument2 pagesSports DiplomacyvasoskNo ratings yet

- Rain BirdDocument18 pagesRain BirdEve PentsaNo ratings yet

- Internal ControlsDocument17 pagesInternal Controlsmissileshield100% (1)

- Instruments & Aid Modalities in External Actions: DG NearDocument15 pagesInstruments & Aid Modalities in External Actions: DG NearvasoskNo ratings yet

- F1 Accounting Exam NotesDocument20 pagesF1 Accounting Exam NotesMarlyn RichardsNo ratings yet

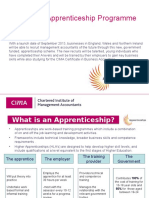

- Apprenticeship Summary 2013Document8 pagesApprenticeship Summary 2013vasoskNo ratings yet

- Charge Out Rate PresentationDocument10 pagesCharge Out Rate PresentationvasoskNo ratings yet

- Methodological Manual SportDocument56 pagesMethodological Manual SportvasoskNo ratings yet

- RBWP 6 Instruction MDocument11 pagesRBWP 6 Instruction MvasoskNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- KEY - Unit 12 Test ReviewDocument4 pagesKEY - Unit 12 Test ReviewHayden MulnixNo ratings yet

- Apostila de AseDocument20 pagesApostila de AseOdair Pereira Dos SantosNo ratings yet

- The Freemason S Monitor-Thomas Smith WebbDocument335 pagesThe Freemason S Monitor-Thomas Smith WebbJORGE LUIZ DE A LINSNo ratings yet

- Permutations and CombinationsDocument15 pagesPermutations and CombinationsThe Rock100% (1)

- Journal No.1:: My Personal TimelineDocument5 pagesJournal No.1:: My Personal TimelineSheena ChanNo ratings yet

- Listening Cd1Document7 pagesListening Cd1Iulian Teodor0% (1)

- Civil Engineer ResumeDocument3 pagesCivil Engineer ResumeRohan Dutt SharmaNo ratings yet

- Process States and Memory Management LabDocument8 pagesProcess States and Memory Management LabJámesNo ratings yet

- Using The PNR Curve To Convert Effort To ScheduleDocument2 pagesUsing The PNR Curve To Convert Effort To ScheduleRajan SainiNo ratings yet

- I+ME ACTIA SAE J2534 Support Release NotesDocument4 pagesI+ME ACTIA SAE J2534 Support Release NotesJose AGNo ratings yet

- Computer QuizDocument31 pagesComputer QuizYOGESH CHHAGANRAO MULEYNo ratings yet

- THEORY Transformation Question BankDocument7 pagesTHEORY Transformation Question Bankpankaj12345katreNo ratings yet

- Sappress Interface ProgrammingDocument0 pagesSappress Interface ProgrammingEfrain OyarceNo ratings yet

- The Historic 7Th March Speech of Bangabandhu Sheikh Mujibur RahmanDocument31 pagesThe Historic 7Th March Speech of Bangabandhu Sheikh Mujibur RahmanSanzid Ahmed ShaqqibNo ratings yet

- Rekha RaniDocument2 pagesRekha RaniSANDEEP SinghNo ratings yet

- Physical Education 1Document25 pagesPhysical Education 1Kynna Devera Dela CruzNo ratings yet

- Theoryt. PR.: of Birth H-GHRDocument1 pageTheoryt. PR.: of Birth H-GHRSanjay TripathiNo ratings yet

- 3GPP LTE Positioning Protocol (LPP)Document115 pages3GPP LTE Positioning Protocol (LPP)dgonzalezmartinNo ratings yet

- Human Resource ManagementDocument18 pagesHuman Resource Managementsamruddhi_khale67% (3)

- Purpose Meaning MeaninginlifeDocument2 pagesPurpose Meaning MeaninginlifeTaufik GeodetikNo ratings yet

- DLL Mtb-Mle3 Q2 W2Document6 pagesDLL Mtb-Mle3 Q2 W2MAUREEN GARCIANo ratings yet

- C Programming Viva Questions for InterviewsDocument5 pagesC Programming Viva Questions for InterviewsParandaman Sampathkumar SNo ratings yet

- Database AdministrationDocument12 pagesDatabase AdministrationjayNo ratings yet

- ABAP - Dynamic Variant Processing With STVARVDocument12 pagesABAP - Dynamic Variant Processing With STVARVrjcamorim100% (1)

- wk8 Activity PresentationDocument13 pageswk8 Activity Presentationapi-280934506No ratings yet

- Arithmetic SequencesDocument3 pagesArithmetic SequencestuvvacNo ratings yet

- G10 Q3 PPT3Document20 pagesG10 Q3 PPT3Ma. Shiela Mira NarceNo ratings yet

- 1 ECI 2015 Final ProgramDocument122 pages1 ECI 2015 Final ProgramDenada Florencia LeonaNo ratings yet

- Session 1 - Introduction To HIP 2017Document18 pagesSession 1 - Introduction To HIP 2017teachernizz100% (3)

- Chem 315 - Lab 6 - Simple and Fractional DistilationDocument27 pagesChem 315 - Lab 6 - Simple and Fractional DistilationkNo ratings yet