You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Citigroup Open Bank Assistance Unredacted FDIC Minutes From 23 Nov 2008 (Lawsuit #2)Document16 pagesCitigroup Open Bank Assistance Unredacted FDIC Minutes From 23 Nov 2008 (Lawsuit #2)Vern McKinleyNo ratings yet

- Saa Group Acca P4 Mock 2011Document9 pagesSaa Group Acca P4 Mock 2011afzal_abjaniNo ratings yet

- B B ADocument3 pagesB B AVaishnavi SubramanianNo ratings yet

- Project ReportDocument11 pagesProject Reportzahid mehmoodNo ratings yet

- Cross Border Transactions HandbookDocument232 pagesCross Border Transactions Handbookralphhvillanueva100% (2)

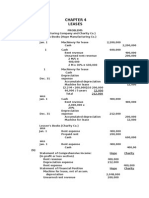

- Financial Accounting 2 Chapter 4Document27 pagesFinancial Accounting 2 Chapter 4Elijah Lou ViloriaNo ratings yet

- Project On Apex BankDocument32 pagesProject On Apex BankRishi Agarwal67% (3)

- Implementing Saudi Arabia's Vision 2030: An Interim Balance SheetDocument10 pagesImplementing Saudi Arabia's Vision 2030: An Interim Balance SheetCrown Center for Middle East StudiesNo ratings yet

- RBS Internship ReportDocument61 pagesRBS Internship ReportWaqas javed100% (3)

- Notice To Shareholders - Right of WithdrawalDocument2 pagesNotice To Shareholders - Right of WithdrawalJBS RINo ratings yet

- Sam Seiden CBOT KeepItSimpleDocument3 pagesSam Seiden CBOT KeepItSimpleferritape100% (2)

- ECP Advisors LLC Sept 2009Document10 pagesECP Advisors LLC Sept 2009Swapnilsagar VithalaniNo ratings yet

- 26 Li Yao vs. CIRDocument2 pages26 Li Yao vs. CIRMichelle Montenegro - AraujoNo ratings yet

- FAR Part 1 Quizbee - DifficultDocument4 pagesFAR Part 1 Quizbee - DifficultRosemarie Miano TrabucoNo ratings yet

- Cash Flow TheoryDocument50 pagesCash Flow TheoryJovelyn ManlucobNo ratings yet

- Case 4 2Document5 pagesCase 4 2Marjorie Morada67% (3)

- India International ExchangeDocument1 pageIndia International ExchangeSugan Pragasam100% (1)

- International Coal VenturesDocument3 pagesInternational Coal VenturesNeerajKumarNo ratings yet

- Dena Bank Working Capital and Ratio Analysis VinayDocument106 pagesDena Bank Working Capital and Ratio Analysis Vinayविनय गुप्ता75% (4)

- Urban Planning and Real Estate DevelopmentDocument5 pagesUrban Planning and Real Estate Developmentanon_145354896No ratings yet

- Benjamin Graham Articles Magazine of Wall Street 1917-1922Document142 pagesBenjamin Graham Articles Magazine of Wall Street 1917-1922Anonymous CP6MdC7S4TNo ratings yet

- The Role of Managerial Finance: All Rights ReservedDocument45 pagesThe Role of Managerial Finance: All Rights ReservedmoonaafreenNo ratings yet

- Macr Incentive FC Rec Mei 2012 - 1Document3,649 pagesMacr Incentive FC Rec Mei 2012 - 1Greget SekaliNo ratings yet

- The Rise of FinTech - Nov '14 PDFDocument26 pagesThe Rise of FinTech - Nov '14 PDFEdwin Shao0% (2)

- Dowdell PRDocument2 pagesDowdell PRreadthehookNo ratings yet

- Comparative Analysis of Mutual Fund of HDFC ICICIDocument33 pagesComparative Analysis of Mutual Fund of HDFC ICICIAniket Ramteke100% (1)

- CRUDE OIL Hedge-StrategyDocument4 pagesCRUDE OIL Hedge-StrategyNeelesh KamathNo ratings yet

- Product Sails5nwudeDocument10 pagesProduct Sails5nwuderakeshraj mahakudNo ratings yet

- Company Law Ii PDFDocument95 pagesCompany Law Ii PDFNYAMEKYE ADOMAKONo ratings yet

- The Time Value of Money: All Rights ReservedDocument55 pagesThe Time Value of Money: All Rights ReservedNad AdenanNo ratings yet