You might also like

- Winning Binary Options Trading Strategy: Simple Secret of Making Money From Binary Options TradingFrom EverandWinning Binary Options Trading Strategy: Simple Secret of Making Money From Binary Options TradingRating: 4.5 out of 5 stars4.5/5 (22)

- #1 Forex Trading CourseDocument63 pages#1 Forex Trading Courseitsrijo100% (1)

- Lesson 1.1 International Finance ManagementDocument15 pagesLesson 1.1 International Finance Managementashu1286No ratings yet

- Demo - Nism 8 - Equity Derivatives ModuleDocument7 pagesDemo - Nism 8 - Equity Derivatives ModuleBhupat1270% (1)

- Upload Portfolio Positions to BloombergDocument30 pagesUpload Portfolio Positions to BloombergAlex LimNo ratings yet

- Meet The Real 'Wolf of Wall Street' in Forbes' Original Takedown of Jordan BelfortDocument4 pagesMeet The Real 'Wolf of Wall Street' in Forbes' Original Takedown of Jordan BelfortJay SayNo ratings yet

- CAPM AssignmentDocument1 pageCAPM Assignmentshreyansh jainNo ratings yet

- 10 Forex Quotes IB. Sess 16Document10 pages10 Forex Quotes IB. Sess 16Kapil PrabhuNo ratings yet

- 1 Foreign Exchange Markets - IDocument8 pages1 Foreign Exchange Markets - INaomi LyngdohNo ratings yet

- Forex ProblemsDocument38 pagesForex Problemsnehali Madhukar AherNo ratings yet

- An Introduction To The Foreign Exchange Market Moorad ChoudhryDocument6 pagesAn Introduction To The Foreign Exchange Market Moorad ChoudhryVipin Kumar CNo ratings yet

- Exchange Rate Calculation Types Spot ForwardDocument6 pagesExchange Rate Calculation Types Spot ForwardRohit AggarwalNo ratings yet

- BCCM International Finance Module Provides Insight into Foreign Exchange MarketsDocument83 pagesBCCM International Finance Module Provides Insight into Foreign Exchange MarketsSingmay MoralNo ratings yet

- SPT, Cross, ForwardDocument38 pagesSPT, Cross, Forwardseagul_1183822No ratings yet

- Forex For CAIIBDocument6 pagesForex For CAIIBkushalnadekarNo ratings yet

- (A& F) - IfM-Foreign Exchange MarketsDocument24 pages(A& F) - IfM-Foreign Exchange Marketsudayraju2007No ratings yet

- World Monetary System and Exchange RatesDocument16 pagesWorld Monetary System and Exchange RatesRishabh SehrawatNo ratings yet

- Balance of Payment 20Document79 pagesBalance of Payment 20Anshul SinhaNo ratings yet

- Cross Rate and Merchant RateDocument26 pagesCross Rate and Merchant RateDivya NadarajanNo ratings yet

- Foreign Exchange Markets: Prof Mahesh Kumar Amity Business SchoolDocument47 pagesForeign Exchange Markets: Prof Mahesh Kumar Amity Business SchoolasifanisNo ratings yet

- 35 Summary ForexDocument15 pages35 Summary ForexRevati GalgaliNo ratings yet

- Introduction To International Financial ManagementDocument37 pagesIntroduction To International Financial ManagementhappyNo ratings yet

- Foreign Exchange Rates CalculationsDocument14 pagesForeign Exchange Rates Calculationsnenu_1000% (1)

- Lecture 7: The Forward Exchange MarketDocument35 pagesLecture 7: The Forward Exchange MarketkarthickgamblerNo ratings yet

- Direct Quotations Can Be Converted Into Indirect Quotations and Vice VersaDocument6 pagesDirect Quotations Can Be Converted Into Indirect Quotations and Vice VersaLeo the BulldogNo ratings yet

- Afu 08504 - International Finance - The Economics of Foreign Exchange MarketDocument10 pagesAfu 08504 - International Finance - The Economics of Foreign Exchange MarketWilliam MuhomiNo ratings yet

- Chapter 15: Foreign Exchange (FX) MarketsDocument32 pagesChapter 15: Foreign Exchange (FX) MarketsjoannamanngoNo ratings yet

- CURRENCY DERIVATIVES MARKET OVERVIEWDocument39 pagesCURRENCY DERIVATIVES MARKET OVERVIEWNandita ShahNo ratings yet

- Illustrations For PracticeDocument3 pagesIllustrations For PracticeDhruvi AgarwalNo ratings yet

- Introduction To Interest Rate Trading: Andrew WilkinsonDocument44 pagesIntroduction To Interest Rate Trading: Andrew WilkinsonLee Jia QingNo ratings yet

- Accounting For Foreign Currency TransactionsDocument8 pagesAccounting For Foreign Currency TransactionsHussen AbdulkadirNo ratings yet

- Forex Trading CourseDocument69 pagesForex Trading Courseapi-3703868No ratings yet

- Study International Finance Markets and CurrenciesDocument14 pagesStudy International Finance Markets and CurrenciesNoopur SrivastavaNo ratings yet

