You might also like

- Cash Accounting, Accrual Accounting, and Discounted Cash Flow ValuationDocument32 pagesCash Accounting, Accrual Accounting, and Discounted Cash Flow ValuationHanh Mai TranNo ratings yet

- Valuation of FirmDocument13 pagesValuation of FirmLalitNo ratings yet

- Chapter 02 Investment AppraisalDocument3 pagesChapter 02 Investment AppraisalMarzuka Akter KhanNo ratings yet

- Stock Pitch GuideDocument25 pagesStock Pitch GuideXie NiyunNo ratings yet

- What Are Valuation MultiplesDocument20 pagesWhat Are Valuation MultiplesDhruv GNo ratings yet

- Equity Research and Valuation B Kemp Dolliver-0935015213Document69 pagesEquity Research and Valuation B Kemp Dolliver-0935015213rockkey76No ratings yet

- Sample Deal Discussions: Sell-Side Divestiture Discussion & AnalysisDocument11 pagesSample Deal Discussions: Sell-Side Divestiture Discussion & AnalysisAnonymous 45z6m4eE7pNo ratings yet

- Valuation Methods GuideDocument82 pagesValuation Methods GuideSourabh Dhawan100% (1)

- Formulas #1: Future Value of A Single Cash FlowDocument4 pagesFormulas #1: Future Value of A Single Cash FlowVikram Sathish AsokanNo ratings yet

- Cash ManagementDocument30 pagesCash ManagementankitaNo ratings yet

- Capital StructureDocument59 pagesCapital StructureRajendra MeenaNo ratings yet

- Equity Valuation ModelsDocument58 pagesEquity Valuation ModelsSarang GuptaNo ratings yet

- ValComp Tutorial 2014 (Unlocked)Document36 pagesValComp Tutorial 2014 (Unlocked)Harsh ChandaliyaNo ratings yet

- Financial Ratios of Keppel Corp 2008-1Document3 pagesFinancial Ratios of Keppel Corp 2008-1Kon Yikun KellyNo ratings yet

- Framework For Business AnalysisDocument10 pagesFramework For Business AnalysismkhanmajlisNo ratings yet

- The Partnering ToolbookDocument45 pagesThe Partnering ToolbooklenaNo ratings yet

- Mergers: Principles of Corporate FinanceDocument35 pagesMergers: Principles of Corporate FinancechooisinNo ratings yet

- Financial Modeling in ExcelDocument32 pagesFinancial Modeling in ExcelMd AtifNo ratings yet

- Reliance Petroleum's Triple Option Convertible Bonds IssueDocument2 pagesReliance Petroleum's Triple Option Convertible Bonds IssueNavin KumarNo ratings yet

- Chapter 10: Equity Valuation & AnalysisDocument22 pagesChapter 10: Equity Valuation & AnalysisMumbo JumboNo ratings yet

- Valuation of BusinessDocument44 pagesValuation of Businessnaren75No ratings yet

- An Intro to Valuation MethodsDocument15 pagesAn Intro to Valuation Methodsdeeps0705No ratings yet

- Cheat Sheet For Valuation (2) - 1Document2 pagesCheat Sheet For Valuation (2) - 1RISHAV BAIDNo ratings yet

- Corporate Finance Case StudyDocument26 pagesCorporate Finance Case StudyJimy ArangoNo ratings yet

- The Business Cycle Approach To Investing - Fidelity InvestmentsDocument8 pagesThe Business Cycle Approach To Investing - Fidelity InvestmentsKitti WongtuntakornNo ratings yet

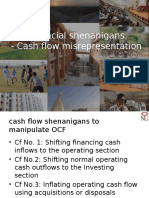

- Red Flags - ShenanigansDocument6 pagesRed Flags - Shenanigansclmu00011No ratings yet

- Cash Flow Analysis, Target Cost, Variable CostDocument29 pagesCash Flow Analysis, Target Cost, Variable CostitsmenatoyNo ratings yet

- CA FINAL SFM DERIVATIVES Futures SUMMARYDocument9 pagesCA FINAL SFM DERIVATIVES Futures SUMMARYsujeet mauryaNo ratings yet

