You might also like

- Investment Analysis and Tri Star Lockheed - FULL FINALDocument8 pagesInvestment Analysis and Tri Star Lockheed - FULL FINALCheytan Thakar100% (3)

- Locheed Case Study Group 1Document9 pagesLocheed Case Study Group 1Michael DevereauxNo ratings yet

- Lockheed Tristar Case Study 11020241041Document19 pagesLockheed Tristar Case Study 11020241041R Harika Reddy100% (7)

- Lockheed Tristar Case SolutionDocument3 pagesLockheed Tristar Case SolutionPrakash Nishtala100% (1)

- Assignment 2 Lockheed CaseDocument6 pagesAssignment 2 Lockheed CaseBob MarlowNo ratings yet

- Investment Analysis - Lockheed Tri-StarDocument2 pagesInvestment Analysis - Lockheed Tri-Staraclink88100% (1)

- Assignment - Group 6 - Case Analysis (Investment Analysis and Lockheed Tristar)Document6 pagesAssignment - Group 6 - Case Analysis (Investment Analysis and Lockheed Tristar)Rajat Gupta100% (4)

- Lockheed Case SolutionDocument3 pagesLockheed Case SolutionKashish SrivastavaNo ratings yet

- Lockheed Tristar Case Similar SolutionDocument12 pagesLockheed Tristar Case Similar SolutionguruprasadkudvaNo ratings yet

- Lockheed Tristar ProjectDocument1 pageLockheed Tristar ProjectDurgaprasad VelamalaNo ratings yet

- Tristar Case Sol.Document4 pagesTristar Case Sol.Niketa JaiswalNo ratings yet

- The Super Project: Mark Smukler, Griffin Meyer & Estefania GarciaDocument8 pagesThe Super Project: Mark Smukler, Griffin Meyer & Estefania GarciaMark SmuklerNo ratings yet

- FM Assignment 2 IDocument2 pagesFM Assignment 2 Irahul gargNo ratings yet

- Hanson CaseDocument11 pagesHanson Casegharelu10No ratings yet

- USX CorporationDocument13 pagesUSX Corporationrockysanjit0% (4)

- Case AnalysisDocument5 pagesCase AnalysisShrijaSrivNo ratings yet

- Samanvya BuildingDocument5 pagesSamanvya BuildingShiladitya Swarnakar0% (1)

- Case Study On Marico IndustriesDocument12 pagesCase Study On Marico IndustriesTrilochan MohantaNo ratings yet

- Sai Coating CaseDocument7 pagesSai Coating CaseSreejith MadhavNo ratings yet

- Case 7 - London Millennium Dome: Profit Revenues - CostsDocument7 pagesCase 7 - London Millennium Dome: Profit Revenues - CostsLauren LeeNo ratings yet

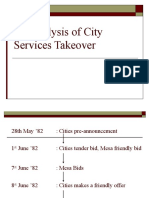

- CitiesService Takeover CaseDocument20 pagesCitiesService Takeover CasesushilkhannaNo ratings yet

- Ford Auto CollectionDocument10 pagesFord Auto Collectionkarishma_sehgal50% (4)

- Can You Suggest Different Actions That The Cofounders Should Have Taken?Document3 pagesCan You Suggest Different Actions That The Cofounders Should Have Taken?Niu WaaleNo ratings yet

- Spyder Student ExcelDocument21 pagesSpyder Student ExcelNatasha PerryNo ratings yet

- Aravind Eye Care SystemDocument4 pagesAravind Eye Care SystemMohammed Hammad RizviNo ratings yet

- Goodyear AquatredDocument2 pagesGoodyear AquatredSaloniNo ratings yet

- The O. M. Scott & Sons CompanyDocument4 pagesThe O. M. Scott & Sons Companycarolina120209100% (1)

- De Beers Group: Marketing Diamonds To Millennials - AnalysisDocument6 pagesDe Beers Group: Marketing Diamonds To Millennials - AnalysisMalielMaleo YTchannelNo ratings yet

- Meagal Stelplast - Steering A New Path - Case Study 1Document9 pagesMeagal Stelplast - Steering A New Path - Case Study 1CH NAIRNo ratings yet

- Forecasting Case - XlxsDocument8 pagesForecasting Case - Xlxsmayank.dce123No ratings yet

- Wills Lifestyle Group1 Section2Document5 pagesWills Lifestyle Group1 Section2vignesh asaithambiNo ratings yet

- Goodyear - Group 3Document4 pagesGoodyear - Group 3Prateek Vijaivargia0% (1)

- L&T DemergerDocument28 pagesL&T DemergerabcdeffabcdefNo ratings yet

- New Heritage Doll Company Capital BudgetDocument5 pagesNew Heritage Doll Company Capital BudgetCarlosNo ratings yet

- Final Version of Goodyear Tire CaseDocument7 pagesFinal Version of Goodyear Tire Casekfrench91100% (1)

