You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Market Outlook Report 4 JuneDocument4 pagesMarket Outlook Report 4 JunezenergynzNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Market Outlook Report 20 May 3013Document4 pagesMarket Outlook Report 20 May 3013zenergynzNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Market Outlook Report 4 March 2013Document4 pagesMarket Outlook Report 4 March 2013zenergynzNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

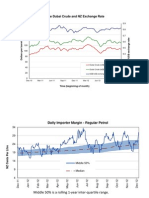

- Weekly Average Dubai Crude and NZ Exchange Rate: Time (Beginning of Month)Document8 pagesWeekly Average Dubai Crude and NZ Exchange Rate: Time (Beginning of Month)zenergynzNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Market Outlook Report 6 May 2013Document4 pagesMarket Outlook Report 6 May 2013zenergynzNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Market Outlook Report 10 December 2012Document4 pagesMarket Outlook Report 10 December 2012zenergynzNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Market Outlook Report 8 AprilDocument5 pagesMarket Outlook Report 8 AprilzenergynzNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Market Outlook Report 6 May 2013Document4 pagesMarket Outlook Report 6 May 2013zenergynzNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Market Outlook Report 22 April 2013Document4 pagesMarket Outlook Report 22 April 2013zenergynzNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- Market Outlook Report 18 March 2013Document4 pagesMarket Outlook Report 18 March 2013zenergynzNo ratings yet

- Market Outlook Report 5 February 2012Document4 pagesMarket Outlook Report 5 February 2012zenergynzNo ratings yet

- Market Outlook Report 18 February 2013Document4 pagesMarket Outlook Report 18 February 2013zenergynzNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Market Outlook Report 12 November 2012Document4 pagesMarket Outlook Report 12 November 2012zenergynzNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Market Outlook Report 26 November 2012Document4 pagesMarket Outlook Report 26 November 2012zenergynzNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Energy Drop - October 12Document4 pagesThe Energy Drop - October 12zenergynzNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Market Outlook Report 29 October 2012Document4 pagesMarket Outlook Report 29 October 2012zenergynzNo ratings yet

- Market Outlook Report 15 October 2012Document4 pagesMarket Outlook Report 15 October 2012zenergynzNo ratings yet

- The Energy Drop - November 12Document4 pagesThe Energy Drop - November 12zenergynzNo ratings yet

- Market Outlook Report 1 October 2012Document4 pagesMarket Outlook Report 1 October 2012zenergynzNo ratings yet

- The Energy Drop - September 12Document4 pagesThe Energy Drop - September 12zenergynzNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Market Outlook Report 20 August 2012Document4 pagesMarket Outlook Report 20 August 2012zenergynzNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Market Outlook Report 17 September 2012Document4 pagesMarket Outlook Report 17 September 2012zenergynzNo ratings yet

- The Energy Drop - July 12Document4 pagesThe Energy Drop - July 12zenergynzNo ratings yet

- Market Outlook Report 3 September 2012Document4 pagesMarket Outlook Report 3 September 2012zenergynzNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Market Outlook Report 6 August 2012Document4 pagesMarket Outlook Report 6 August 2012zenergynzNo ratings yet

- The Energy Drop - June 12Document4 pagesThe Energy Drop - June 12zenergynzNo ratings yet

- Regal Haulage Help Us Trial Our New Truck Stop Cardreaders: Z.co - NZDocument4 pagesRegal Haulage Help Us Trial Our New Truck Stop Cardreaders: Z.co - NZzenergynzNo ratings yet

- Market Outlook Report 23 July 2012Document4 pagesMarket Outlook Report 23 July 2012zenergynzNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Market Outlook #2 9 July 2012Document4 pagesMarket Outlook #2 9 July 2012zenergynzNo ratings yet

- HealthFlex Dave BauzonDocument10 pagesHealthFlex Dave BauzonNino Dave Bauzon100% (1)

- DEFCON ManualDocument13 pagesDEFCON Manualbuyvalve100% (1)

