You might also like

- Business PCL I Fin Session 9&10 Techniques of HedgingDocument13 pagesBusiness PCL I Fin Session 9&10 Techniques of HedgingAashima JainNo ratings yet

- Determinants of Exchange RatesDocument10 pagesDeterminants of Exchange RatesNandhaNo ratings yet

- Determination of Exchange Rates & Balance of PaymentsDocument15 pagesDetermination of Exchange Rates & Balance of PaymentsBivek DahalNo ratings yet

- Eco Prasant InterlinkageDocument5 pagesEco Prasant InterlinkageAnkit AgrawalNo ratings yet

- Prayoga Dwi Nugraha - Summary CH 12 Buku 2Document10 pagesPrayoga Dwi Nugraha - Summary CH 12 Buku 2Prayoga Dwi NugrahaNo ratings yet

- FX Market GuideDocument19 pagesFX Market Guidesaurabh thakurNo ratings yet

- IT Final Ch.6.2023Document12 pagesIT Final Ch.6.2023Amgad ElshamyNo ratings yet

- MF0015 - International Financial Management - Set - 2Document10 pagesMF0015 - International Financial Management - Set - 2Shilpa PokharkarNo ratings yet

- Chapter 4 The Interntional Flow of Funds and Exchange RatesDocument14 pagesChapter 4 The Interntional Flow of Funds and Exchange RatesRAY NICOLE MALINGI100% (1)

- Balance of Payments: UNIT-2Document9 pagesBalance of Payments: UNIT-2naveenNo ratings yet

- FIN 422 (Chapter 2)Document9 pagesFIN 422 (Chapter 2)Sumaiya AfrinNo ratings yet

- Case C8Document6 pagesCase C8Việt Tuấn TrịnhNo ratings yet

- The Balance of Payments, Foreign Exchange Rates and IS-LM-BoP ModelDocument10 pagesThe Balance of Payments, Foreign Exchange Rates and IS-LM-BoP Modelmah rukhNo ratings yet

- Global Financial System: International InstitutionsDocument21 pagesGlobal Financial System: International Institutionsapi-265248190% (1)

- BB106 Unit 9: Balance of Payments TutorialDocument16 pagesBB106 Unit 9: Balance of Payments TutorialLi NiniNo ratings yet

- Topic 4 - The Balance of International PaymentsDocument20 pagesTopic 4 - The Balance of International PaymentsMonique VillaNo ratings yet

- Topic 1 BbalanceofpaymentDocument3 pagesTopic 1 BbalanceofpaymentMohammad TalhaNo ratings yet

- Ibo-1 Em-1Document13 pagesIbo-1 Em-1AtulNo ratings yet

- Quiz AnswerDocument11 pagesQuiz Answercharlie tunaNo ratings yet

- Exchange Rate Determination Challenges LimitationsDocument5 pagesExchange Rate Determination Challenges LimitationsSakshi LodhaNo ratings yet

- Fundamentals of International Finance ExplainedDocument11 pagesFundamentals of International Finance ExplainedChirag KotianNo ratings yet

- Mid-term Practice Q&ADocument5 pagesMid-term Practice Q&AMustafa TotanNo ratings yet

- Determinants of Exchange RateDocument5 pagesDeterminants of Exchange RatedayaksdNo ratings yet

- Bop 2018Document7 pagesBop 2018mba departmentNo ratings yet

- Chapter 4Document19 pagesChapter 4Proveedor Iptv EspañaNo ratings yet

- Factors That Influence Exchange RatesDocument2 pagesFactors That Influence Exchange RatesJoelene ChewNo ratings yet

- module 4Document4 pagesmodule 4vipin kpNo ratings yet

- Balance of PaymentDocument4 pagesBalance of Paymentpriya chauhanNo ratings yet

- International Economics - Key Concepts and TheoriesDocument4 pagesInternational Economics - Key Concepts and TheoriesMarika KovácsNo ratings yet

- Week Two International Financial Organizations and ArrangementsDocument17 pagesWeek Two International Financial Organizations and ArrangementsWanjiku MathuNo ratings yet

- Balance of Payment 1Document8 pagesBalance of Payment 1Wanjiku MathuNo ratings yet

- Module 6 - Interntional Flow of FundsDocument4 pagesModule 6 - Interntional Flow of FundsMICHELLE MILANANo ratings yet

- Determination of Exchange Rates & Balance of PaymentsDocument33 pagesDetermination of Exchange Rates & Balance of Paymentsanji 123100% (8)

- Unit - 5 - ME & IPDocument33 pagesUnit - 5 - ME & IPKishore kumarNo ratings yet

- Class12 Economics2 MacroEconomics Unit06 NCERT TextBook EnglishEditionDocument22 pagesClass12 Economics2 MacroEconomics Unit06 NCERT TextBook EnglishEditionSanjana PrabhuNo ratings yet