- Exercises on FRA’s and SWAPS valuationDocument5 pagesExercises on FRA’s and SWAPS valuationrandomcuriNo ratings yet

- Formulae Sheets: Ps It Orp S It 1 1Document3 pagesFormulae Sheets: Ps It Orp S It 1 1Mengdi ZhangNo ratings yet

- Fcffsimpleginzu ITCDocument62 pagesFcffsimpleginzu ITCPravin AwalkondeNo ratings yet

- A Note On Valuation in Entrepreneurial SettingsDocument4 pagesA Note On Valuation in Entrepreneurial SettingsUsmanNo ratings yet

- Measuring Value for M&ADocument18 pagesMeasuring Value for M&Arishit_93No ratings yet

- Ch5 - Financial Statement AnalysisDocument39 pagesCh5 - Financial Statement AnalysisLaura TurbatuNo ratings yet

- Financial Shenanigans CashflowsDocument19 pagesFinancial Shenanigans CashflowsAdarsh ChhajedNo ratings yet

- CFA Industry Analysis PharmaceuticalDocument58 pagesCFA Industry Analysis Pharmaceuticalgioro_miNo ratings yet

- Exam 1 Study Guide S15Document1 pageExam 1 Study Guide S15Jack JacintoNo ratings yet

- Think Equity Think QGLP Contest 2019: Application FormDocument20 pagesThink Equity Think QGLP Contest 2019: Application Formvishakha100% (1)

- 300 - PEI - Jun 2019 - DigiDocument24 pages300 - PEI - Jun 2019 - Digimick ryanNo ratings yet

- Ubs Investor Guide 5.27Document44 pagesUbs Investor Guide 5.27shayanjalali44No ratings yet

- How To Analyze Bank Stocks - PDFDocument22 pagesHow To Analyze Bank Stocks - PDFRamasamyShenbagarajNo ratings yet

- Ê, in Finance, Is AnDocument11 pagesÊ, in Finance, Is AnJome MathewNo ratings yet

- Security Analysis: Chapter - 1Document47 pagesSecurity Analysis: Chapter - 1Harsh GuptaNo ratings yet

- Weeks 1 To 4 Fundamental AnalysisDocument166 pagesWeeks 1 To 4 Fundamental Analysismuller1234No ratings yet

- Rajagopal Deloitte Business ValuationDocument85 pagesRajagopal Deloitte Business Valuationanalyst_anil14No ratings yet

- Financial Statement Analysis RatiosDocument3 pagesFinancial Statement Analysis RatiosshahbazsiddikieNo ratings yet

- Dabur Healthcare valuation reportDocument58 pagesDabur Healthcare valuation reportUmangNo ratings yet

- Cost of CapitalDocument55 pagesCost of CapitalSaritasaruNo ratings yet

- KKR - Consolidated Research ReportsDocument60 pagesKKR - Consolidated Research Reportscs.ankur7010No ratings yet

- Valuation Practices Survey 2013 v3Document36 pagesValuation Practices Survey 2013 v3Deagle_zeroNo ratings yet

- Restructuring Debt and EquityDocument20 pagesRestructuring Debt and EquityErick SumarlinNo ratings yet

- P/B Ratio Explained for Valuing StocksDocument18 pagesP/B Ratio Explained for Valuing StocksVicknesan AyapanNo ratings yet

- Corporate RestructuringDocument18 pagesCorporate Restructuring160286sanjeevjha50% (6)

- Financial Markets: Dr. P.R .KulkarniDocument66 pagesFinancial Markets: Dr. P.R .KulkarnihrshtkatwalaNo ratings yet

- How To Choose Between Growth and ROICDocument5 pagesHow To Choose Between Growth and ROICFDRbardNo ratings yet

- WACC Capital StructureDocument68 pagesWACC Capital StructuremileticmarkoNo ratings yet

- Exam Prep for:: Business Analysis and Valuation Using Financial Statements, Text and CasesFrom EverandExam Prep for:: Business Analysis and Valuation Using Financial Statements, Text and CasesNo ratings yet

