You might also like

- As Sess Ment Pro Ced Ure: SEC - 139 o Nwar DsDocument179 pagesAs Sess Ment Pro Ced Ure: SEC - 139 o Nwar Dsmsnethrapal100% (2)

- Javier Milei's Dnu: Basis for the Reconstruction of the Argentine EconomyFrom EverandJavier Milei's Dnu: Basis for the Reconstruction of the Argentine EconomyNo ratings yet

- Assess Pro 1Document128 pagesAssess Pro 1msnethrapal100% (2)

- As Sess Ment Pro Ced Ure: SEC - 139 o Nwar DsDocument113 pagesAs Sess Ment Pro Ced Ure: SEC - 139 o Nwar Dsmsnethrapal100% (2)

- Assess Pro 1Document140 pagesAssess Pro 1msnethrapal100% (2)

- As Sess Ment Pro Ced Ure: SEC - 139 o Nwar DsDocument74 pagesAs Sess Ment Pro Ced Ure: SEC - 139 o Nwar Dsmsnethrapal100% (2)

- Assess Pro 1Document168 pagesAssess Pro 1msnethrapal100% (2)

- Assess Pro 1Document125 pagesAssess Pro 1msnethrapal100% (2)

- Assess Pro 1Document101 pagesAssess Pro 1msnethrapal100% (2)

- Assess Pro 1Document82 pagesAssess Pro 1msnethrapal100% (2)

- Assess Pro FinalDocument194 pagesAssess Pro Finalmsnethrapal100% (2)

- Income Tax Summary TulibasDocument66 pagesIncome Tax Summary TulibasVan DahuyagNo ratings yet

- EH403 TAXATION IIPREFINALS TAX ENFORCEMENT ADMIN EditedDocument7 pagesEH403 TAXATION IIPREFINALS TAX ENFORCEMENT ADMIN Editedethel hyugaNo ratings yet

- Taxation Law Review Notes SummaryDocument58 pagesTaxation Law Review Notes SummarySara Dela Cruz Avillon0% (1)

- Fundamentals of TaxationDocument13 pagesFundamentals of TaxationKatrina MaglaquiNo ratings yet

- Supplemental Note #1 - General Principles of Taxation, Intro To Income TaxationDocument9 pagesSupplemental Note #1 - General Principles of Taxation, Intro To Income TaxationRicojay FernandezNo ratings yet

- 2021 SBU Red Book Volume 1 - Taxation LawDocument121 pages2021 SBU Red Book Volume 1 - Taxation LawJong CjaNo ratings yet

- Chapter 1 - Basic Concepts of Income Tax - AY - 20-21 PDFDocument16 pagesChapter 1 - Basic Concepts of Income Tax - AY - 20-21 PDFAbhishek VermaNo ratings yet

- Lesson 1Document17 pagesLesson 1Rachel Mae BardeNo ratings yet

- SunChi Notes on Taxation PrinciplesDocument23 pagesSunChi Notes on Taxation PrinciplesdoraemoanNo ratings yet

- Income Taxation ReviewerDocument17 pagesIncome Taxation ReviewerheheNo ratings yet

- Taxation Notes (Tabag)Document10 pagesTaxation Notes (Tabag)Mary Angeline SalvaneraNo ratings yet

- 10yrs GSTDocument70 pages10yrs GSTmehakahuja2003No ratings yet

- Introduction To Taxtion: Taxation May Be Defined As ADocument7 pagesIntroduction To Taxtion: Taxation May Be Defined As ACharmae BrutasNo ratings yet

- Basic Principles TaxationDocument13 pagesBasic Principles TaxationgRascia Ona0% (1)

- Taxes, Tax Laws, and Tax AdministrationDocument8 pagesTaxes, Tax Laws, and Tax AdministrationAilene MendozaNo ratings yet

- Domondon Tax ReviewerDocument47 pagesDomondon Tax ReviewerHezl Valerie Arzadon100% (1)

- Income Tax Basic ComponentDocument72 pagesIncome Tax Basic ComponentRohit SinghNo ratings yet

