You might also like

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- Tutorial For UT Exam PDFDocument62 pagesTutorial For UT Exam PDFHanafi MansorNo ratings yet

- Shares and Taxation: A Practical Guide to Saving Tax on Your SharesFrom EverandShares and Taxation: A Practical Guide to Saving Tax on Your SharesNo ratings yet

- Selling Your BusinessDocument27 pagesSelling Your BusinessCatherine GannonNo ratings yet

- Investment in Equity SecuritiesDocument23 pagesInvestment in Equity SecuritiesJay-L TanNo ratings yet

- Balance Sheet & Income StatementDocument12 pagesBalance Sheet & Income StatementPahile Bajirao PeshaveNo ratings yet

- JAIIB CAPITAL MARKET GUIDEDocument48 pagesJAIIB CAPITAL MARKET GUIDEKumar JayantNo ratings yet

- Financial Accounting and Reporting Study Guide NotesFrom EverandFinancial Accounting and Reporting Study Guide NotesRating: 1 out of 5 stars1/5 (1)

- Aditya 1138Document31 pagesAditya 1138Nirbhay SinghNo ratings yet

- Unit 4Document85 pagesUnit 4Ankush Singh100% (1)

- The Role of StockbrokersDocument32 pagesThe Role of StockbrokersSaif AliNo ratings yet

- Cash FlowDocument25 pagesCash Flowamits3989No ratings yet

- AccountsDocument12 pagesAccountsKhadeeja ShoukathNo ratings yet

- Capital Gains Tax Rules for Asset ClassificationDocument44 pagesCapital Gains Tax Rules for Asset ClassificationPrince Anton DomondonNo ratings yet

- Investor RightsDocument1 pageInvestor RightsUlycys GrantNo ratings yet

- CORPORATE ACCOUNTING FUNDAMENTALSDocument42 pagesCORPORATE ACCOUNTING FUNDAMENTALSedsie manguladNo ratings yet

- Balance Sheet: by Dr. ArchanaDocument19 pagesBalance Sheet: by Dr. ArchanaHan JeeNo ratings yet

- Capital Gains TaxDocument16 pagesCapital Gains TaxHazel ChatsNo ratings yet

- 10 AS13 Invesment AccountingDocument8 pages10 AS13 Invesment Accountingprashantmis452No ratings yet

- BASIC ACCOUNTING - Balance SheetDocument31 pagesBASIC ACCOUNTING - Balance Sheetjulito losbanosNo ratings yet

- Stock Exchange: by Huda A.S. QureshiDocument27 pagesStock Exchange: by Huda A.S. Qureshistd_10225No ratings yet

- Analyze Financial Statements to Calculate Key Metrics Like ROIC, FCFDocument12 pagesAnalyze Financial Statements to Calculate Key Metrics Like ROIC, FCFhitman2986No ratings yet

- Delivery Trading in Stock MarketDocument4 pagesDelivery Trading in Stock MarketkingmanNo ratings yet

- Share Market - 2012Document27 pagesShare Market - 2012sthesibisiNo ratings yet

- Accounting TerminologyDocument17 pagesAccounting TerminologyMurali Krishna GbNo ratings yet

- Amity Business School: Cost & Management Accounting For Decision Making-ACCT611Document76 pagesAmity Business School: Cost & Management Accounting For Decision Making-ACCT611Manjula ShastriNo ratings yet

- Cash Flow and Fund Flow AnalysisDocument54 pagesCash Flow and Fund Flow AnalysisBondye LimyèNo ratings yet

- DP1 FM FaDocument32 pagesDP1 FM FaananditaNo ratings yet

- Module D - Final Accounts of Banks & Companies - PresentationDocument102 pagesModule D - Final Accounts of Banks & Companies - PresentationASHISH GUPTANo ratings yet

- Buying & Selling RatesDocument29 pagesBuying & Selling RatesSunil SinghNo ratings yet

- For Quiz 4Document29 pagesFor Quiz 4ncq6dmzmp4No ratings yet

- Chapter 12 Dealings in PropertyDocument7 pagesChapter 12 Dealings in PropertyCharmie JaviertoNo ratings yet

- Employment and Self Employment..Document17 pagesEmployment and Self Employment..eraraja390No ratings yet

- Financial Asset at Fair ValueDocument32 pagesFinancial Asset at Fair ValueJay-L TanNo ratings yet

- CAIIB - Financial Management - ModuleDocument26 pagesCAIIB - Financial Management - ModuleSantosh100% (3)