- IFM1Document12 pagesIFM1Shaan MahendraNo ratings yet

- Effects of Foreign Exchange Rates On Indian EconomyDocument43 pagesEffects of Foreign Exchange Rates On Indian EconomyMohamed Rizwan0% (1)

- International Monetary and Financial Systems - Chapter-4 MbsDocument62 pagesInternational Monetary and Financial Systems - Chapter-4 MbsArjun MishraNo ratings yet

- Week 7 Openness in Goods and Financial MarketsDocument49 pagesWeek 7 Openness in Goods and Financial MarketsGreg AubinNo ratings yet

- Global Financial System: International InstitutionsDocument15 pagesGlobal Financial System: International Institutionsapi-26524819No ratings yet

- Ge 10Document4 pagesGe 10Lisa LvqiuNo ratings yet

- Ass1 InternationalDocument21 pagesAss1 InternationalAbdulhafiz HajkedirNo ratings yet

- Open Economy Macroeconomics Notes on Balance of Payments, Exchange RatesDocument5 pagesOpen Economy Macroeconomics Notes on Balance of Payments, Exchange RatesAlans TechnicalNo ratings yet

- Int Eco II AssignmentDocument7 pagesInt Eco II AssignmentMosisa ShelemaNo ratings yet

- Assignment 2 (Theories of Exchange Rates - PPP, IFE, IRP)Document6 pagesAssignment 2 (Theories of Exchange Rates - PPP, IFE, IRP)doraemonNo ratings yet

- Currency Exchange RatesDocument5 pagesCurrency Exchange RatesJuan AgudeloNo ratings yet

- Cheat Sheet - CHE374Document26 pagesCheat Sheet - CHE374JoeNo ratings yet

- Balance of Payments - FinalDocument26 pagesBalance of Payments - Finalrania tareqNo ratings yet

- Assignment 2 (Theories of Exchange Rates - PPP, IfE, IRP)Document6 pagesAssignment 2 (Theories of Exchange Rates - PPP, IfE, IRP)doraemonNo ratings yet

- IF Internals 1Document11 pagesIF Internals 1Amith AlphaNo ratings yet

- Open Economy Macroeconomics Class 12 Notes CBSE Macro Economics Chapter 6 PDFDocument5 pagesOpen Economy Macroeconomics Class 12 Notes CBSE Macro Economics Chapter 6 PDFganeshNo ratings yet

- The Balance of Payments and The Exchange RateDocument10 pagesThe Balance of Payments and The Exchange RateOtis MelbournNo ratings yet

- US Capital and Current AccountDocument23 pagesUS Capital and Current Accountsabyasachi_mitraNo ratings yet

- External SectorDocument22 pagesExternal SectorCarlo CanlasNo ratings yet

- The Balance of Payments: Chapter ObjectiveDocument20 pagesThe Balance of Payments: Chapter ObjectiveBigbi KumarNo ratings yet

- Reading Lesson 6Document8 pagesReading Lesson 6AnshumanNo ratings yet

- BSA CORE 6 - Factors Affecting Exchange RatesDocument4 pagesBSA CORE 6 - Factors Affecting Exchange RatesKryzzel JonNo ratings yet

- Exchange RatesDocument32 pagesExchange RatesStuti BansalNo ratings yet

- The Determination of Exchange Rate: BY Annisa Ramadhani Bertha Muhammad Karina Fitri Zahira SalsabellaDocument25 pagesThe Determination of Exchange Rate: BY Annisa Ramadhani Bertha Muhammad Karina Fitri Zahira SalsabellaRatu ShaviraNo ratings yet

- AFC3240 Topic 03 S1 2011Document36 pagesAFC3240 Topic 03 S1 2011sittmoNo ratings yet

- International Parity Relationship: Topic 4Document32 pagesInternational Parity Relationship: Topic 4sittmoNo ratings yet

- AFC3240 Topic 07 S1 2011Document12 pagesAFC3240 Topic 07 S1 2011sittmoNo ratings yet

- AFC3240 Topic 01 S2 2010Document18 pagesAFC3240 Topic 01 S2 2010sittmoNo ratings yet

- AFC3240 NotesDocument18 pagesAFC3240 NotessittmoNo ratings yet

- AFC3240 Topic 08 S1 2011Document24 pagesAFC3240 Topic 08 S1 2011sittmoNo ratings yet

- AFC3240 Topic 09 S1 2011Document17 pagesAFC3240 Topic 09 S1 2011sittmoNo ratings yet

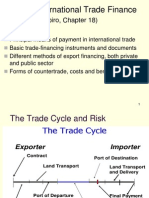

- Topic 2: International Trade Finance: (Reading: Shapiro, Chapter 18)Document15 pagesTopic 2: International Trade Finance: (Reading: Shapiro, Chapter 18)sittmoNo ratings yet