- Evolution and Future of ForexDocument44 pagesEvolution and Future of Forexsushant1903No ratings yet

- R21 Currency Exchange Rates IFT NotesDocument35 pagesR21 Currency Exchange Rates IFT NotesMohammad Jubayer AhmedNo ratings yet

- Exchange Rate Quotations, Balance of Payments, Prices, Parities and Interest RatesDocument22 pagesExchange Rate Quotations, Balance of Payments, Prices, Parities and Interest RatesSourav PaulNo ratings yet

- Foreign Exchange Market: Dr. Amit Kumar SinhaDocument67 pagesForeign Exchange Market: Dr. Amit Kumar SinhaAmit SinhaNo ratings yet

- ABC of Foreign ExchangeDocument8 pagesABC of Foreign Exchangesulabhpathak1987No ratings yet

- Currency Future and OptionsDocument60 pagesCurrency Future and Optionspanicker_maheshNo ratings yet

- Echange Rate Mechanism: 1. Direct Quote 2. Indirect QuoteDocument4 pagesEchange Rate Mechanism: 1. Direct Quote 2. Indirect QuoteanjankumarNo ratings yet

- Foreign Exchange MarketDocument29 pagesForeign Exchange MarketRavi SistaNo ratings yet

- FX 102 - FX Rates and ArbitrageDocument32 pagesFX 102 - FX Rates and Arbitragetesting1997No ratings yet

- 08 - MM FuturesDocument9 pages08 - MM FuturesildaNo ratings yet

- Unit 2Document15 pagesUnit 2Aryan RajNo ratings yet

- International Business FinanceDocument14 pagesInternational Business FinanceKshitij ShahNo ratings yet

- INTERNATIONAL BANKING MANAGEMENTDocument39 pagesINTERNATIONAL BANKING MANAGEMENTaabha06021984No ratings yet

- INTERNATIONAL FINANCE MODULES AND EVALUATIONDocument30 pagesINTERNATIONAL FINANCE MODULES AND EVALUATIONSaurav GoyalNo ratings yet

- Lecture 10-Foreign Exchange MarketDocument42 pagesLecture 10-Foreign Exchange MarketfarahNo ratings yet

- Forex Trading Course - Turn $1,260 Into $12,300 in 30 Days by David CDocument74 pagesForex Trading Course - Turn $1,260 Into $12,300 in 30 Days by David Capi-3748231No ratings yet

- Foreign Exchange MarketDocument27 pagesForeign Exchange MarketMD SHUJAATULLAH SADIQNo ratings yet

- Assignment 1stDocument3 pagesAssignment 1stAmmar ButtNo ratings yet

- Foreign Exchange Rate MarketDocument92 pagesForeign Exchange Rate Marketamubine100% (1)

- Euro EconomyDocument26 pagesEuro EconomyJinal ShahNo ratings yet

- Foreign Exchange MarketDocument73 pagesForeign Exchange MarketAmit Sinha100% (1)

- International Financial ManagementDocument38 pagesInternational Financial Managementhaidersyed06No ratings yet

- Forex Markets: International Finance - Group 3 Roll No-11, 16, 30, 45, 47, 58Document34 pagesForex Markets: International Finance - Group 3 Roll No-11, 16, 30, 45, 47, 58Pradyumna SwainNo ratings yet

- What Is The Spot Market?Document2 pagesWhat Is The Spot Market?chinmayaNo ratings yet

- INTERNATIONAL FINANCIAL SYLLABUSDocument90 pagesINTERNATIONAL FINANCIAL SYLLABUSTarini MohantyNo ratings yet

- Unit 17 Exchange RatesDocument15 pagesUnit 17 Exchange Ratesujjwal kumar 2106No ratings yet

- Forex Trading for Beginners: The Ultimate Trading Guide. Learn Successful Strategies to Buy and Sell in the Right Moment in the Foreign Exchange Market and Master the Right Mindset.From EverandForex Trading for Beginners: The Ultimate Trading Guide. Learn Successful Strategies to Buy and Sell in the Right Moment in the Foreign Exchange Market and Master the Right Mindset.No ratings yet

- Lesson - 4.1 (1) International Finance ManagementDocument14 pagesLesson - 4.1 (1) International Finance Managementashu1286No ratings yet

- IFM SyllabusDocument4 pagesIFM Syllabusashu1286No ratings yet

- Lesson - 4.2 International Finance ManagementDocument19 pagesLesson - 4.2 International Finance Managementashu1286No ratings yet

- Lesson - 2.2 International Finance ManagementDocument10 pagesLesson - 2.2 International Finance Managementashu1286No ratings yet

- Lesson - 3.3 International Finance ManagementDocument11 pagesLesson - 3.3 International Finance Managementashu1286No ratings yet

- International Finance ManagementDocument38 pagesInternational Finance Managementashu1286No ratings yet

- Lesson - 5.2 International Finance ManagementDocument12 pagesLesson - 5.2 International Finance Managementashu1286No ratings yet

- Lesson - 5.2 International Finance ManagementDocument37 pagesLesson - 5.2 International Finance Managementashu1286No ratings yet