- SEBIDocument22 pagesSEBIGautam Jayasurya0% (1)

- Cash Flow StatementDocument20 pagesCash Flow StatementDr. Shoaib MohammedNo ratings yet

- Dealing of PropertiesDocument15 pagesDealing of Propertiessha maranan100% (2)

- Financial Management I: Session 3, 4 & 5Document26 pagesFinancial Management I: Session 3, 4 & 5Harshit MaheshwariNo ratings yet

- VAT Presentation: Key Concepts ExplainedDocument30 pagesVAT Presentation: Key Concepts ExplainedKartik VermaNo ratings yet

- Balance Sheet Analysis Sources of FundsDocument4 pagesBalance Sheet Analysis Sources of FundsMohammad Asraf Ul HaqueNo ratings yet

- TAX Chapter 6Document4 pagesTAX Chapter 6Myz MessyNo ratings yet

- Financial Accounting: by Prof. Anirban DuttaDocument18 pagesFinancial Accounting: by Prof. Anirban DuttaDixith GandheNo ratings yet

- Series 6 Study SheetDocument14 pagesSeries 6 Study SheetJoseph BarozNo ratings yet

- Capita GainsDocument3 pagesCapita GainsAdeem AshrafiNo ratings yet

- PURCHASE FUNCTIONING AacountsDocument13 pagesPURCHASE FUNCTIONING AacountsVrushali JadhavNo ratings yet

- Ajay Pillai Finanacial Report-2Document10 pagesAjay Pillai Finanacial Report-2Ajay PillaiNo ratings yet

- Cash Flow StatementDocument18 pagesCash Flow StatementSriram BastolaNo ratings yet

- Cash Flow Statement ExplainedDocument15 pagesCash Flow Statement ExplainedJose Miguel TorresNo ratings yet

- ?UTF 8?B?TGVjdHVyZTA4LnBkZg ? 2Document66 pages?UTF 8?B?TGVjdHVyZTA4LnBkZg ? 2MAINY RYANNo ratings yet

- Rules On Gross Income TaxationDocument15 pagesRules On Gross Income TaxationEar TanNo ratings yet

- CTPM 2Document38 pagesCTPM 2abh ljknNo ratings yet

- As 9Document27 pagesAs 9AATHARSH RADHAKRISHNANNo ratings yet

- Financial Accounting: Session - 16: Accounting For EquityDocument11 pagesFinancial Accounting: Session - 16: Accounting For EquitySuraj KumarNo ratings yet

- Vat Input and Output TaxDocument137 pagesVat Input and Output TaxLen100% (1)

- Chapter 3 NotesDocument3 pagesChapter 3 NoteshannahandrearosarioNo ratings yet

- CH09 - Intermediate AccountingDocument34 pagesCH09 - Intermediate Accountingklebek100% (1)

- Delaunay Triangulation As A New Coverage MeasurementDocument230 pagesDelaunay Triangulation As A New Coverage MeasurementMohit GuptaNo ratings yet

- Discover Your Personality TreeDocument1 pageDiscover Your Personality TreeDeepak VermaNo ratings yet

- 52.139 Computer Organisation and DesignDocument8 pages52.139 Computer Organisation and DesignMohit GuptaNo ratings yet

- Dining Philosophers in E.S.DDocument2 pagesDining Philosophers in E.S.DMohit GuptaNo ratings yet

- Corporate Etiquette Handout PDFDocument3 pagesCorporate Etiquette Handout PDFMohit GuptaNo ratings yet

- Investor Guide BookDocument169 pagesInvestor Guide BooktonyvinayakNo ratings yet

- Finite State Machine Traffic Light ControlDocument3 pagesFinite State Machine Traffic Light ControlMohit GuptaNo ratings yet

- Chapter 2Document6 pagesChapter 2Tarciso FerreiraNo ratings yet

- Gas Control - Case Study: TopicDocument5 pagesGas Control - Case Study: TopicMohit GuptaNo ratings yet

- SecretarialDocument16 pagesSecretarialMohit GuptaNo ratings yet

- Business LawDocument3 pagesBusiness LawMohit GuptaNo ratings yet

- Investor Grievance Complaint & Arbitration ProceedingDocument44 pagesInvestor Grievance Complaint & Arbitration ProceedingMohit GuptaNo ratings yet

- Book Building Process: BY Atul ChikersalDocument20 pagesBook Building Process: BY Atul ChikersalMohit GuptaNo ratings yet

