You might also like

- Process of MergerDocument7 pagesProcess of MergerSankalp RajNo ratings yet

- Key Steps Before Talking To Venture Capitalists - Intel Capital PDFDocument7 pagesKey Steps Before Talking To Venture Capitalists - Intel Capital PDFSam100% (1)

- The Banewarrens PDFDocument138 pagesThe Banewarrens PDFSaint_Timonious100% (8)

- Foreign Ownership Rules in The PhilippinesDocument13 pagesForeign Ownership Rules in The PhilippinesAustin Viel Lagman MedinaNo ratings yet

- Venture Capital FundamentalsDocument13 pagesVenture Capital Fundamentalsdch204No ratings yet

- Sally JamesonDocument3 pagesSally JamesonMithun Sridharan100% (2)

- Citigroup Practical Banking Pres 06Document30 pagesCitigroup Practical Banking Pres 06jwkNo ratings yet

- Underwriting Placements and The Art of Investor Relations Presentation by Sherilyn Foong Alliance Investment Bank Berhad MalaysiaDocument25 pagesUnderwriting Placements and The Art of Investor Relations Presentation by Sherilyn Foong Alliance Investment Bank Berhad MalaysiaPramod GosaviNo ratings yet

- Bain - Mergers & AcquisitionsDocument2 pagesBain - Mergers & AcquisitionsddubyaNo ratings yet

- Bob Robotti - Navigating Deep WatersDocument35 pagesBob Robotti - Navigating Deep WatersCanadianValueNo ratings yet

- Corp. Gov. Lessons From Enron PDFDocument6 pagesCorp. Gov. Lessons From Enron PDFRatnesh SinghNo ratings yet

- Creating Starting Business Plan VentureDocument24 pagesCreating Starting Business Plan VenturesagartolaneyNo ratings yet

- PartnershipDocument15 pagesPartnershipchowchow12364% (11)

- Eil RFQDocument221 pagesEil RFQBIRANCHI100% (1)

- Perception of Derivatives at SMC Investment Project ReportDocument108 pagesPerception of Derivatives at SMC Investment Project ReportBabasab Patil (Karrisatte)No ratings yet

- Chapter 4 Oppotunity ScreeningDocument20 pagesChapter 4 Oppotunity ScreeningClarissNo ratings yet

- Square PharmaDocument23 pagesSquare PharmaSabrina SamantaNo ratings yet

- CSR Strategy For Sustainable Business Samy Odemilin and BamptonDocument16 pagesCSR Strategy For Sustainable Business Samy Odemilin and BamptonabbakaNo ratings yet

- 17.MARK-monserrat Vs CeronDocument2 pages17.MARK-monserrat Vs CeronbowbingNo ratings yet

- TATA-TEA Project ReportDocument33 pagesTATA-TEA Project Reportsujata shah82% (11)

- 9 NV HGWX 45 ZB YRE4 FDocument2 pages9 NV HGWX 45 ZB YRE4 FBadam VenkatareddyNo ratings yet

- 9 NV HGWX 45 ZB YRE4 FDocument2 pages9 NV HGWX 45 ZB YRE4 FBadam VenkatareddyNo ratings yet

- Chap12 MbaDocument40 pagesChap12 MbaMehar Sheikh100% (1)

- Mergers Acquisitions 41323 25082Document21 pagesMergers Acquisitions 41323 25082Sheetal VermaNo ratings yet

- Buying an Existing Business GuideDocument24 pagesBuying an Existing Business GuideberkNo ratings yet

- Valuation-Methods and ParametersDocument15 pagesValuation-Methods and ParametersPranav Chaudhari100% (2)

- 1-10 Key Considerations For Going Public With A SPAC - Corporate - Commercial Law - United StatesDocument3 pages1-10 Key Considerations For Going Public With A SPAC - Corporate - Commercial Law - United Statespayal chaudhariNo ratings yet

- Precedent Transaction Homework Assignment-2Document8 pagesPrecedent Transaction Homework Assignment-2amelie romainNo ratings yet

- 9-25-07 Valuations in Family BDocument44 pages9-25-07 Valuations in Family BZhebin ZhangNo ratings yet

- 10 Factors to Consider Before Entering International MarketsDocument4 pages10 Factors to Consider Before Entering International MarketsSoria Zoon HaiderNo ratings yet

- Raising Venture Capital: For Private Circulation OnlyDocument18 pagesRaising Venture Capital: For Private Circulation OnlyCma Pankaj JainNo ratings yet

- Keys For An Effective Business Plan: Business Planning Workshop September 27, 2006Document61 pagesKeys For An Effective Business Plan: Business Planning Workshop September 27, 2006Tan Tok HoiNo ratings yet

- Business Analysis Checklist Growbridge Advisors LTDDocument11 pagesBusiness Analysis Checklist Growbridge Advisors LTDNishok VirurchNo ratings yet

