You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- NIOS Culture NotesDocument71 pagesNIOS Culture Notesmevrick_guy0% (1)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- 01.19 Safe CustodyDocument9 pages01.19 Safe Custodymevrick_guyNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Banking Glossary 2011Document27 pagesBanking Glossary 2011Praneeth Kumar NaganNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Currency Chest Operations GuideDocument10 pagesCurrency Chest Operations Guidemevrick_guyNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- IBPS Interview PrepDocument33 pagesIBPS Interview Prepmevrick_guyNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Top 10 Economic Challenges for Modi GovtDocument17 pagesTop 10 Economic Challenges for Modi Govtmevrick_guyNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Yuva Savings Bank AccountDocument1 pageYuva Savings Bank Accountmevrick_guyNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A StudyDocument12 pagesA Studymevrick_guyNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- 01 21-RBIremittanceDocument11 pages01 21-RBIremittancemevrick_guyNo ratings yet

- 2nd Issue E-Gyan, October-2013Document28 pages2nd Issue E-Gyan, October-2013mevrick_guyNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- BOD EOD ProcessesDocument25 pagesBOD EOD Processesmevrick_guy100% (1)

- 47-Corporate Salary Package - CSPDocument3 pages47-Corporate Salary Package - CSPmevrick_guyNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- State Bank Learning Centre e-gyan Vol 1 Key HighlightsDocument13 pagesState Bank Learning Centre e-gyan Vol 1 Key Highlightsmevrick_guyNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- 01.20 Government BusinessDocument48 pages01.20 Government Businessmevrick_guyNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- BOD EOD ProcessesDocument25 pagesBOD EOD Processesmevrick_guy100% (1)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Generate Multiple Demand Drafts from Deposit AccountDocument40 pagesGenerate Multiple Demand Drafts from Deposit Accountmevrick_guyNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

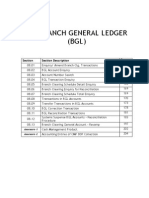

- 8 To 8 Functionality: Section Section DescriptionDocument7 pages8 To 8 Functionality: Section Section Descriptionmevrick_guyNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- 01 08-BGLDocument40 pages01 08-BGLmevrick_guy100% (2)

- 01.09-User System ManagementDocument12 pages01.09-User System Managementmevrick_guyNo ratings yet

- 01.13 ClearingDocument38 pages01.13 Clearingmevrick_guy0% (1)

- 01.14 Maker Checker FunctionalitiesDocument19 pages01.14 Maker Checker Functionalitiesmevrick_guyNo ratings yet

- 01.12 Posting RestrictionsDocument14 pages01.12 Posting Restrictionsmevrick_guyNo ratings yet

- Transaction Processing: Cash, Cheques, TransfersDocument23 pagesTransaction Processing: Cash, Cheques, Transfersmevrick_guyNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 01.03-Deposit Accounts OpeningDocument38 pages01.03-Deposit Accounts Openingmevrick_guy0% (1)

- Manage cash workflow and transactionsDocument21 pagesManage cash workflow and transactionsmevrick_guyNo ratings yet

- Deposit Accounts - Joint Accounts and NomineesDocument30 pagesDeposit Accounts - Joint Accounts and Nomineesmevrick_guyNo ratings yet

- 01.01 IntroductionDocument16 pages01.01 Introductionmevrick_guyNo ratings yet

- 01 02-CifDocument25 pages01 02-Cifmevrick_guyNo ratings yet

- 00.01 PrefaceDocument1 page00.01 Prefacemevrick_guyNo ratings yet

- Trust Receipts LawDocument6 pagesTrust Receipts LawPrinting PandaNo ratings yet

- Dispute over mortgage loan violations and notice of intent to rescindDocument3 pagesDispute over mortgage loan violations and notice of intent to rescindj_west30No ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Judicial NoticeDocument13 pagesJudicial NoticeRobert Salzano100% (2)

- Counter Bautista Estafa bp22Document4 pagesCounter Bautista Estafa bp22Bornok TamolmolNo ratings yet

- Rule 67, 69 and 71Document18 pagesRule 67, 69 and 71Maria Cristina MartinezNo ratings yet

- Tuason v. MachucaDocument2 pagesTuason v. MachucaAdi CruzNo ratings yet

- OUM Bank Liquidity ManagementDocument23 pagesOUM Bank Liquidity ManagementSashiNo ratings yet

- Writing ContractsDocument67 pagesWriting ContractsHisExcellency100% (7)

- Green House and Poly HouseDocument14 pagesGreen House and Poly HouseSubhashBaindha50% (2)

- Land Bank of Th-Wps OfficeDocument1 pageLand Bank of Th-Wps OfficeSaira Mae HayoNo ratings yet

- Britam Insurance Deal DetailsDocument2 pagesBritam Insurance Deal Detailsapi-50425236No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Financial Hardship Letter SampleDocument2 pagesFinancial Hardship Letter SampleWilliam BluntNo ratings yet

- Simple Mortgage DeedDocument3 pagesSimple Mortgage DeedkjapashaNo ratings yet

- Mortel vs. BrundigeDocument12 pagesMortel vs. BrundigeElvin BauiNo ratings yet

- SBI-SME-Checklist MUDRA LoansDocument1 pageSBI-SME-Checklist MUDRA LoansBijay Tiwari50% (2)

- Lease-Contract Rodel CustodioDocument3 pagesLease-Contract Rodel CustodiocamilleNo ratings yet

- SBA Loan ChartDocument2 pagesSBA Loan ChartsbdcwtNo ratings yet

- Sample Qualified Written Request 1Document5 pagesSample Qualified Written Request 1derrick1958100% (2)

- Paglaum Management and Dev't Corp. and Health Marketing Technologies, Inc., Vs Union Bank of The Philippines G.R. No. 179018 April 17, 2013Document2 pagesPaglaum Management and Dev't Corp. and Health Marketing Technologies, Inc., Vs Union Bank of The Philippines G.R. No. 179018 April 17, 2013mjpjore100% (1)

- Pious Obligation of SonDocument9 pagesPious Obligation of SonGagandeepNo ratings yet

- Borrower and Lo To Sign Initial DisclosurDocument110 pagesBorrower and Lo To Sign Initial DisclosurNicola NaunauNo ratings yet

- HARVEY V. HSBC - April Charney Esq. Appeal Brief - PSADocument46 pagesHARVEY V. HSBC - April Charney Esq. Appeal Brief - PSAwinstons2311No ratings yet

- Philippine Supreme Court rules on writ of possession caseDocument12 pagesPhilippine Supreme Court rules on writ of possession casevylletteNo ratings yet

- Indemnity BondDocument3 pagesIndemnity BondMritunjai SinghNo ratings yet

- Research Paper For International FinanceDocument18 pagesResearch Paper For International FinancenanoiNo ratings yet

- Bonds PayableDocument52 pagesBonds PayableJohn Charles Andaya100% (2)

- EjectmentPacket As APPLIED in USDocument23 pagesEjectmentPacket As APPLIED in USdsay88No ratings yet

- Focus On Personal Finance 5Th Edition Kapoor Test Bank Full Chapter PDFDocument67 pagesFocus On Personal Finance 5Th Edition Kapoor Test Bank Full Chapter PDFmiguelstone5tt0f100% (12)

- 84 Dec. Helen ChaitmanDocument19 pages84 Dec. Helen Chaitmanlarry-612445No ratings yet

- Sujitha Resume Underwriter ExperienceDocument3 pagesSujitha Resume Underwriter ExperienceAnil Kumar SadanaNo ratings yet