- Depository Participants Part - I: Presented By:-Mr. Vinay Mahajan Assistant General Manager & Compliance OfficerDocument70 pagesDepository Participants Part - I: Presented By:-Mr. Vinay Mahajan Assistant General Manager & Compliance OfficerMohit GuptaNo ratings yet

- Gas Control - Case Study: TopicDocument5 pagesGas Control - Case Study: TopicMohit GuptaNo ratings yet

- Depository Participants Part - I: Presented By:-Mr. Vinay Mahajan Assistant General Manager & Compliance OfficerDocument70 pagesDepository Participants Part - I: Presented By:-Mr. Vinay Mahajan Assistant General Manager & Compliance OfficerMohit GuptaNo ratings yet

- Traffic Light ControlDocument7 pagesTraffic Light ControlyuvaranzNo ratings yet

- View Certi If CateDocument1 pageView Certi If CateMahfuzur Rahman0% (3)

- Furukawa Electric Autoparts Philippines IncDocument1 pageFurukawa Electric Autoparts Philippines IncMary Cris GenilNo ratings yet

- CIR Appeals CTA Ruling on ICC Tax DeductionsDocument4 pagesCIR Appeals CTA Ruling on ICC Tax DeductionsJane MarianNo ratings yet

- Case 15-2. Dixon :ompany: 15-201.l Compo1ition of Total Co1t. The Total Cost of A Concraet Is TheDocument2 pagesCase 15-2. Dixon :ompany: 15-201.l Compo1ition of Total Co1t. The Total Cost of A Concraet Is TheJayesh WNo ratings yet

- Taxation Laws and Practice in BangladeshDocument26 pagesTaxation Laws and Practice in BangladeshZafour80% (10)

- DR - Pss Study Material Tax Law 1Document395 pagesDR - Pss Study Material Tax Law 1leela naga janaki rajitha attiliNo ratings yet

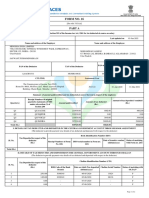

- FORM 16 TDS CERTIFICATEDocument8 pagesFORM 16 TDS CERTIFICATESaleemNo ratings yet

- PUP College of Law Midterm Taxation Law ExamDocument3 pagesPUP College of Law Midterm Taxation Law ExamAlfred Robert BabasoroNo ratings yet

- 1smied Vs CirDocument2 pages1smied Vs CirBam BathanNo ratings yet

- Classification of TaxesDocument3 pagesClassification of TaxesRomela Jean OcarizaNo ratings yet

- Tax Deposit-Challan 281-Excel FormatDocument8 pagesTax Deposit-Challan 281-Excel FormatMahaveer DhelariyaNo ratings yet

- Strategic Options for Sure Pass GroupDocument12 pagesStrategic Options for Sure Pass GroupstacyyauNo ratings yet

- Case DigestDocument5 pagesCase DigestGabriel Jhick SaliwanNo ratings yet

- TaxDocument2 pagesTaxnomercykillingNo ratings yet

- S C Test Bank Income TaxationDocument135 pagesS C Test Bank Income Taxationthenikkitr50% (6)

- Cash Budget: Month: April May June Cash Receipts Total Receipts 161,200 166,400 173,200 Cash OutflowsDocument5 pagesCash Budget: Month: April May June Cash Receipts Total Receipts 161,200 166,400 173,200 Cash OutflowsMenodiado FamNo ratings yet

- Employee tax certificationDocument3 pagesEmployee tax certificationCharlyster LisondraNo ratings yet

- 76920bos61942 1Document8 pages76920bos61942 1bhatjanardhan2000No ratings yet

- Invoice - Book RK JainDocument2 pagesInvoice - Book RK JainAbhi GargNo ratings yet

- 809 Premium Calculator of LIC Jeevan VaibhavDocument1 page809 Premium Calculator of LIC Jeevan VaibhavKiti MahajanNo ratings yet

- Commissioner of Internal Revenue vs. de La Salle University, Inc., 808 SCRA 156, November 09, 2016Document11 pagesCommissioner of Internal Revenue vs. de La Salle University, Inc., 808 SCRA 156, November 09, 2016Jane BandojaNo ratings yet

- CIR v. San Miguel Corporation (180740) (180910) 11-11-2019 CDDocument2 pagesCIR v. San Miguel Corporation (180740) (180910) 11-11-2019 CDAnime FreakNo ratings yet

