You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Uslovi Za Putno - EngleskiDocument15 pagesUslovi Za Putno - EngleskiJasmin TafićNo ratings yet

- Finacle Ebanking SolutionDocument2 pagesFinacle Ebanking SolutionGuru Narayanan0% (1)

- Iwokazpy Fo - QR Forj.K Fuxe Fyfevsm: Purvanchal Vidyut Vitaran Nigam LTDDocument2 pagesIwokazpy Fo - QR Forj.K Fuxe Fyfevsm: Purvanchal Vidyut Vitaran Nigam LTDShashank PandeyNo ratings yet

- Configure and Verify A Site To Site IPsec VPN Using CLIDocument4 pagesConfigure and Verify A Site To Site IPsec VPN Using CLICristhian HadesNo ratings yet

- 2023 M&A Trends ReportDocument16 pages2023 M&A Trends ReportFuture-Proof AdvisorsNo ratings yet

- ESSAR PartA Group09 PDFDocument8 pagesESSAR PartA Group09 PDFSwarnjeet Singh DhillonNo ratings yet

- Most Important Terms and ConditionsDocument22 pagesMost Important Terms and ConditionsAnkit PatelNo ratings yet

- Leslie Turner CH 8Document59 pagesLeslie Turner CH 8AYI FADILLAHNo ratings yet

- Returning Students - How To Make School Fees Payment Via InterswitchDocument9 pagesReturning Students - How To Make School Fees Payment Via InterswitchBolaji AwokiyesiNo ratings yet

- E Banking Chapter 3Document19 pagesE Banking Chapter 3Philip K BugaNo ratings yet

- M3 UNIT 5 AdvertisementDocument12 pagesM3 UNIT 5 AdvertisementJanet DiosanaNo ratings yet

- Lecture 02 - Inventory ManagementDocument69 pagesLecture 02 - Inventory ManagementBharath BalasubramanianNo ratings yet

- Mr. SHRIYANS DAFTARI bank account statement from 19 Dec 2022 to 20 Mar 2023Document12 pagesMr. SHRIYANS DAFTARI bank account statement from 19 Dec 2022 to 20 Mar 2023Shriyans DaftariNo ratings yet

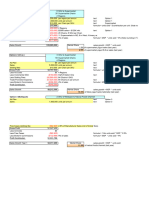

- Natureview Farm Case Calculations Pre-Class SpreadsheetDocument12 pagesNatureview Farm Case Calculations Pre-Class Spreadsheet1010478907No ratings yet

- HLB Receipt-2023-05-17 2Document3 pagesHLB Receipt-2023-05-17 2v6wxcvjmvgNo ratings yet

- NTB Promo Codes for Tax Payment, Cash Transactions & Group Account ManagementDocument9 pagesNTB Promo Codes for Tax Payment, Cash Transactions & Group Account ManagementYash JainNo ratings yet

- Colegio de Dagupan Arellano Street, Dagupan City School of Business and Accountancy Final Examination Auditing and Assurance PrincipleDocument16 pagesColegio de Dagupan Arellano Street, Dagupan City School of Business and Accountancy Final Examination Auditing and Assurance PrincipleFeelingerang MAYoraNo ratings yet

- Computer Networks Lesson Plan Materials Computer Networks Lesson Plan MaterialsDocument6 pagesComputer Networks Lesson Plan Materials Computer Networks Lesson Plan MaterialsAldrin Canicula CompetenteNo ratings yet

- S HW T9 Z W95 X CB GXVeDocument10 pagesS HW T9 Z W95 X CB GXVehosantoshNo ratings yet

- No BordersDocument1 pageNo BordersCathy GabroninoNo ratings yet

- Dessler 13Document14 pagesDessler 13Victoria EyelashesNo ratings yet

- 2014 Bar Examinations - InsuranceDocument2 pages2014 Bar Examinations - InsurancesiaoNo ratings yet

- Fact Orders Tec Stored A To S 2022Document2,364 pagesFact Orders Tec Stored A To S 2022Mikel SUAREZ BARREIRONo ratings yet

- Auditing Concepts PSA Based QuestionsDocument560 pagesAuditing Concepts PSA Based QuestionsNir Noel Aquino100% (12)

- PFRS 17 Insurance ContractsDocument13 pagesPFRS 17 Insurance ContractsAlex OngNo ratings yet

- International Commercial Terms (INCOTERMS)Document9 pagesInternational Commercial Terms (INCOTERMS)albertNo ratings yet

- InsuranceDocument12 pagesInsuranceRupa MohalanobishNo ratings yet

- Optimize Network Traffic and Security with Allot ProductsDocument10 pagesOptimize Network Traffic and Security with Allot ProductsPandu PriambodoNo ratings yet

- SWOT Analysis of ICICI Bank Reveals Strengths and Growth OpportunitiesDocument6 pagesSWOT Analysis of ICICI Bank Reveals Strengths and Growth Opportunitiessouvikrock12No ratings yet

- Credit Card Balance Transfer FormDocument2 pagesCredit Card Balance Transfer FormTanvir AhmedNo ratings yet