You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- September 11 Commission Report Revised December 2008Document381 pagesSeptember 11 Commission Report Revised December 2008ep heidner100% (17)

- Certificate: Reva Institute of Science and ManagementDocument1 pageCertificate: Reva Institute of Science and ManagementnithinjmjNo ratings yet

- Review of Literature & Design of The Study: Market Segmention Is A Group of People or Organizations Sharing One orDocument1 pageReview of Literature & Design of The Study: Market Segmention Is A Group of People or Organizations Sharing One ornithinjmjNo ratings yet

- 2.2 Review of LiteratureDocument3 pages2.2 Review of LiteraturenithinjmjNo ratings yet

- Organisational StudyDocument8 pagesOrganisational StudynithinjmjNo ratings yet

- Balance Sheet of Indusind Bank - in Rs. Cr.Document1 pageBalance Sheet of Indusind Bank - in Rs. Cr.nithinjmjNo ratings yet

- Pricing Case Study - Penetrative Pricing of Jio (Impact On The Industry) 4Document4 pagesPricing Case Study - Penetrative Pricing of Jio (Impact On The Industry) 4Vyshnavi L RNo ratings yet

- Citi Short Sale Approval Letter (Non-GSE)Document2 pagesCiti Short Sale Approval Letter (Non-GSE)kwillsonNo ratings yet

- Sbi Corporate Credit CardDocument9 pagesSbi Corporate Credit CardArvindNo ratings yet

- GL Account Balance QueryDocument5 pagesGL Account Balance QueryKhalil ShafeekNo ratings yet

- 3 de Thi ToeicDocument115 pages3 de Thi ToeicTiểu MinhNo ratings yet

- NIC Account BenefitsDocument4 pagesNIC Account BenefitsAnkit UpretyNo ratings yet

- Fema Add CHDocument54 pagesFema Add CHMukesh DholakiaNo ratings yet

- Bank Statement 1 Fusionn 1 PDFDocument6 pagesBank Statement 1 Fusionn 1 PDFBenny BerniceNo ratings yet

- FM - 1 - Accounts of Professional PersonsDocument15 pagesFM - 1 - Accounts of Professional Personsyagnesh trivedi100% (1)

- Defining General Options AddendumDocument16 pagesDefining General Options AddendumchinnaNo ratings yet

- Marquez Vs Desierto DigestDocument2 pagesMarquez Vs Desierto DigestKathleen CruzNo ratings yet

- RBS & Faysal BankDocument13 pagesRBS & Faysal BankOmer MirzaNo ratings yet

- Uan B.inggeris 1990-20088dDocument211 pagesUan B.inggeris 1990-20088dPhyan HyunNo ratings yet

- A Project Report: "Analysis of Banks Using Camels Approach''Document41 pagesA Project Report: "Analysis of Banks Using Camels Approach''Siddarth JainNo ratings yet

- Hotel Details Check in Check Out Rooms: Guest Name: DateDocument1 pageHotel Details Check in Check Out Rooms: Guest Name: DateAARTI AHIRWARNo ratings yet

- Unit - 3 Bank Reconciliation StatementDocument21 pagesUnit - 3 Bank Reconciliation StatementMrutyunjay SaramandalNo ratings yet

- Tanzania To Start Tests On 542km Long New Mtwara-Dar Gas Pipeline - BusinessDocument3 pagesTanzania To Start Tests On 542km Long New Mtwara-Dar Gas Pipeline - BusinessEng Kombe ChemicalNo ratings yet

- Factoring As An Important Tool For Working Capital ManagementDocument25 pagesFactoring As An Important Tool For Working Capital ManagementRupal HatkarNo ratings yet

- Tutorial6 AnswersDocument3 pagesTutorial6 AnswersTosin OjoNo ratings yet

- FT Business EducationDocument76 pagesFT Business EducationDenis VarlamovNo ratings yet

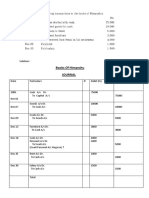

- Books of Himanshu JournalDocument4 pagesBooks of Himanshu Journalrakesh19865No ratings yet

- Venture Capital Financing in India 2Document48 pagesVenture Capital Financing in India 2Arpit Patel0% (1)

- Fee Information DocumentDocument2 pagesFee Information DocumentGsz Eli WongNo ratings yet

- Effect of Rajesh Tyagi CaseDocument40 pagesEffect of Rajesh Tyagi CasePrasannaKadethotaNo ratings yet

- Process Mapping Toolkit SummaryDocument2 pagesProcess Mapping Toolkit SummaryНебојша БабовићNo ratings yet

- Banking Finals Samplex Sample Answers (Ver.2)Document2 pagesBanking Finals Samplex Sample Answers (Ver.2)Florence RoseteNo ratings yet

- 2012 Jiao vs. NLRCDocument2 pages2012 Jiao vs. NLRCMa Gabriellen Quijada-Tabuñag100% (1)

- JP Morgan Chase Sues To Get Mortgage Loan Files Back From Ben Ezra... Ben Ezra Claims Chase Did Not Pay Its BillDocument59 pagesJP Morgan Chase Sues To Get Mortgage Loan Files Back From Ben Ezra... Ben Ezra Claims Chase Did Not Pay Its Bill83jjmackNo ratings yet

- Form 16 SV PDFDocument2 pagesForm 16 SV PDFPravin HireNo ratings yet