- Operations Due Diligence: An M&A Guide for Investors and BusinessFrom EverandOperations Due Diligence: An M&A Guide for Investors and BusinessNo ratings yet

- Report of BecgDocument15 pagesReport of BecgPiyush SharmaNo ratings yet

- Ethics and Delivering Customer Value Across Global MarketsDocument30 pagesEthics and Delivering Customer Value Across Global MarketsPiyush SharmaNo ratings yet

- MarketingDocument12 pagesMarketingNikunj KamalNo ratings yet

- Nimisha Singh (PGFB1328) Paridhi Bathwal (PGFB1329) Piyush Sharma (PGFB1330) Pooja Saraf (PGFB1331) Pratyush Sahu (PGFB1332)Document36 pagesNimisha Singh (PGFB1328) Paridhi Bathwal (PGFB1329) Piyush Sharma (PGFB1330) Pooja Saraf (PGFB1331) Pratyush Sahu (PGFB1332)Piyush SharmaNo ratings yet

- Business Communication2Document9 pagesBusiness Communication2Piyush SharmaNo ratings yet

- Managing Brand EquityDocument22 pagesManaging Brand EquityPiyush SharmaNo ratings yet

- Introduction To Strategic Brand ManagementDocument28 pagesIntroduction To Strategic Brand ManagementPiyush SharmaNo ratings yet

- 10 Nadiri TumerDocument13 pages10 Nadiri TumerPiyush SharmaNo ratings yet

- 6.Post-Merger and Acquisition Short-Run Financial Performance - Yayati 11Document12 pages6.Post-Merger and Acquisition Short-Run Financial Performance - Yayati 11Piyush SharmaNo ratings yet

- Credit RiskDocument3 pagesCredit RiskPiyush SharmaNo ratings yet

- SRRFFDocument32 pagesSRRFFPiyush SharmaNo ratings yet

- Internal Factor Evaluation MatrixDocument1 pageInternal Factor Evaluation MatrixPiyush SharmaNo ratings yet

- Analysis of Adoption Pattern of An Innovation ofDocument10 pagesAnalysis of Adoption Pattern of An Innovation ofPiyush SharmaNo ratings yet

- Ing Vysya Bank ProjectDocument89 pagesIng Vysya Bank Projectniteshniki100% (3)

- Final ReportDocument45 pagesFinal ReportPiyush SharmaNo ratings yet

- Get All Pair of City Values Such That Supplier 89 in The First City Supplies Project89 in The Second CityDocument7 pagesGet All Pair of City Values Such That Supplier 89 in The First City Supplies Project89 in The Second CityPiyush SharmaNo ratings yet

- Ing Vysya Bank ProjectDocument89 pagesIng Vysya Bank Projectniteshniki100% (3)

- Final ReportDocument45 pagesFinal ReportPiyush SharmaNo ratings yet

- Introduction to Production and Operations Management in 40 CharactersDocument3 pagesIntroduction to Production and Operations Management in 40 CharactersPiyush SharmaNo ratings yet

- Steve Jobs Group 4Document3 pagesSteve Jobs Group 4Piyush SharmaNo ratings yet

- CASE STUDY - Staffing A Call CenterDocument2 pagesCASE STUDY - Staffing A Call CenterPiyush Sharma50% (2)

- Portfolio ProblemDocument4 pagesPortfolio ProblemPiyush SharmaNo ratings yet

- of KhyatiDocument7 pagesof KhyatiPiyush SharmaNo ratings yet

- Definition of Business PolicyDocument3 pagesDefinition of Business PolicyPiyush Sharma100% (3)

- StrengthsDocument4 pagesStrengthsPiyush SharmaNo ratings yet

- Icci BankDocument23 pagesIcci BankPhateh Krishna AgrawalNo ratings yet

- EJMCM Volume 7 Issue 4 Pages 999-1009Document11 pagesEJMCM Volume 7 Issue 4 Pages 999-1009Reem Alaa AldinNo ratings yet

- Operating System of ICB Unit FundDocument58 pagesOperating System of ICB Unit FundShahriar Zaman HridoyNo ratings yet

