You might also like

- Butrico Manufacturing Corporation Uses A Standard Cost System RDocument2 pagesButrico Manufacturing Corporation Uses A Standard Cost System RAmit PandeyNo ratings yet

- 3.04 CH419A Jovellana Humidification FundamentalsDocument46 pages3.04 CH419A Jovellana Humidification FundamentalsAsh KetchapNo ratings yet

- Unit 6 Unit 6: Learning ObjectivesDocument36 pagesUnit 6 Unit 6: Learning ObjectivesCheryll ElaineNo ratings yet

- Standard Costs and Variance Analysis ExplainedDocument33 pagesStandard Costs and Variance Analysis ExplainedSay the name Pentastic100% (1)

- DIN EN ISO 12944-4 071998-EnDocument29 pagesDIN EN ISO 12944-4 071998-EnChristopher MendozaNo ratings yet

- USOnline PayslipDocument2 pagesUSOnline PayslipTami SariNo ratings yet

- CounterclaimDocument53 pagesCounterclaimTorrentFreak_No ratings yet

- The Amtasiddhi Hahayogas Tantric Buddh PDFDocument14 pagesThe Amtasiddhi Hahayogas Tantric Buddh PDFalmadebuenosaires100% (1)

- Al Fara'aDocument56 pagesAl Fara'azoinasNo ratings yet

- FIMA 40023 Security Analysis FinalsDocument14 pagesFIMA 40023 Security Analysis FinalsPrincess ErickaNo ratings yet

- W6-Module Concept of Income-Part 1Document14 pagesW6-Module Concept of Income-Part 1Danica VetuzNo ratings yet

- Pasion, Kaye Lianne G. Relos, Yella Mae P. Santos, Monica Sophia LDocument32 pagesPasion, Kaye Lianne G. Relos, Yella Mae P. Santos, Monica Sophia LYella Mae Pariña RelosNo ratings yet

- Two Level Clipping CircuisDocument2 pagesTwo Level Clipping CircuisAvd KishoreNo ratings yet

- Quiz Chapter 6Document1 pageQuiz Chapter 6Beanca GonzalesNo ratings yet

- Chapter 6 Practice QuizDocument5 pagesChapter 6 Practice QuizJialu GaoNo ratings yet

- Gyroscopic InstrumentsDocument23 pagesGyroscopic InstrumentsRobin ForbesNo ratings yet

- 1 - CPAR - Audit of Inventory - Theo×ProbDocument5 pages1 - CPAR - Audit of Inventory - Theo×ProbMargaux CornetaNo ratings yet

- Name: - Section: - Schedule: - Class Number: - DateDocument7 pagesName: - Section: - Schedule: - Class Number: - DateKath DeguzmanNo ratings yet

- Acctg 100C 08Document2 pagesAcctg 100C 08Maddie ManganoNo ratings yet

- Aud Application 2 - Handout 2 Borrowing Cost (UST)Document2 pagesAud Application 2 - Handout 2 Borrowing Cost (UST)RNo ratings yet

- GOVERNANCE PRELIM QUIZ MergedDocument147 pagesGOVERNANCE PRELIM QUIZ MergedSofia SantosNo ratings yet

- Appropriations of Retained EarningsDocument6 pagesAppropriations of Retained EarningsJessa Mae BanseNo ratings yet

- Rizal Technological University-Accountancy Department (Cost Accounting)Document9 pagesRizal Technological University-Accountancy Department (Cost Accounting)Quartz KrystalNo ratings yet

- Financial Environment Chapter 1 SummaryDocument57 pagesFinancial Environment Chapter 1 Summaryn nNo ratings yet

- Exam2 Solutions 40610 2008Document8 pagesExam2 Solutions 40610 2008blackghostNo ratings yet

- Experimental and Numerical Analysis of Airflow Around A Building Model With An Array of DomesDocument55 pagesExperimental and Numerical Analysis of Airflow Around A Building Model With An Array of Domesmarco_doniseteNo ratings yet

- Chapter 8-Financial Reporting and Management Reporting SystemsDocument8 pagesChapter 8-Financial Reporting and Management Reporting SystemsKwini CBNo ratings yet

- AT03 02 Introduction To Financial Statement Audit and Pre Engagement ActivitiesDocument2 pagesAT03 02 Introduction To Financial Statement Audit and Pre Engagement ActivitiesLuna VNo ratings yet

- Case Study Report: Kansei Engineering: Cebu Institute of Technology UniversityDocument6 pagesCase Study Report: Kansei Engineering: Cebu Institute of Technology UniversityJohannie ClaridadNo ratings yet

- Bouncing LawDocument3 pagesBouncing LawALYSSA MAE ABAAGNo ratings yet

- Facility layout types for different businessesDocument2 pagesFacility layout types for different businessesnicolearetano417No ratings yet

- MCQ (New Topics-Special Laws) - PartDocument1 pageMCQ (New Topics-Special Laws) - PartJEP WalwalNo ratings yet

- W4 Module 4 FINANCIAL RATIOS Part 2BDocument12 pagesW4 Module 4 FINANCIAL RATIOS Part 2BDanica VetuzNo ratings yet