- Problem Set 2Document2 pagesProblem Set 2Rithesh KNo ratings yet

- Sport Obermeyer CaseDocument4 pagesSport Obermeyer CaseNamita DeyNo ratings yet

- Spyder Active SportsDocument12 pagesSpyder Active SportsShubham SharmaNo ratings yet

- Making SMaL Big: SMaL Camera TechnologiesDocument28 pagesMaking SMaL Big: SMaL Camera Technologiesattar11No ratings yet

- Flyrock TyresDocument2 pagesFlyrock TyresPranshu Agrawal100% (2)

- Lockheed Case WriteUpDocument12 pagesLockheed Case WriteUppratappranayNo ratings yet

- Investment Banking: Individual Assignment 2Document5 pagesInvestment Banking: Individual Assignment 2Aakash Ladha100% (3)

- Innovation Done by CompanyDocument15 pagesInnovation Done by Companyndim betaNo ratings yet

- Bata Aradhana 2Document26 pagesBata Aradhana 2Aradhana DixitNo ratings yet

- Suzlon Strategic AnalysisDocument78 pagesSuzlon Strategic AnalysisGargiNM88% (24)

- Bio TechDocument9 pagesBio TechDavid Fluky FlukyNo ratings yet

- Wilkins, A Zurn Company: Group 7Document6 pagesWilkins, A Zurn Company: Group 7Aditya Meena DoraiburuNo ratings yet

- Case Study On Hindalco Acquire NovelisDocument13 pagesCase Study On Hindalco Acquire Novelissahilagl23_121905585No ratings yet

- Ducati CaseStudyDocument4 pagesDucati CaseStudySparsh Gupta100% (1)

- Cipla LTD: Company AnalysisDocument13 pagesCipla LTD: Company AnalysisDante DonNo ratings yet

- Chapter 4 SlidesDocument71 pagesChapter 4 SlidesShivi Shrivastava75% (4)

- Case Analysis Landmark FacilityDocument25 pagesCase Analysis Landmark Facilitystark100% (1)

- Computron CaseDocument4 pagesComputron CaseZafar Ibrahim (M20MS074)No ratings yet

- SVCM - Group 4 - Case 3Document2 pagesSVCM - Group 4 - Case 3NehaTaneja0% (1)

- Wintel AnalysisDocument11 pagesWintel AnalysisSrikanth Kumar Konduri100% (2)

- Investment Analysis & Lockheed Tri Star Solutions (A)Document4 pagesInvestment Analysis & Lockheed Tri Star Solutions (A)SamratNo ratings yet

- Chapter 10 SolutionsDocument9 pagesChapter 10 Solutionsaroddddd23No ratings yet

- Investment Analysis and Lookheed Tri Star Case StudyDocument5 pagesInvestment Analysis and Lookheed Tri Star Case StudyShabbar RazaNo ratings yet

- PSB Tutorial Solutions Week 2Document14 pagesPSB Tutorial Solutions Week 2Iqtidar KhanNo ratings yet

- NPV NPV: SolutionDocument13 pagesNPV NPV: SolutionMaria Princess Mae MatzaNo ratings yet

- International Commercial ArbitrationDocument4 pagesInternational Commercial ArbitrationKshitij GuptaNo ratings yet

- BurberryDocument5 pagesBurberryKshitij GuptaNo ratings yet

- Intel Inside CaseDocument37 pagesIntel Inside CaseKshitij Gupta100% (1)

- Industry Analysis Report On SolarDocument10 pagesIndustry Analysis Report On SolarKshitij GuptaNo ratings yet

- Netflix Case Submission Group 3Document5 pagesNetflix Case Submission Group 3Kshitij Gupta100% (1)

- Elie Saab Case AnalysisDocument3 pagesElie Saab Case AnalysisKshitij GuptaNo ratings yet

- NetflixDocument9 pagesNetflixKshitij GuptaNo ratings yet

- Charles and KeithDocument3 pagesCharles and KeithKshitij GuptaNo ratings yet

- Kone Case AnalysisDocument4 pagesKone Case AnalysisKshitij GuptaNo ratings yet

- Facebook FinalDocument55 pagesFacebook FinalKshitij GuptaNo ratings yet

- Coffee Industry Stakeholders: SmallholderDocument3 pagesCoffee Industry Stakeholders: SmallholderKshitij GuptaNo ratings yet

- PG CaseDocument1 pagePG CaseKshitij GuptaNo ratings yet

- PEPSI COLA Case AnalysisDocument3 pagesPEPSI COLA Case AnalysisKshitij Gupta0% (1)

- Business Communication in JapanDocument17 pagesBusiness Communication in JapanKshitij GuptaNo ratings yet

- The Infulence of Leadership Styles On Organisational Performance of Logistics CompanyDocument23 pagesThe Infulence of Leadership Styles On Organisational Performance of Logistics CompanyKshitij GuptaNo ratings yet