- Lesson - 5.1 International Finance ManagementDocument31 pagesLesson - 5.1 International Finance Managementashu1286No ratings yet

- Lesson 2.3 Revised International Finance ManagementDocument12 pagesLesson 2.3 Revised International Finance Managementashu1286No ratings yet

- Lesson 2.4 International Finance ManagementDocument18 pagesLesson 2.4 International Finance Managementashu1286No ratings yet

- Lesson 1.2 BOP International Finance ManagementDocument16 pagesLesson 1.2 BOP International Finance Managementashu1286No ratings yet

- Lesson 3.2 International Finance ManagementDocument26 pagesLesson 3.2 International Finance Managementashu1286No ratings yet

- Lesson 3.1 International Finance ManagementDocument24 pagesLesson 3.1 International Finance Managementashu1286No ratings yet

- Project Finance and Management Post-Completion Audit Abandonment AnalysisDocument8 pagesProject Finance and Management Post-Completion Audit Abandonment Analysisashu1286No ratings yet

- Iifm AssignmentDocument3 pagesIifm Assignmentashu1286No ratings yet

- Test of IfmDocument3 pagesTest of Ifmashu1286No ratings yet

- Assignment 1 International Financial MangtDocument5 pagesAssignment 1 International Financial Mangtashu1286No ratings yet

- Graham & Doddsville Issue: Fall 2019Document48 pagesGraham & Doddsville Issue: Fall 2019marketfolly.comNo ratings yet

- Chapter 5 FinanceDocument18 pagesChapter 5 FinancePia Eriksson0% (1)

- Order in The Matter of M/s Sunshine Global Agro LimitedDocument16 pagesOrder in The Matter of M/s Sunshine Global Agro LimitedShyam SunderNo ratings yet

- Balance of Payments AccountingDocument20 pagesBalance of Payments AccountingWilly AndersonNo ratings yet

- DNL Use of Proceeds Annual Progress As of 12.31.14Document6 pagesDNL Use of Proceeds Annual Progress As of 12.31.14WrLw7pcufeGUNo ratings yet

- Self Trading Prevention Functionality v100Document25 pagesSelf Trading Prevention Functionality v100Leonardo GiglioNo ratings yet

- Company Conformed Name: Morgan Stanley Central IndexDocument169 pagesCompany Conformed Name: Morgan Stanley Central IndexgggfickaNo ratings yet

- F9D2Document30 pagesF9D2mysticsoulNo ratings yet

- Day Trading StrategiesDocument4 pagesDay Trading Strategiesthushantha50% (2)

- Terms and Conditions EToroDocument42 pagesTerms and Conditions EToroZhess BugNo ratings yet

- SBI's Organizational StructureDocument1 pageSBI's Organizational StructureKautuk Popli100% (1)

- Case Study - Harshad MehtaDocument5 pagesCase Study - Harshad MehtaMudit AgarwalNo ratings yet

- Select Banking and Finance AbbreviationsDocument5 pagesSelect Banking and Finance AbbreviationsAnmol JainNo ratings yet

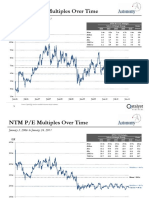

- NTM Revenue Multiples Over Time: Mean 6.8x, 75th Perc 7.6xDocument3 pagesNTM Revenue Multiples Over Time: Mean 6.8x, 75th Perc 7.6xmittleNo ratings yet

- Research Methodology on Major Stock Market ScamsDocument35 pagesResearch Methodology on Major Stock Market ScamsSameer VelaniNo ratings yet

- Law and Practice of BankingDocument151 pagesLaw and Practice of BankingAshok KumarNo ratings yet

- Session 2 International FinanceDocument3 pagesSession 2 International FinanceTumbleweedNo ratings yet

- Trade Capture Report MessagesDocument25 pagesTrade Capture Report Messagesjatipatel5719No ratings yet

- ReportDocument3 pagesReportumaganNo ratings yet

- Binus Financial Analyst Academy CFA Program Level 1 Semester 2 Batch 34 2018 V4fDocument5 pagesBinus Financial Analyst Academy CFA Program Level 1 Semester 2 Batch 34 2018 V4fBudiman SnowieNo ratings yet

- Risk and Return: Past and PrologueDocument39 pagesRisk and Return: Past and ProloguerrNo ratings yet

- Prudential Regulations For Corporate / Commercial BankingDocument73 pagesPrudential Regulations For Corporate / Commercial BankingAsma ShoaibNo ratings yet

- Investment:: Process of Estimating Return and Risk of A Security Is Known As Security AnalysisDocument76 pagesInvestment:: Process of Estimating Return and Risk of A Security Is Known As Security AnalysisDowlathAhmedNo ratings yet

- Premier Cement 16Document177 pagesPremier Cement 16Leanna R. Braxton100% (1)

- 99th AGM AR WEB 16 07 2018 PDFDocument184 pages99th AGM AR WEB 16 07 2018 PDFpks009No ratings yet

- AEA: Simultaneous Determination of Spot and Futures PricesDocument15 pagesAEA: Simultaneous Determination of Spot and Futures PricesGeorge máximoNo ratings yet