You might also like

- Bom List50klDocument3 pagesBom List50klRafeek ShaikhNo ratings yet

- 125k Receiver DataDocument2 pages125k Receiver DataRafeek ShaikhNo ratings yet

- Spray Drying PlantsDocument3 pagesSpray Drying PlantsRafeek ShaikhNo ratings yet

- Standard Measurement of Painting (Section Area/Metre) For Beams For Channels For Angels (Star Bracing)Document2 pagesStandard Measurement of Painting (Section Area/Metre) For Beams For Channels For Angels (Star Bracing)Rafeek ShaikhNo ratings yet

- Storage Tank Design Calculation - Api 650: Open Cone-RoofDocument1 pageStorage Tank Design Calculation - Api 650: Open Cone-RoofRafeek ShaikhNo ratings yet

- Agitator Vessel Design Costing50klDocument1 pageAgitator Vessel Design Costing50klRafeek ShaikhNo ratings yet

- 50kl Cost Estimation of Storage TankDocument1 page50kl Cost Estimation of Storage TankRafeek ShaikhNo ratings yet

- New 30 KL green silica vessel projectDocument2 pagesNew 30 KL green silica vessel projectRafeek ShaikhNo ratings yet

- MYMT PersonalBudgetWorksheet TrackingWeeklyExpenses Final Version 1 Jan 2004Document7 pagesMYMT PersonalBudgetWorksheet TrackingWeeklyExpenses Final Version 1 Jan 2004gopi100% (2)

- Virus CodeDocument1 pageVirus CodeRafeek ShaikhNo ratings yet

- Painting Work Inquiry-20121205-235314Document2 pagesPainting Work Inquiry-20121205-235314Rafeek ShaikhNo ratings yet

- Chip Plus Handson With Ms WordDocument50 pagesChip Plus Handson With Ms Wordknlyadav8463No ratings yet

- THE SECRETS OUT - How To Hack Yahoo PasswordsDocument1 pageTHE SECRETS OUT - How To Hack Yahoo PasswordsRafeek ShaikhNo ratings yet

- Related FormulaDocument279 pagesRelated FormulaRafeek ShaikhNo ratings yet

- Rotary Dryer Design & Working PrincipleDocument12 pagesRotary Dryer Design & Working PrincipleRafeek ShaikhNo ratings yet

- MKM Solutions Plastic Pyrolysis Plant: Other ProductsDocument4 pagesMKM Solutions Plastic Pyrolysis Plant: Other ProductsRafeek ShaikhNo ratings yet

- Faizaan 5kl With Distillation UnitDocument2 pagesFaizaan 5kl With Distillation UnitRafeek ShaikhNo ratings yet

- Jdi-L11 Liaquat Engineering WorksDocument21 pagesJdi-L11 Liaquat Engineering WorksRafeek ShaikhNo ratings yet

- Ra BillDocument1 pageRa BillRafeek ShaikhNo ratings yet

- Calculating Fault CurrentDocument8 pagesCalculating Fault Currentenghassanain6486No ratings yet

- Motor Power and TorqueDocument4 pagesMotor Power and Torquepippo2378793No ratings yet

- Battery Sizing CalculatorDocument6 pagesBattery Sizing Calculatormfisol2000No ratings yet

- Electrical Panel Load Calculation 22 8 12Document33 pagesElectrical Panel Load Calculation 22 8 12vicent johnNo ratings yet

- Autocad TricksDocument1 pageAutocad TricksRafeek ShaikhNo ratings yet

- Minimum Insulation Resistance Values GuideDocument37 pagesMinimum Insulation Resistance Values GuideHilmy FadlyNo ratings yet

- Pharma Co ListDocument7 pagesPharma Co ListRafeek ShaikhNo ratings yet

- ASME Boiler & Fuel Cell Pressure Vessel Spreadsheets-Content-J AndrewDocument1 pageASME Boiler & Fuel Cell Pressure Vessel Spreadsheets-Content-J AndrewRafeek ShaikhNo ratings yet

- ASME Boiler & Fuel Cell Pressure Vessel Spreadsheets-Content-J AndrewDocument55 pagesASME Boiler & Fuel Cell Pressure Vessel Spreadsheets-Content-J AndrewAravindan Ganesh KumarNo ratings yet

- Home Electrical Bill / Energy Consumption / Electrical Load CalculatorDocument21 pagesHome Electrical Bill / Energy Consumption / Electrical Load Calculatorsrabon1059No ratings yet