- My Pay PDFDocument1 pageMy Pay PDFbuckwheat122507No ratings yet

- RA-NH Tie Up FareDocument11 pagesRA-NH Tie Up FareSanjog PandeyNo ratings yet

- M7 Donor's TaxDocument31 pagesM7 Donor's TaxChris MartinezNo ratings yet

- 421-A: Affordable New York Page Sept. 2019Document5 pages421-A: Affordable New York Page Sept. 2019Norman OderNo ratings yet

- Ias 1 QuestionsDocument7 pagesIas 1 QuestionsIssa AdiemaNo ratings yet

- CFP Tax Planning & Estate Planning Practice Book SampleDocument35 pagesCFP Tax Planning & Estate Planning Practice Book SampleMeenakshi100% (1)

- Richland School District Two 2022-2023 Budget FIRST READINGDocument2 pagesRichland School District Two 2022-2023 Budget FIRST READINGWLTXNo ratings yet

- Chapt 1 - Introduction To Public FinanceDocument12 pagesChapt 1 - Introduction To Public FinanceYitera SisayNo ratings yet

- You Can't Joke About That: Why Everything Is Funny, Nothing Is Sacred, and We're All in This TogetherFrom EverandYou Can't Joke About That: Why Everything Is Funny, Nothing Is Sacred, and We're All in This TogetherNo ratings yet

- Lessons from Tara: Life Advice from the World's Most Brilliant DogFrom EverandLessons from Tara: Life Advice from the World's Most Brilliant DogRating: 4.5 out of 5 stars4.5/5 (42)

- Sexual Bloopers: An Outrageous, Uncensored Collection of People's Most Embarrassing X-Rated FumblesFrom EverandSexual Bloopers: An Outrageous, Uncensored Collection of People's Most Embarrassing X-Rated FumblesRating: 3.5 out of 5 stars3.5/5 (7)

- The Importance of Being Earnest: Classic Tales EditionFrom EverandThe Importance of Being Earnest: Classic Tales EditionRating: 4.5 out of 5 stars4.5/5 (42)

- Welcome to the United States of Anxiety: Observations from a Reforming NeuroticFrom EverandWelcome to the United States of Anxiety: Observations from a Reforming NeuroticRating: 3.5 out of 5 stars3.5/5 (10)

- The House at Pooh Corner - Winnie-the-Pooh Book #4 - UnabridgedFrom EverandThe House at Pooh Corner - Winnie-the-Pooh Book #4 - UnabridgedRating: 4.5 out of 5 stars4.5/5 (5)

- The Asshole Survival Guide: How to Deal with People Who Treat You Like DirtFrom EverandThe Asshole Survival Guide: How to Deal with People Who Treat You Like DirtRating: 4 out of 5 stars4/5 (60)

- The Inimitable Jeeves [Classic Tales Edition]From EverandThe Inimitable Jeeves [Classic Tales Edition]Rating: 5 out of 5 stars5/5 (3)

- Other People's Dirt: A Housecleaner's Curious AdventuresFrom EverandOther People's Dirt: A Housecleaner's Curious AdventuresRating: 3.5 out of 5 stars3.5/5 (104)

- The Smartest Book in the World: A Lexicon of Literacy, A Rancorous Reportage, A Concise Curriculum of CoolFrom EverandThe Smartest Book in the World: A Lexicon of Literacy, A Rancorous Reportage, A Concise Curriculum of CoolRating: 4 out of 5 stars4/5 (14)

- The Comedians in Cars Getting Coffee BookFrom EverandThe Comedians in Cars Getting Coffee BookRating: 4.5 out of 5 stars4.5/5 (8)

- Tidy the F*ck Up: The American Art of Organizing Your Sh*tFrom EverandTidy the F*ck Up: The American Art of Organizing Your Sh*tRating: 4.5 out of 5 stars4.5/5 (99)

- Humorous American Short Stories: Selections from Mark Twain, O. Henry, James Thurber, Kurt Vonnegut, Jr. and moreFrom EverandHumorous American Short Stories: Selections from Mark Twain, O. Henry, James Thurber, Kurt Vonnegut, Jr. and moreNo ratings yet

- The Best Joke Book (Period): Hundreds of the Funniest, Silliest, Most Ridiculous Jokes EverFrom EverandThe Best Joke Book (Period): Hundreds of the Funniest, Silliest, Most Ridiculous Jokes EverRating: 3.5 out of 5 stars3.5/5 (4)