- MAS Compilation of QuestionsDocument21 pagesMAS Compilation of QuestionsHazel Joy GaboNo ratings yet

- Chapter 1Document45 pagesChapter 1Zedie Leigh VioletaNo ratings yet

- MULTIPLE CHOICE: Write Your Answer On The Space Provided Before Each Number. Write CAPITAL LETTER. ErasureDocument2 pagesMULTIPLE CHOICE: Write Your Answer On The Space Provided Before Each Number. Write CAPITAL LETTER. ErasurewivadaNo ratings yet

- Histology Module 1 Types of EpitheliumDocument13 pagesHistology Module 1 Types of EpitheliumPia CincoNo ratings yet

- BS Accountancy Qualifying Exam: Management Advisory ServicesDocument7 pagesBS Accountancy Qualifying Exam: Management Advisory ServicesMae Ann RaquinNo ratings yet

- Comparison of IAS 7 and PAS 7Document2 pagesComparison of IAS 7 and PAS 7Julia Villanueva100% (1)

- FEU Intermediate Accounting 1 MCQ on Biological AssetsDocument4 pagesFEU Intermediate Accounting 1 MCQ on Biological AssetsJimbo ManalastasNo ratings yet

- ACTBFAR Work Text Chapter 11 2T1920 FormattedDocument11 pagesACTBFAR Work Text Chapter 11 2T1920 FormattednuggsNo ratings yet

- 06.module & Task-Share Capital PDFDocument8 pages06.module & Task-Share Capital PDFJohn Lery YumolNo ratings yet

- Statement of Financial Position (Balance Sheet) : Lopez, Erica BS Accountancy 2Document8 pagesStatement of Financial Position (Balance Sheet) : Lopez, Erica BS Accountancy 2Erica LopezNo ratings yet

- Chapter 12: The Strategy of International Business: True / False QuestionsDocument40 pagesChapter 12: The Strategy of International Business: True / False QuestionsQuốc PhúNo ratings yet

- CHAP 15. Audit Sampling For Tests of Controls and Substantive Tests of TranDocument32 pagesCHAP 15. Audit Sampling For Tests of Controls and Substantive Tests of TranNoroNo ratings yet

- CTDI Final Pre-Board Special Laws Only PDFDocument4 pagesCTDI Final Pre-Board Special Laws Only PDFPatricia Marie MercaderNo ratings yet

- C. Inclusions and Exclusions From Gross IncomeDocument10 pagesC. Inclusions and Exclusions From Gross IncomeGreggy BoyNo ratings yet

- M00340020220114128M0034-PT11-12-The Expenditure CycleDocument25 pagesM00340020220114128M0034-PT11-12-The Expenditure CycleriznaldoNo ratings yet

- 3 6 Use The Following Graph For Yolandas Frozen Yogurt Stand To Answer The Questions A Use TheDocument2 pages3 6 Use The Following Graph For Yolandas Frozen Yogurt Stand To Answer The Questions A Use TheCharlotteNo ratings yet

- MAC Material 2Document33 pagesMAC Material 2Blessy Zedlav LacbainNo ratings yet

- Practice Examination in Auditing TheoryDocument28 pagesPractice Examination in Auditing TheoryGabriel PonceNo ratings yet

- Acctg 100C 17Document2 pagesAcctg 100C 17lov3m3No ratings yet

- Toa 123Document13 pagesToa 123fredeksdiiNo ratings yet

- Chapter 1 THE INFORMATION SYSTEM AN ACCOUNTANT'S PERSPECTIVEDocument11 pagesChapter 1 THE INFORMATION SYSTEM AN ACCOUNTANT'S PERSPECTIVEAngela Marie PenarandaNo ratings yet

- 2021 2022 1st Sem Prelim ExamDocument2 pages2021 2022 1st Sem Prelim ExamPHILLIT CLASSNo ratings yet

- Questionnaire: Act112 - Intermediate Accounting IDocument20 pagesQuestionnaire: Act112 - Intermediate Accounting IMichaelNo ratings yet

- CPA Review School Philippines Final Preboard ExamDocument13 pagesCPA Review School Philippines Final Preboard ExamMyAccntNo ratings yet

- Job 114 Job 115 Job 116Document2 pagesJob 114 Job 115 Job 116Wendelyn LingayuNo ratings yet

- Gleim Exam Questions and Explanations Updates To Cost/Managerial AccountingDocument13 pagesGleim Exam Questions and Explanations Updates To Cost/Managerial AccountingEndah DipoyantiNo ratings yet

- Chapter 3 - Tactical Decision MakingDocument37 pagesChapter 3 - Tactical Decision MakingMarvin EduarteNo ratings yet

- Contract of Sales and Negotiable Instruments SummaryDocument19 pagesContract of Sales and Negotiable Instruments SummaryCarlito B. BancilNo ratings yet

- Rizal As A National Hero?Document1 pageRizal As A National Hero?Useless-chan UwUNo ratings yet

- Review 105 - Day 16 P1Document12 pagesReview 105 - Day 16 P1Chronos ChronosNo ratings yet

- Finacc 3 Question Set BDocument9 pagesFinacc 3 Question Set BEza Joy ClaveriasNo ratings yet