- Ace Tax Law NotesDocument145 pagesAce Tax Law Notesalexes24No ratings yet

- General Principles of TaxationDocument5 pagesGeneral Principles of TaxationDenise MedranoNo ratings yet

- Inbound 3957617422269830470Document59 pagesInbound 3957617422269830470Ashley BrozasNo ratings yet

- Tax 1 Notes PDFDocument17 pagesTax 1 Notes PDFRose Ann BatucanNo ratings yet

- Introduction to Canadian Income Tax LawDocument113 pagesIntroduction to Canadian Income Tax LawJoel McleishNo ratings yet

- Chapter 2: Taxes, Tax Laws, and Tax AdministrationDocument9 pagesChapter 2: Taxes, Tax Laws, and Tax Administrationemielyn lafortezaNo ratings yet

- Week 2 DiscussionsDocument6 pagesWeek 2 DiscussionsUnknowingly AnonymousNo ratings yet

- Domondon Taxation Notes 2010Document81 pagesDomondon Taxation Notes 2010ryanmigNo ratings yet

- Taxation Law Review Prelims Finals PeriodDocument118 pagesTaxation Law Review Prelims Finals Periodmarcus.pebenitojrNo ratings yet

- Association of The Philippines, Et Al., G. R. No. 158540, August 3, 2005)Document27 pagesAssociation of The Philippines, Et Al., G. R. No. 158540, August 3, 2005)GeanelleRicanorEsperonNo ratings yet

- Tax 1 Reviewer Atty. Bolivar NotesDocument121 pagesTax 1 Reviewer Atty. Bolivar NotesRauden Bacerdo Panotes100% (1)

- Presentation in General Principles National Taxation by Prof. Marvin CañeroDocument77 pagesPresentation in General Principles National Taxation by Prof. Marvin CañeroRoita Amon Jordan VallesNo ratings yet

- General Principles of TaxationDocument88 pagesGeneral Principles of TaxationKristine LumanogNo ratings yet

- 2010 Taxation Review by Domondon 1Document13 pages2010 Taxation Review by Domondon 1Aldus31100% (1)

- 01 - General Principles of Taxation (Revised 2023)Document6 pages01 - General Principles of Taxation (Revised 2023)Princess DantesNo ratings yet

- Domondon Based Tax ReviewerDocument77 pagesDomondon Based Tax ReviewerGenevieve Penetrante100% (1)

- Lesson 1,2 and 3 BASIC PRINCIPLES OF TAXATIONDocument11 pagesLesson 1,2 and 3 BASIC PRINCIPLES OF TAXATIONLouie Ann CasabarNo ratings yet

- Taxation Bar ReviewerDocument14 pagesTaxation Bar ReviewerevangarethNo ratings yet

- Taxation - Introductory ChapterDocument34 pagesTaxation - Introductory ChapterDan SuminguitNo ratings yet

- Taxation Notes (Tabag)Document10 pagesTaxation Notes (Tabag)Mary Angeline SalvaneraNo ratings yet

- NEU Taxation Law Pre-Week NotesDocument35 pagesNEU Taxation Law Pre-Week NotesKin Pearly FloresNo ratings yet

- NEU Taxation Law Pre-Week Notes PDFDocument35 pagesNEU Taxation Law Pre-Week Notes PDFKin Pearly FloresNo ratings yet

- Income Tax May23 Free ResourcesDocument321 pagesIncome Tax May23 Free ResourcesPurna PatelNo ratings yet

- CM Taxation 2Document56 pagesCM Taxation 2ErmawooNo ratings yet

- Taxation 1 PDFDocument2 pagesTaxation 1 PDFCoolen OlindoNo ratings yet

- Basics of Taxation and Constitutional ProvisionsDocument22 pagesBasics of Taxation and Constitutional ProvisionsSrivathsan NambiraghavanNo ratings yet

- What Is TaxationDocument3 pagesWhat Is TaxationElmira Joyce PaugNo ratings yet

- TAXATIONDocument23 pagesTAXATIONJessica AragonNo ratings yet

- Income TaxationDocument10 pagesIncome TaxationCamille Anne GalvezNo ratings yet

