You might also like

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Financial AccountingDocument1,056 pagesFinancial AccountingCalmguy Chaitu96% (28)

- Financial Accounting Reporting, Analysis and Decision Making, 6th Australian EditionDocument1,215 pagesFinancial Accounting Reporting, Analysis and Decision Making, 6th Australian Editionvenkatachalam radhakrishnan100% (6)

- International Accounting Standards: from UK standards to IAS, an accelerated route to understanding the key principles of international accounting rulesFrom EverandInternational Accounting Standards: from UK standards to IAS, an accelerated route to understanding the key principles of international accounting rulesRating: 3.5 out of 5 stars3.5/5 (2)

- IFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsFrom EverandIFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsRating: 4 out of 5 stars4/5 (11)

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionFrom EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNo ratings yet

- Financial Reporting Volume-IDocument860 pagesFinancial Reporting Volume-IMayank Parekh100% (3)

- Financial Reporting Vol. 2Document884 pagesFinancial Reporting Vol. 2Mayank Jain100% (5)

- Financial Reporting Analysis 2 EdgDocument315 pagesFinancial Reporting Analysis 2 EdgPeter Snell100% (1)

- Advanced Accounting Vol. IDocument944 pagesAdvanced Accounting Vol. ISrinivasa Rao Bandlamudi89% (9)

- Financial AnalysisDocument44 pagesFinancial AnalysisHeap Ke Xin100% (3)

- Managerial AccountingDocument550 pagesManagerial Accountingriya toteja100% (11)

- Principles of Accounting, Volume 1 - Financial Accounting PDFDocument1,055 pagesPrinciples of Accounting, Volume 1 - Financial Accounting PDFThanh Huyền Nguyễn64% (11)

- Accounting For All-1Document641 pagesAccounting For All-1Cristina Covaciu100% (4)

- IfrsDocument273 pagesIfrsmargery_bumagat100% (10)

- Accounting Vol - IIDocument296 pagesAccounting Vol - IISrinivasa Rao Bandlamudi67% (3)

- Financial AccountingDocument844 pagesFinancial AccountingAkash Talwar92% (50)

- Financial Statement AnalysisDocument50 pagesFinancial Statement AnalysisHannahPojaFeria90% (10)

- Principles of Cost Accounting Epub PDFDocument432 pagesPrinciples of Cost Accounting Epub PDFFatima andleeb100% (7)

- Principles of Financial Accounting PDFDocument318 pagesPrinciples of Financial Accounting PDFRalph Aries Almeyda Alvarez100% (2)

- Laws Essentials of Financial Management v7Document186 pagesLaws Essentials of Financial Management v7hshshdhd100% (1)

- Financial Accounting TextbookDocument905 pagesFinancial Accounting TextbookLikamva Mgqamqho100% (1)

- Managerial Accounting PDFDocument539 pagesManagerial Accounting PDFMuhammad makhrojal97% (31)

- Complete: AccountingDocument47 pagesComplete: AccountingKamranKhan88% (8)

- Cost Accounting & Financial Management Vol. IDocument640 pagesCost Accounting & Financial Management Vol. Iseektheraj100% (6)

- Accounting NotesDocument66 pagesAccounting NotesShashank Gadia71% (17)

- Financial Accounting Volume 1 Chapter 1 Kieso PDFDocument46 pagesFinancial Accounting Volume 1 Chapter 1 Kieso PDFCitra Riansyah100% (1)

- 03 04 Analysis Financial StatementDocument216 pages03 04 Analysis Financial StatementShanique Y. Harnett100% (1)

- IFRS Study MaterialDocument687 pagesIFRS Study MaterialBin Saadun78% (9)

- Cost Accounting Vol. IIDocument464 pagesCost Accounting Vol. IISrinivasa Rao Bandlamudi96% (24)

- Financial Management Volume - IDocument522 pagesFinancial Management Volume - ISrinivasa Rao Bandlamudi80% (5)