- AFC3240 Topic 06 S1 2011Document27 pagesAFC3240 Topic 06 S1 2011sittmoNo ratings yet

- Sec 03Document24 pagesSec 03sittmoNo ratings yet

- Sec 01Document35 pagesSec 01sittmoNo ratings yet

- Section 2 Section 2 Intervention in Markets Intervention in MarketsDocument18 pagesSection 2 Section 2 Intervention in Markets Intervention in MarketssittmoNo ratings yet

- Sec 04Document32 pagesSec 04sittmoNo ratings yet

- Solving Inhomogenous Recurrence Relations 3Document4 pagesSolving Inhomogenous Recurrence Relations 3sittmoNo ratings yet

- Solving Inhomogenous Recurrence Relations 2Document2 pagesSolving Inhomogenous Recurrence Relations 2sittmoNo ratings yet

- Solving Inhomogenous Recurrence RelationsDocument3 pagesSolving Inhomogenous Recurrence Relationssittmo0% (1)

- Accounts Test - Chapter 1 and 3Document5 pagesAccounts Test - Chapter 1 and 3Vikram KatariaNo ratings yet

- NOTESDocument53 pagesNOTESirahQNo ratings yet

- Chapter 3Document23 pagesChapter 3jannessh100% (2)

- Business Plan Horse RidingDocument39 pagesBusiness Plan Horse RidingJames ZacharyNo ratings yet

- Phuket CaseDocument4 pagesPhuket Casejperez1980100% (1)

- We TubeDocument38 pagesWe TubeGaurav ChikhalikarNo ratings yet

- EBIT EPS AnalysisDocument17 pagesEBIT EPS AnalysisAditya GuptaNo ratings yet

- Final Sip SRDocument40 pagesFinal Sip SRdpusinghNo ratings yet

- Bank Ganesha TBKDocument3 pagesBank Ganesha TBKTam sneakersNo ratings yet

- The Economic Times Wealth - March 27 2023Document26 pagesThe Economic Times Wealth - March 27 2023Bakary DjabyNo ratings yet

- Accounting For ValueDocument15 pagesAccounting For Valueolst100% (5)

- EF Lecture 5 2024Document42 pagesEF Lecture 5 2024donNo ratings yet

- Steelcast Limited: Website WW. Steel Cast NetDocument5 pagesSteelcast Limited: Website WW. Steel Cast NetRahul PambharNo ratings yet

- HSBC Project Report DRAFT1Document94 pagesHSBC Project Report DRAFT1hikvNo ratings yet

- Relationship Between Inflation and Stock Prices in ThailandDocument6 pagesRelationship Between Inflation and Stock Prices in ThailandEzekiel WilliamNo ratings yet

- CFPB Mortgage Complaint DatabaseDocument718 pagesCFPB Mortgage Complaint DatabaseSP BiloxiNo ratings yet

- Chapter 9: FOREX MARKET Key PointsDocument6 pagesChapter 9: FOREX MARKET Key PointsDanica AbelardoNo ratings yet

- Here Are Some IdeasDocument3 pagesHere Are Some IdeasBrahim OuhammouNo ratings yet

- All Schemes Half Yearly Portfolio - As On 31 March 2020Document1,458 pagesAll Schemes Half Yearly Portfolio - As On 31 March 2020anjuNo ratings yet

- Commerce Guru: AccountancyDocument1 pageCommerce Guru: AccountancyHEMMU SAHU INSTITUTENo ratings yet

- Ioqm DPP-4Document1 pageIoqm DPP-4tanishk goyalNo ratings yet

- 95th JAIBB LAPBDocument4 pages95th JAIBB LAPBPial122No ratings yet

- Eco Project Chapter 5Document2 pagesEco Project Chapter 5Sanket KumarNo ratings yet

- 9Document5 pages9mukeshgangulyNo ratings yet

- ASsignmentDocument10 pagesASsignmenthu mirzaNo ratings yet

- Life Insurance and Annuity Models for Multiple LivesDocument16 pagesLife Insurance and Annuity Models for Multiple LivesFion TayNo ratings yet

- Term-4 Mid Term Question PapersDocument64 pagesTerm-4 Mid Term Question PapersParas KhuranaNo ratings yet

- Solutions To Problem Set 7Document4 pagesSolutions To Problem Set 7Manuel BoahenNo ratings yet

- Retail Financial Services Products 2022 FL 509 Report enDocument78 pagesRetail Financial Services Products 2022 FL 509 Report enStathis MetsovitisNo ratings yet

- Unit 3: The Cost of CapitalDocument10 pagesUnit 3: The Cost of CapitalhabtamuNo ratings yet