- Remedies in Taxation Reviewer (Japatax)Document14 pagesRemedies in Taxation Reviewer (Japatax)Janine AranasNo ratings yet

- General Principles and Concepts of TaxationDocument19 pagesGeneral Principles and Concepts of TaxationShook GaNo ratings yet

- Sanskrit - IDocument18 pagesSanskrit - ImsnethrapalNo ratings yet

- Easy and Fun Cursive WritingDocument112 pagesEasy and Fun Cursive WritingL.A.N.Y87% (23)

- Cursive Practice A ZDocument26 pagesCursive Practice A Zavabhyankar9393No ratings yet

- Cursive Practice A ZDocument26 pagesCursive Practice A Zavabhyankar9393No ratings yet

- Design Toolkit (Converted)Document1 pageDesign Toolkit (Converted)msnethrapalNo ratings yet

- MaratiDocument16 pagesMaratimsnethrapalNo ratings yet

- Sanskrit - IIIDocument12 pagesSanskrit - IIImsnethrapalNo ratings yet

- Office of The Director of Public Instruction (Research & Training) - (Dsert)Document13 pagesOffice of The Director of Public Instruction (Research & Training) - (Dsert)msnethrapalNo ratings yet

- Office of The Director of Public Instruction (Research & Training) - (Dsert)Document16 pagesOffice of The Director of Public Instruction (Research & Training) - (Dsert)msnethrapalNo ratings yet

- Fractions VII Subtracting Like Denominators: Iota MathDocument21 pagesFractions VII Subtracting Like Denominators: Iota MathmsnethrapalNo ratings yet

- Ék#Tk Aùkvll Tkykotkk Aùdkk - RBK K (L Kakzk - PPPMZK Xkkakk LCTRM XKKCKDocument14 pagesÉk#Tk Aùkvll Tkykotkk Aùdkk - RBK K (L Kakzk - PPPMZK Xkkakk LCTRM XKKCKmsnethrapalNo ratings yet

- (H XR Àw - MFM: D.S.E.R.TDocument11 pages(H XR Àw - MFM: D.S.E.R.TmsnethrapalNo ratings yet

- Fractions XIV Multiplication of Fractions With Mixed NumbersDocument15 pagesFractions XIV Multiplication of Fractions With Mixed NumbersmsnethrapalNo ratings yet

- Fractions XIII Multiplication of FractionsDocument17 pagesFractions XIII Multiplication of FractionsmsnethrapalNo ratings yet

- Fractions XiDocument28 pagesFractions XimsnethrapalNo ratings yet

- Fractions XiiDocument15 pagesFractions XiimsnethrapalNo ratings yet

- Fractions VIIIDocument34 pagesFractions VIIImsnethrapalNo ratings yet

- MD Facts 1to9 010Document2 pagesMD Facts 1to9 010msnethrapalNo ratings yet

- Fractions VIDocument20 pagesFractions VImsnethrapalNo ratings yet

- Fractions IIIDocument16 pagesFractions IIImsnethrapalNo ratings yet

- Fractions IVDocument26 pagesFractions IVmsnethrapalNo ratings yet

- Fractions VDocument40 pagesFractions VmsnethrapalNo ratings yet

- Fraction X Adding Unlike Denominators: Iota MathDocument31 pagesFraction X Adding Unlike Denominators: Iota MathmsnethrapalNo ratings yet

- Iota Math Fractions - 2Document16 pagesIota Math Fractions - 2msnethrapalNo ratings yet

- Fraction IxDocument42 pagesFraction IxmsnethrapalNo ratings yet

- MD Facts 1to9 009Document2 pagesMD Facts 1to9 009msnethrapalNo ratings yet

- Fractions IDocument21 pagesFractions ImsnethrapalNo ratings yet

- MD Facts 1to9 008Document2 pagesMD Facts 1to9 008msnethrapalNo ratings yet

- MD Facts 1to9 005Document2 pagesMD Facts 1to9 005msnethrapalNo ratings yet

- MD Facts 1to9 007Document2 pagesMD Facts 1to9 007msnethrapalNo ratings yet

- Value Line Research Report GuideDocument23 pagesValue Line Research Report GuideCarl HsiehNo ratings yet