- Managerial Accounting An Introduction To Concepts Methods and Uses PDFDocument624 pagesManagerial Accounting An Introduction To Concepts Methods and Uses PDFLeojelaineIgcoy100% (6)

- Understanding The Income StatementDocument4 pagesUnderstanding The Income Statementluvujaya100% (1)

- Cost Accounting Vol. IDocument691 pagesCost Accounting Vol. ISrinivasa Rao Bandlamudi88% (8)

- IFRS in Your Pocket 2021Document145 pagesIFRS in Your Pocket 2021Rob BakerNo ratings yet

- Financial Statement AnalysisDocument28 pagesFinancial Statement AnalysisSachin Methree75% (4)

- FINANCIAL ACCOUNTING IFRS EDITION SLIDES ch02Document51 pagesFINANCIAL ACCOUNTING IFRS EDITION SLIDES ch02salmanyz6100% (2)

- Certified Public Accountant Course Book Unit 1 FinanceDocument297 pagesCertified Public Accountant Course Book Unit 1 Financeumer12100% (2)

- Introduction To Financial AccountingDocument11 pagesIntroduction To Financial AccountingRubab Khalid100% (1)

- Intermediate Accounting Test Bank Chapter 18Document3 pagesIntermediate Accounting Test Bank Chapter 18Magdy Kamel33% (3)

- CAF7-Financial Accounting and Reporting II - QuestionbankDocument250 pagesCAF7-Financial Accounting and Reporting II - QuestionbankEvan Jones100% (7)

- Accounting For Managers Canadian EditionDocument535 pagesAccounting For Managers Canadian Editiondrankitamayekar83% (23)

- Introduction To Cost AccountingDocument30 pagesIntroduction To Cost AccountingParamjit Sharma100% (18)

- Management AccountingDocument255 pagesManagement AccountingFradrick100% (8)

- Wey AP 8e Ch01Document47 pagesWey AP 8e Ch01Bintang RahmadiNo ratings yet

- Kieso Chapter 1 SlideDocument61 pagesKieso Chapter 1 SlideErni RohmawatiNo ratings yet

- Accounting Principle Kieso 8e - Ch01Document47 pagesAccounting Principle Kieso 8e - Ch01Sania M. JayantiNo ratings yet

- Accounting in Action: Accounting Principles, Ninth EditionDocument51 pagesAccounting in Action: Accounting Principles, Ninth EditionHusni Rasyidin CervinnyNo ratings yet

- Accounting in ActionDocument62 pagesAccounting in ActionbortycanNo ratings yet

- Accounting in Action: TopicDocument20 pagesAccounting in Action: TopicJannah Amir HassanNo ratings yet

- CH 1 Session IDocument27 pagesCH 1 Session IOkthalia AdamNo ratings yet

- Chapter 1 ACCOUNTING IN ACTIONDocument61 pagesChapter 1 ACCOUNTING IN ACTIONWendy Priscilia Manayang100% (1)

- The Essentials of Finance and Accounting for Nonfinancial ManagersFrom EverandThe Essentials of Finance and Accounting for Nonfinancial ManagersRating: 5 out of 5 stars5/5 (1)

- CH 01Document64 pagesCH 01Kh H100% (1)

- Understanding Business Accounting For DummiesFrom EverandUnderstanding Business Accounting For DummiesRating: 3.5 out of 5 stars3.5/5 (8)

- Chapter - 1 Accounting in ActionDocument19 pagesChapter - 1 Accounting in ActionfuriousTaherNo ratings yet

- FORECLOSURE Response To JP Morgan Chase ForeclosureDocument102 pagesFORECLOSURE Response To JP Morgan Chase ForeclosureLAUREN J TRATAR96% (23)

- Sarfaesi ActDocument7 pagesSarfaesi ActBhakti Bhushan MishraNo ratings yet

- Ass 3 Answer Key01Document2 pagesAss 3 Answer Key01JAN ERWIN LACUESTANo ratings yet

- Chapter 1 The Conceptual Framework: Answer 1Document11 pagesChapter 1 The Conceptual Framework: Answer 1samuel_dwumfourNo ratings yet