- Calculations on an adiabatic continuous dryer processDocument11 pagesCalculations on an adiabatic continuous dryer processBülent KabadayiNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Koyas PerfumeryDocument2 pagesKoyas PerfumeryTANUJ CHAKRABORTYNo ratings yet

- Assignment of Cash ManagementDocument4 pagesAssignment of Cash ManagementHarsh ChauhanNo ratings yet

- TDS RECEIVABLE REPORTDocument4 pagesTDS RECEIVABLE REPORTravibhartia1978No ratings yet

- Aastha Realtors Vendor FormDocument2 pagesAastha Realtors Vendor Formshibani thomasNo ratings yet

- CFI Accounting FactsheetDocument1 pageCFI Accounting FactsheetPirvuNo ratings yet

- 20201213-Statements-9476 - (1) - UnlockedDocument4 pages20201213-Statements-9476 - (1) - UnlockedHamza AzamNo ratings yet

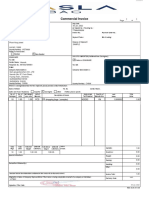

- InvoiceDocument1 pageInvoiceLe NgocNo ratings yet

- Estatement Chase JulyDocument6 pagesEstatement Chase JulyAtta ur RehmanNo ratings yet

- c.11. Filipinas Synthetic Fiber Corp v. CADocument1 pagec.11. Filipinas Synthetic Fiber Corp v. CAArbie LlesisNo ratings yet

- Enrich RezekiDocument6 pagesEnrich RezekiBig DaddyCoolNo ratings yet

- 568 - LLC Tax Return FormDocument7 pages568 - LLC Tax Return FormAndreana Dumpling WilliamsNo ratings yet

- Order Summary PDFDocument4 pagesOrder Summary PDFAlyaa Syafika NadiraNo ratings yet

- Bank ReconciliationDocument6 pagesBank ReconciliationnikNo ratings yet

- Training Program: Organised by Mauritius Revenue Authority Staff AssociationDocument42 pagesTraining Program: Organised by Mauritius Revenue Authority Staff AssociationradhakrishanNo ratings yet

- UnknownDocument1 pageUnknownBSNL BBOVERWIFINo ratings yet

- Grand Central Hotel Pekanbaru VoucherDocument1 pageGrand Central Hotel Pekanbaru VoucherDhani NuswandiNo ratings yet

- MITC Document CustomerDocument14 pagesMITC Document CustomerSwapnil PankeNo ratings yet

- Halal TaxDocument2 pagesHalal TaxNelson IheanachoNo ratings yet

- Customer credit card statement summaryDocument3 pagesCustomer credit card statement summaryLeonardo GarciaNo ratings yet

- Payslip Nov - Sailu1 fINALDocument2 pagesPayslip Nov - Sailu1 fINALChristine HallNo ratings yet

- RESA TAX PreWeek (B43)Document23 pagesRESA TAX PreWeek (B43)MellaniNo ratings yet

- Sol To Tax Chapter10to15 2013 2014Document33 pagesSol To Tax Chapter10to15 2013 2014Jayrick James AriscoNo ratings yet

- PWW Currency Guide enDocument112 pagesPWW Currency Guide enrrajesheeeNo ratings yet

- EY Tax Alert: Malaysian DevelopmentsDocument10 pagesEY Tax Alert: Malaysian DevelopmentsSirius StarNo ratings yet

- Calculate Profit Margins Excel TemplateDocument4 pagesCalculate Profit Margins Excel TemplateMustafa Ricky Pramana SeNo ratings yet

- Deficiency Interest vs. Delinquency Interest. RCU 9.14.12Document2 pagesDeficiency Interest vs. Delinquency Interest. RCU 9.14.12Paul GeorgeNo ratings yet

- Bank Statement: Account HolderDocument2 pagesBank Statement: Account HolderYurii OmeliukhNo ratings yet

- Amazon Tax Information InterviewDocument2 pagesAmazon Tax Information Interviewasad nNo ratings yet

- Tax Planning, Avoidance, and Evasion StrategiesDocument8 pagesTax Planning, Avoidance, and Evasion StrategiesJaydeep KumarNo ratings yet

- What Is Virtual Credit Card?Document6 pagesWhat Is Virtual Credit Card?Suraj Bahadur77% (26)