- Central Bank of The Philippines v. CA (G.r. No. 88353) DigestDocument2 pagesCentral Bank of The Philippines v. CA (G.r. No. 88353) DigestApril100% (1)

- Genmath11 q2 Mod4 Stocks-And-BondsDocument16 pagesGenmath11 q2 Mod4 Stocks-And-BondsLicht KnavesmireNo ratings yet

- Private Commercial BanksDocument7 pagesPrivate Commercial Banksjakia sultanaNo ratings yet

- Daftar Akun Nomor Nama Akun Fungsi Untuk Mencatat Mutasi NilaiDocument4 pagesDaftar Akun Nomor Nama Akun Fungsi Untuk Mencatat Mutasi NilaiFhina LarioNo ratings yet

- Copy of Summer Internship Project ReportDocument28 pagesCopy of Summer Internship Project ReportSandeep SharmaNo ratings yet

- Madhucon Projects: Performance HighlightsDocument12 pagesMadhucon Projects: Performance HighlightsAngel BrokingNo ratings yet

- Gross KlussmannDocument131 pagesGross KlussmannMotiram paudelNo ratings yet

- ForexCOMBOSystem Guide v5.0 (4in1) NFDocument14 pagesForexCOMBOSystem Guide v5.0 (4in1) NFMiguel Angel PerezNo ratings yet

- Stock Broking Firms 2003Document41 pagesStock Broking Firms 2003sudipkudasNo ratings yet

- FRIA NotesDocument6 pagesFRIA Notesaquanesse21100% (1)

- Working CapitalDocument61 pagesWorking CapitalSharmistha Banerjee100% (1)

- Mutual FundDocument68 pagesMutual Fundgyanprakashdeb302100% (1)

- Money Monster (Reaction Paper)Document1 pageMoney Monster (Reaction Paper)Kersteen JoyNo ratings yet

- Erajaya Swasembada TBK.: Company Report: January 2018 As of 31 January 2018Document3 pagesErajaya Swasembada TBK.: Company Report: January 2018 As of 31 January 2018Ahmad SyukriNo ratings yet

- MAF653 TEST 1 NOV 2022 QuestionDocument11 pagesMAF653 TEST 1 NOV 2022 QuestionAyunieazahaNo ratings yet

- Benefits of Adverse PossessionDocument3 pagesBenefits of Adverse PossessionBob Hurt100% (3)

- NC Concept MapDocument3 pagesNC Concept MapMitch MindanaoNo ratings yet

- SRC Supplement 1-Registered Debt CompaniesDocument2 pagesSRC Supplement 1-Registered Debt CompaniesMae Richelle Dizon DacaraNo ratings yet

- Chorus Investor Presentation February 14 2020Document46 pagesChorus Investor Presentation February 14 2020Raja El jaafariNo ratings yet

- The Objective in Corporate Finance: Maximizing Stockholder WealthDocument51 pagesThe Objective in Corporate Finance: Maximizing Stockholder WealthFrank MatthewsNo ratings yet

- Usefulness of AccountingDocument17 pagesUsefulness of AccountingMochamadMaarifNo ratings yet

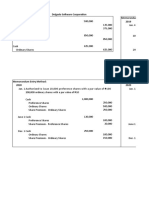

- Memorandum and Journal Entry Methods for Share Capital TransactionsDocument3 pagesMemorandum and Journal Entry Methods for Share Capital TransactionsFeiya Liu100% (1)

- Dissertation For II Year M .Com StudentsDocument12 pagesDissertation For II Year M .Com Studentsnischal mathewNo ratings yet

- Formation of Joint Stock CompanyDocument5 pagesFormation of Joint Stock CompanyHemchandra PatilNo ratings yet

- CSLDocument4 pagesCSLEnriqueNo ratings yet

- Promise & Potential of US Savings BondsDocument55 pagesPromise & Potential of US Savings BondsSarika AbbiNo ratings yet

- UntitledDocument43 pagesUntitledShirley YipNo ratings yet

- Secure Electronic TransactionDocument22 pagesSecure Electronic TransactionRiddhi DesaiNo ratings yet