- Introduction To Commercial Real Estate DebtDocument11 pagesIntroduction To Commercial Real Estate Debtsm1205No ratings yet

- Investor Document Package - Borrower Dependent Notes 1Document87 pagesInvestor Document Package - Borrower Dependent Notes 1api-274293476No ratings yet

- Credit TransactionsDocument46 pagesCredit TransactionsKyla DabalmatNo ratings yet

- Student Loan Debt 1Document10 pagesStudent Loan Debt 1api-483681351No ratings yet

- Zacarias Vs Revilla DigestDocument2 pagesZacarias Vs Revilla DigestAnonymous bBBpEOG9No ratings yet

- Illustrative LBO AnalysisDocument21 pagesIllustrative LBO AnalysisBrian DongNo ratings yet

- BOND MARKET & PREFERRED STOCKS in BANGLADESHDocument39 pagesBOND MARKET & PREFERRED STOCKS in BANGLADESHFerdous Mahmud Shaon100% (1)

- Insolvency and Bankruptcy Code ChallengeDocument33 pagesInsolvency and Bankruptcy Code Challengeprakhar singhNo ratings yet

- 99Document23 pages99mary jane garcinesNo ratings yet

- MTGE CheatsheetDocument2 pagesMTGE CheatsheetandrewzkyNo ratings yet

- Winding Up of Banking CompaniesDocument18 pagesWinding Up of Banking CompaniesSandeep Bhosale100% (5)

- Interest Agreement (For EBLR Based Loans)Document3 pagesInterest Agreement (For EBLR Based Loans)brijendra1270% (1)

- 15 Engineering Economy SolutionsDocument4 pages15 Engineering Economy SolutionsKristian Erick Ofiana Rimas0% (1)

- United Malayan Banking Corp BHD V Ernest CheDocument13 pagesUnited Malayan Banking Corp BHD V Ernest ChenestleomegasNo ratings yet

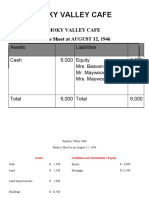

- Smoky Valley CafeDocument3 pagesSmoky Valley CafeRajkumar KrishnamoorthyNo ratings yet

- Personal Finance Chapter 4 TestDocument4 pagesPersonal Finance Chapter 4 Testapi-548712254No ratings yet

- Numbers and Statistics: Posted On April 22, 2008by LzhgladiatorDocument3 pagesNumbers and Statistics: Posted On April 22, 2008by LzhgladiatorЮлияNo ratings yet

- New Charts of Insolvency Bankruptcy Code 2016 PDFDocument9 pagesNew Charts of Insolvency Bankruptcy Code 2016 PDFDeepak WadhwaNo ratings yet

- Ak - Keu (Problem)Document51 pagesAk - Keu (Problem)Vivy DNo ratings yet

- Afar 2702 Corporate LiquidationDocument35 pagesAfar 2702 Corporate Liquidationlijeh312No ratings yet

- Unit 5: Ind As 111: Joint ArrangementsDocument26 pagesUnit 5: Ind As 111: Joint ArrangementsDheeraj TurpunatiNo ratings yet

- IF You Want To Purchase This and Any Other Then:-Contact Us atDocument50 pagesIF You Want To Purchase This and Any Other Then:-Contact Us atJolina AynganNo ratings yet

- MERS V Cabrera Order of Dismissal Judge Jon Gordon Miami Dade Co FLDocument17 pagesMERS V Cabrera Order of Dismissal Judge Jon Gordon Miami Dade Co FLWilliam A. Roper Jr.No ratings yet

- IcrddcDocument7 pagesIcrddcapi-213789026No ratings yet

- Student LoanDocument8 pagesStudent LoanCEStampa1No ratings yet

- Debtocracy : On The Title: It Is A Neologism Between Debt and Democracy Since Greece Is The Cradle of DemocracyDocument1 pageDebtocracy : On The Title: It Is A Neologism Between Debt and Democracy Since Greece Is The Cradle of DemocracyEliezer MPianoNo ratings yet