- The Role of Leadership Management in Promoting Supply Chain ManagementDocument14 pagesThe Role of Leadership Management in Promoting Supply Chain ManagementKshitij GuptaNo ratings yet

- P&G Benefits of CRMDocument2 pagesP&G Benefits of CRMKshitij GuptaNo ratings yet

- The Infulence of Leadership Styles On Organisational Performance of Logistics CompanyDocument23 pagesThe Infulence of Leadership Styles On Organisational Performance of Logistics CompanyKshitij GuptaNo ratings yet

- Test Bank For CH1 - CH2Document15 pagesTest Bank For CH1 - CH2passemmoresNo ratings yet

- Form MGT 7 27112018 SignedDocument15 pagesForm MGT 7 27112018 SignedBhavin SagarNo ratings yet

- Amalgamation and Valuation by CA RajDocument72 pagesAmalgamation and Valuation by CA Rajkoppineni srikanthNo ratings yet

- Transcript - Mike Green - Perils of Passive IndexationDocument24 pagesTranscript - Mike Green - Perils of Passive IndexationWilhelm BeekmanNo ratings yet

- Fixed Income Securities:, 645 With Face Value of $100, 000Document34 pagesFixed Income Securities:, 645 With Face Value of $100, 000Joaquín Norambuena EscalonaNo ratings yet

- Goldman Funds SicavDocument658 pagesGoldman Funds SicavThanh NguyenNo ratings yet

- United Tractors (UNTR IJ) : Regional Morning NotesDocument5 pagesUnited Tractors (UNTR IJ) : Regional Morning NotesAmirul AriffNo ratings yet

- Auditing Problems3Document32 pagesAuditing Problems3Kimberly Milante100% (2)

- Echange Rate Mechanism: 1. Direct Quote 2. Indirect QuoteDocument4 pagesEchange Rate Mechanism: 1. Direct Quote 2. Indirect QuoteanjankumarNo ratings yet

- Main Exam 2014-Sol-1Document7 pagesMain Exam 2014-Sol-1Diego AguirreNo ratings yet

- Financial Accounting and Reporting Ii Final Quiz 2/3Document7 pagesFinancial Accounting and Reporting Ii Final Quiz 2/3jemsNo ratings yet

- Ebook Corporate Financial Accounting PDF Full Chapter PDFDocument67 pagesEbook Corporate Financial Accounting PDF Full Chapter PDFmyrtle.sampson431100% (27)

- CFT IchimokuDocument1 pageCFT IchimokuGlenden KhewNo ratings yet

- Table 2.1 Samsung Debt Ratio Annual Report 2012-2016 (Measured in Thousand USD)Document6 pagesTable 2.1 Samsung Debt Ratio Annual Report 2012-2016 (Measured in Thousand USD)Intan IntongNo ratings yet

- QQ Test 1 Dec2022Document4 pagesQQ Test 1 Dec2022WAN MOHAMAD ANAS WAN MOHAMADNo ratings yet

- RISK Management CASE STUDY - 2022Document4 pagesRISK Management CASE STUDY - 2022BobbyNo ratings yet

- Ishares U.S. ETF Product ListDocument12 pagesIshares U.S. ETF Product ListFedeGarayNo ratings yet

- Week3Document26 pagesWeek3saqib khanNo ratings yet

- Cash and Receivable Management With SolutionsDocument3 pagesCash and Receivable Management With SolutionsRandy ManzanoNo ratings yet

- Assignment Financial Management RVSDDocument10 pagesAssignment Financial Management RVSDY.Nirmala YellamalaiNo ratings yet

- Green TransformationDocument17 pagesGreen TransformationCissiVRNo ratings yet

- AP Preweek (B44)Document62 pagesAP Preweek (B44)LeiNo ratings yet

- Winning Moves - PDF VersionDocument343 pagesWinning Moves - PDF VersionHichemNo ratings yet

- Using Solvency II To Implement IFRSDocument40 pagesUsing Solvency II To Implement IFRSМансур ШарафутдиновNo ratings yet

- Chapte R: Dividend TheoryDocument19 pagesChapte R: Dividend TheoryArunim MehrotraNo ratings yet

- Balance Sheet of JK Tyre and IndustriesDocument4 pagesBalance Sheet of JK Tyre and IndustriesHimanshu MangeNo ratings yet

- Minority InterestDocument1 pageMinority Interestankur4042007No ratings yet

- ISB Essays Pre-FinalDocument4 pagesISB Essays Pre-FinalRishabh JhunjhunwalaNo ratings yet

- Bongaigaon Ref - FinanDocument10 pagesBongaigaon Ref - FinansdNo ratings yet

- Mergers & Acquisitions: Question Banks Varsha ViraniDocument3 pagesMergers & Acquisitions: Question Banks Varsha ViraniAnkit Patel100% (1)