- Dissertation On Ipo in IndiaDocument5 pagesDissertation On Ipo in IndiaCheapestPaperWritingServiceSingapore100% (1)

- Mergers & Acquisitions: 10 Solid Reasons To Support An Acquisition StrategyDocument2 pagesMergers & Acquisitions: 10 Solid Reasons To Support An Acquisition StrategyCatherine JohnsonNo ratings yet

- MAPEDocument7 pagesMAPEcheif sNo ratings yet

- Business Analysis & Valuation: Using Financial StatementsDocument67 pagesBusiness Analysis & Valuation: Using Financial StatementsVan-Hu NguyenNo ratings yet

- Valuation For M&a Parag Ved MumbaiDocument22 pagesValuation For M&a Parag Ved MumbaiRavikumar KurnalNo ratings yet

- FinanceDocument8 pagesFinancepiyush kumarNo ratings yet

- VALUATIONDocument48 pagesVALUATIONIshika ParasrampuriaNo ratings yet

- Umbrex Commercial Due Diligence Playbook First EDocument102 pagesUmbrex Commercial Due Diligence Playbook First EAlexandre GoncalvesNo ratings yet

- Informal Risk Capital and Venture Capital,: Hisrich Peters ShepherdDocument59 pagesInformal Risk Capital and Venture Capital,: Hisrich Peters ShepherdAYONA P SNo ratings yet

- Mergers & Acquisitions in India - December 2014Document12 pagesMergers & Acquisitions in India - December 2014Ankit JainNo ratings yet

- Sources of Financing: Debt and EquityDocument26 pagesSources of Financing: Debt and EquitykalyaniduttaNo ratings yet

- 03 Success of Equity Funding Deal v2 11-07-2020 AJDocument42 pages03 Success of Equity Funding Deal v2 11-07-2020 AJarunjoshi12345No ratings yet

- COMPARATIVE EQUITY ANALYSIS OF BANKING AND IT SECTOR - INDIABULLS - Plega NewDocument97 pagesCOMPARATIVE EQUITY ANALYSIS OF BANKING AND IT SECTOR - INDIABULLS - Plega NewMohmmedKhayyumNo ratings yet

- Identifying and Analyzing Domestic and International OpportunitiesDocument32 pagesIdentifying and Analyzing Domestic and International OpportunitiesNM.ZIHANNo ratings yet

- Internal Assessment based on Summer Internship at Praedico Global ResearchDocument3 pagesInternal Assessment based on Summer Internship at Praedico Global ResearchNishant BhartiNo ratings yet

- Corporate Restructuring and M&A StrategiesDocument15 pagesCorporate Restructuring and M&A StrategiesJay BhattNo ratings yet

- Chapter 5Document40 pagesChapter 5RV EntertainmentNo ratings yet

- Level Ii Developing Business PracticeDocument62 pagesLevel Ii Developing Business PracticetomNo ratings yet

- Business Plan ToolkitDocument22 pagesBusiness Plan ToolkitantonhayeNo ratings yet

- 6 Lessons: Markets in 2018Document15 pages6 Lessons: Markets in 2018devdliveNo ratings yet

- FINA4050 Class 7 Payment and Legal ConsiderationsDocument25 pagesFINA4050 Class 7 Payment and Legal ConsiderationsJai PaulNo ratings yet

- Developing A Viable Business Model: Patrick BarryDocument19 pagesDeveloping A Viable Business Model: Patrick BarryCocoNo ratings yet

- Trica - The Private Market MonitorDocument89 pagesTrica - The Private Market MonitoraashinerrNo ratings yet

- Fundamental Analysis: A Step-by-Step Guide to Evaluating StocksDocument9 pagesFundamental Analysis: A Step-by-Step Guide to Evaluating StockskazminoNo ratings yet

- S1 IntroDocument20 pagesS1 IntroMayank SinghNo ratings yet

- Company and Mutual Fund DetailsDocument53 pagesCompany and Mutual Fund DetailsChintan PavsiyaNo ratings yet

- Crafting A Winning Business PlanDocument24 pagesCrafting A Winning Business PlanWahid RokadiyaNo ratings yet

- Mergers and AcquisitionsDocument8 pagesMergers and AcquisitionsSudābe EynaliNo ratings yet

- Venture Financing: Process and Selection CriteriaDocument6 pagesVenture Financing: Process and Selection Criteriakartikay27No ratings yet

- Steps in M & A DealDocument8 pagesSteps in M & A DealMukund1211No ratings yet

- Developing A Viable Business Model: Patrick BarryDocument19 pagesDeveloping A Viable Business Model: Patrick BarryNirmalya MukherjeeNo ratings yet

- Comparative Analysis of Investment OptionsDocument47 pagesComparative Analysis of Investment Optionsnayan_vet78% (9)