- Structure and Mechanism of Corporate Governance in The Indian Banking SectorDocument7 pagesStructure and Mechanism of Corporate Governance in The Indian Banking SectorIJAR JOURNALNo ratings yet

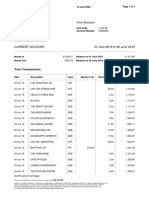

- Attachments 71b8d55c 2019 June Statement PDFDocument5 pagesAttachments 71b8d55c 2019 June Statement PDFMarianaNo ratings yet

- Assignment June 2022Document3 pagesAssignment June 2022AirForce ManNo ratings yet

- Internship Report: Janata Bank Limited and Its General Banking ActivitiesDocument54 pagesInternship Report: Janata Bank Limited and Its General Banking ActivitiesMehedi HasanNo ratings yet

- Non-Current Liabilities Cheat SheetDocument1 pageNon-Current Liabilities Cheat SheetSarah SafiraNo ratings yet

- Retail Banking Industry Growth Potential Despite ChallengesDocument26 pagesRetail Banking Industry Growth Potential Despite Challengesshukhi89No ratings yet

- Financial - Regulations Part-2 PDFDocument426 pagesFinancial - Regulations Part-2 PDFafe782480% (30)

- FixedDepositsDocument1 pageFixedDepositsTiso Blackstar GroupNo ratings yet

- Wildcat Capital InvestorsDocument18 pagesWildcat Capital Investorsokta hutahaeanNo ratings yet

- New profit sharing ratiosDocument9 pagesNew profit sharing ratiosAman KakkarNo ratings yet

- Barclays Shiller White PaperDocument36 pagesBarclays Shiller White PaperRyan LeggioNo ratings yet

- Financial Management 1 Risk and Return AnalysisDocument12 pagesFinancial Management 1 Risk and Return AnalysisANKITA M SHARMANo ratings yet

- Accounts.31.12.17.FinalDocument7 pagesAccounts.31.12.17.FinalMileticoNo ratings yet

- CA - FOUNDATION LT (APRIL BATCH) NOV'23WE-4 QP-keyDocument4 pagesCA - FOUNDATION LT (APRIL BATCH) NOV'23WE-4 QP-keyDhruv AgarwalNo ratings yet

- Deloitte Au Tax Insight Deconstructing Chevron Transfer Pricing Case 041115 PDFDocument8 pagesDeloitte Au Tax Insight Deconstructing Chevron Transfer Pricing Case 041115 PDFCA.Srikant Parthasarathy ParthasarathyNo ratings yet

- Audit Property Plant EquipmentDocument5 pagesAudit Property Plant EquipmentMonica GarciaNo ratings yet

- Form OC-10 Appl 4 FRNDocument51 pagesForm OC-10 Appl 4 FRNBenne James100% (4)

- Accountancy & Auditing Paper - 1-2015Document3 pagesAccountancy & Auditing Paper - 1-2015Qasim IbrarNo ratings yet

- Basis Trading BasicsDocument51 pagesBasis Trading BasicsTajinder SinghNo ratings yet

- STDSMT Funds MT MX MapDocument120 pagesSTDSMT Funds MT MX MapDnyaneshwar PatilNo ratings yet

- This Spreadsheet Supports Analysis of The Case, "Coleco Industries Inc." (Case 60)Document6 pagesThis Spreadsheet Supports Analysis of The Case, "Coleco Industries Inc." (Case 60)kashanr82No ratings yet

- Account Opening DisclosuresDocument7 pagesAccount Opening DisclosuresMarcus Wilson100% (1)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument12 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balanceamool rokadeNo ratings yet

- WM Unit 8 Retirement Planning 6th Jan 2022Document32 pagesWM Unit 8 Retirement Planning 6th Jan 2022Aarti GuptaNo ratings yet

- Corporate Financial Management IntroDocument17 pagesCorporate Financial Management IntroADEYANJU AKEEMNo ratings yet

- About IndustryDocument36 pagesAbout IndustryHardik AgarwalNo ratings yet

- PNB v. CA and Ramon LopezDocument2 pagesPNB v. CA and Ramon LopezRebecca ChanNo ratings yet