- Presentation 1Document32 pagesPresentation 1Ahmed HussainNo ratings yet

- Stats Class 1Document3 pagesStats Class 1naseerf_816259742No ratings yet

- Measures of Spread ExerciseDocument3 pagesMeasures of Spread Exercisenaseerf_816259742No ratings yet

- Computer UsageDocument19 pagesComputer Usagenaseerf_816259742No ratings yet

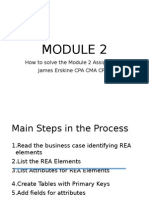

- MODULE 2: HOW TO SOLVE THE MODULE 2 ASSIGNMENTDocument11 pagesMODULE 2: HOW TO SOLVE THE MODULE 2 ASSIGNMENTnaseerf_816259742No ratings yet

- Ch12 ACCG20478 (Cost 2) PPT MMDocument90 pagesCh12 ACCG20478 (Cost 2) PPT MMnaseerf_816259742No ratings yet

- Module 1.2a Diagraming Data Flows - Context DiagramDocument19 pagesModule 1.2a Diagraming Data Flows - Context Diagramnaseerf_816259742No ratings yet

- Spouses Ismael and Teresita Macasaet Vs Spouses Vicente and Rosario MacasaetDocument20 pagesSpouses Ismael and Teresita Macasaet Vs Spouses Vicente and Rosario MacasaetGladys Laureta GarciaNo ratings yet

- Reading Comprehension and Vocabulary PracticeDocument10 pagesReading Comprehension and Vocabulary Practice徐明羽No ratings yet

- Wa0010Document3 pagesWa0010BRANDO LEONARDO ROJAS ROMERONo ratings yet

- Quant Congress - BarCapDocument40 pagesQuant Congress - BarCapperry__mason100% (1)

- BGAS-CSWIP 10 Year Re-Certification Form (Overseas) No LogbookDocument7 pagesBGAS-CSWIP 10 Year Re-Certification Form (Overseas) No LogbookMedel Cay De CastroNo ratings yet

- Esmf 04052017 PDFDocument265 pagesEsmf 04052017 PDFRaju ReddyNo ratings yet

- What Is Taekwondo?Document14 pagesWhat Is Taekwondo?Josiah Salamanca SantiagoNo ratings yet

- European Gunnery's Impact on Artillery in 16th Century IndiaDocument9 pagesEuropean Gunnery's Impact on Artillery in 16th Century Indiaharry3196No ratings yet

- Types of Electronic CommerceDocument2 pagesTypes of Electronic CommerceVivek RajNo ratings yet

- 0500 w16 Ms 13Document9 pages0500 w16 Ms 13Mohammed MaGdyNo ratings yet

- Chua v. CFI DigestDocument1 pageChua v. CFI DigestMae Ann Sarte AchaNo ratings yet

- Globalization Winners and LosersDocument2 pagesGlobalization Winners and Losersnprjkb5r2wNo ratings yet

- Rights of Accused in Libuit v. PeopleDocument3 pagesRights of Accused in Libuit v. PeopleCheska BorjaNo ratings yet

- Public-International-Law Reviewer Isagani Cruz - Scribd 2013 Public International Law (Finals) - Arellano ..Document1 pagePublic-International-Law Reviewer Isagani Cruz - Scribd 2013 Public International Law (Finals) - Arellano ..Lylanie Alexandria Yan GalaNo ratings yet

- Employee Separation Types and ReasonsDocument39 pagesEmployee Separation Types and ReasonsHarsh GargNo ratings yet

- Guidelines: For Submitting A Candidature To OrganiseDocument19 pagesGuidelines: For Submitting A Candidature To OrganiseDan ZoltnerNo ratings yet

- ThangkaDocument8 pagesThangkasifuadrian100% (1)

- Baccmass - ChordsDocument7 pagesBaccmass - ChordsYuan MasudaNo ratings yet

- Apply for Letter of AdministrationDocument5 pagesApply for Letter of AdministrationCharumathy NairNo ratings yet

- Intermediate Accounting 1 - Cash Straight ProblemsDocument3 pagesIntermediate Accounting 1 - Cash Straight ProblemsCzarhiena SantiagoNo ratings yet

- Critical Perspectives On AccountingDocument17 pagesCritical Perspectives On AccountingUmar Amar100% (2)

- AN ORDINANCE ESTABLISHING THE BARANGAY SPECIAL BENEFIT AND SERVICE IMPROVEMENT SYSTEMDocument7 pagesAN ORDINANCE ESTABLISHING THE BARANGAY SPECIAL BENEFIT AND SERVICE IMPROVEMENT SYSTEMRomel VillanuevaNo ratings yet

- Life Member ListDocument487 pagesLife Member Listpuiritii airNo ratings yet

- ERA1209-001 Clarification About Points 18.4 and 18.5 of Annex I of Regulation 2018-545 PDFDocument10 pagesERA1209-001 Clarification About Points 18.4 and 18.5 of Annex I of Regulation 2018-545 PDFStan ValiNo ratings yet

- HertzDocument2 pagesHertzChhavi AnandNo ratings yet