- Chapter 5 - Part 1Document50 pagesChapter 5 - Part 1Kiều PhươngNo ratings yet

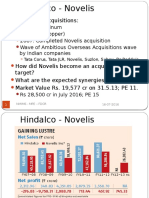

- Hindalco's Acquisition of Novelis and Expected SynergiesDocument16 pagesHindalco's Acquisition of Novelis and Expected SynergiesLalNo ratings yet

- Identifying and Analyzing Domestic and International OpportunitiesDocument28 pagesIdentifying and Analyzing Domestic and International OpportunitiesDani DaniNo ratings yet

- HSI A Guide To Raising Capital For Business GrowthDocument22 pagesHSI A Guide To Raising Capital For Business GrowthAli Gokhan KocanNo ratings yet

- Corporate PresentationDocument46 pagesCorporate PresentationBadam VenkatareddyNo ratings yet

- Competing in A Flat WorldDocument9 pagesCompeting in A Flat WorldBadam VenkatareddyNo ratings yet

- Balancing Innovation TechnologyDocument18 pagesBalancing Innovation TechnologyBadam VenkatareddyNo ratings yet

- Securitization ProcessDocument62 pagesSecuritization Processbablu991No ratings yet

- Barriers of QWLDocument14 pagesBarriers of QWLAlak Malik100% (1)

- Monetary PolicyDocument44 pagesMonetary PolicyYogesh BhitalwalNo ratings yet

- MFunds Ch9Document10 pagesMFunds Ch9itmnavimumbaiNo ratings yet

- Inflation N Stock PriceDocument5 pagesInflation N Stock PricesrishtikailashNo ratings yet

- Risk ManagementDocument2 pagesRisk ManagementBadam VenkatareddyNo ratings yet

- IKEADocument7 pagesIKEAGery Rheynhard ManurungNo ratings yet

- Ledger - Ajanta Shoes (India) Private LimitedDocument10 pagesLedger - Ajanta Shoes (India) Private LimitedSuraj MehtaNo ratings yet

- CAPE Economics 2007 U1 P1Document10 pagesCAPE Economics 2007 U1 P1aliciaNo ratings yet

- Harga Mesin Jahit Typical:: Juki DDL 8100eDocument2 pagesHarga Mesin Jahit Typical:: Juki DDL 8100eRismapleNo ratings yet

- Chapter 2 The Firm and Its GoalDocument36 pagesChapter 2 The Firm and Its GoalMon HươngNo ratings yet

- CBMDocument31 pagesCBMGaurav BhaleraoNo ratings yet

- HDFC AgroDocument2 pagesHDFC Agrovinit kumar singhNo ratings yet

- Stock - Questionnaire For Internal ControlDocument3 pagesStock - Questionnaire For Internal ControlBindu RaoNo ratings yet

- Advantages and Disadvantages of The FloatingDocument22 pagesAdvantages and Disadvantages of The FloatingFarhana KhanNo ratings yet

- Carol Lam Appointed Chief Creative Officer and Managing Director For DDB Group Hong KongDocument2 pagesCarol Lam Appointed Chief Creative Officer and Managing Director For DDB Group Hong KongDDBcomPRNo ratings yet

- Understanding Company LawDocument13 pagesUnderstanding Company LawUditaNo ratings yet

- Name: Barnabas Ikpefuan Wallet Number: 9163284136Document45 pagesName: Barnabas Ikpefuan Wallet Number: 9163284136Barnabas IkpefuanNo ratings yet

- Chief Operating Officer in NYC Resume William HoganDocument3 pagesChief Operating Officer in NYC Resume William HoganWilliamHoganNo ratings yet

- Bharati Vidyapeeth Deemed University, Pune: Institute of Management andDocument32 pagesBharati Vidyapeeth Deemed University, Pune: Institute of Management andLainious Rai50% (2)

- Solution Ch#11Document13 pagesSolution Ch#11usman aliNo ratings yet

- A New Breed of Travel Agent Is Winning Over The Hearts and Wallets of ConsumersDocument3 pagesA New Breed of Travel Agent Is Winning Over The Hearts and Wallets of ConsumersBrian Ainsley HornNo ratings yet

- Advanced Financial Reporting and Theory 26325 Module Leader: Pat MouldDocument8 pagesAdvanced Financial Reporting and Theory 26325 Module Leader: Pat MouldKaran ChopraNo ratings yet

- A Tale of Two TradersDocument4 pagesA Tale of Two Tradersmayankjain24inNo ratings yet

- 068 Prequalification For Solid Waste MGTDocument29 pages068 Prequalification For Solid Waste MGTapi-257737819No ratings yet

- Regn of Cooperative Housing Socities PDFDocument6 pagesRegn of Cooperative Housing Socities PDFArindam MoulickNo ratings yet