- ABN AMRO Holding N.V. 2009 Annual ReportDocument243 pagesABN AMRO Holding N.V. 2009 Annual ReportF.N. HeinsiusNo ratings yet

- City Gas Distribution ReportDocument22 pagesCity Gas Distribution Reportdimple1101100% (9)

- Statement of PurposeDocument2 pagesStatement of Purposearmaan kaurNo ratings yet

- Savable Data Page - Its Configuration, Usage & ExecutionDocument20 pagesSavable Data Page - Its Configuration, Usage & ExecutionsurmanpaNo ratings yet

- Lead Magnet 43 Foolproof Strategies To Get More Leads, Win A Ton of New Customers and Double Your Profits in Record Time... (RDocument189 pagesLead Magnet 43 Foolproof Strategies To Get More Leads, Win A Ton of New Customers and Double Your Profits in Record Time... (RluizdasilvaazevedoNo ratings yet

- Software Engineering Modern ApproachesDocument775 pagesSoftware Engineering Modern ApproachesErico Antonio TeixeiraNo ratings yet

- Determining Total Impulse and Specific Impulse From Static Test DataDocument4 pagesDetermining Total Impulse and Specific Impulse From Static Test Datajai_selvaNo ratings yet

- Memento Mori: March/April 2020Document109 pagesMemento Mori: March/April 2020ICCFA StaffNo ratings yet

- Request For AffidavitDocument2 pagesRequest For AffidavitGhee MoralesNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- HSPA+ Compressed ModeDocument10 pagesHSPA+ Compressed ModeAkhtar KhanNo ratings yet

- Lesson 3 - Materials That Undergo DecayDocument14 pagesLesson 3 - Materials That Undergo DecayFUMIKO SOPHIA67% (6)

- Sap Fi/Co: Transaction CodesDocument51 pagesSap Fi/Co: Transaction CodesReddaveni NagarajuNo ratings yet

- Checklist PBL 2Document3 pagesChecklist PBL 2Hazrina AwangNo ratings yet

- Unit 13 AminesDocument3 pagesUnit 13 AminesArinath DeepaNo ratings yet

- Iso 4624Document15 pagesIso 4624klkopopoonetdrghjktl100% (2)

- UBI1Document66 pagesUBI1Rudra SinghNo ratings yet

- BCM Risk Management and Compliance Training in JakartaDocument2 pagesBCM Risk Management and Compliance Training in Jakartaindra gNo ratings yet

- A CASE STUDY OF AU SMALL FINANCE BANK'S SHRIRAMPUR BRANCHDocument9 pagesA CASE STUDY OF AU SMALL FINANCE BANK'S SHRIRAMPUR BRANCHprajakta shindeNo ratings yet

- Embedded Systems: Martin Schoeberl Mschoebe@mail - Tuwien.ac - atDocument27 pagesEmbedded Systems: Martin Schoeberl Mschoebe@mail - Tuwien.ac - atDhirenKumarGoleyNo ratings yet

- Alexander Lee ResumeDocument2 pagesAlexander Lee Resumeapi-352375940No ratings yet

- Vallance - Sistema Do VolvoDocument15 pagesVallance - Sistema Do VolvoNuno PachecoNo ratings yet

- Organization Structure GuideDocument6 pagesOrganization Structure GuideJobeth BedayoNo ratings yet

- Draft of The English Literature ProjectDocument9 pagesDraft of The English Literature ProjectHarshika Verma100% (1)

- 63db2cf62042802 Budget Eco SurveyDocument125 pages63db2cf62042802 Budget Eco SurveyNehaNo ratings yet

- The Power of Flexibility: - B&P Pusher CentrifugesDocument9 pagesThe Power of Flexibility: - B&P Pusher CentrifugesberkayNo ratings yet

- Department of Education: Republic of The PhilippinesDocument3 pagesDepartment of Education: Republic of The PhilippinesAdonis BesaNo ratings yet

- Camera MatchingDocument10 pagesCamera MatchingcleristonmarquesNo ratings yet

- SHIPPING TERMSDocument1 pageSHIPPING TERMSGung Mayura100% (1)