You might also like

- 61a38d5c7b74a - INcome Tax and ETA HandwrittenDocument15 pages61a38d5c7b74a - INcome Tax and ETA HandwrittenAnuska ThapaNo ratings yet

- Corporate TaxesDocument6 pagesCorporate TaxesfranNo ratings yet

- Fiscal Guide ZambiaDocument9 pagesFiscal Guide ZambiaVenkatesh GorurNo ratings yet

- Tax System in SyngaporeDocument21 pagesTax System in SyngaporeMaria BulgaruNo ratings yet

- Create Act: Corporate Recovery & Tax Incentives For EnterprisesDocument6 pagesCreate Act: Corporate Recovery & Tax Incentives For EnterprisesDanica RamosNo ratings yet

- 3.2 Business Profit TaxDocument49 pages3.2 Business Profit TaxBizu AtnafuNo ratings yet

- International Tax: Bangladesh Highlights 2020Document8 pagesInternational Tax: Bangladesh Highlights 2020Mehadi HasanNo ratings yet

- How Do You See It?: East Africa Quick Tax Guide 2012Document11 pagesHow Do You See It?: East Africa Quick Tax Guide 2012Zimbo KigoNo ratings yet

- India Tax SystemDocument53 pagesIndia Tax SystemNiket DattaniNo ratings yet

- Week 16 and 17 Tax Incentives and BMBEDocument28 pagesWeek 16 and 17 Tax Incentives and BMBEwatanabe200412No ratings yet

- Tax PlanningDocument7 pagesTax PlanningCharan AdharNo ratings yet

- Singapore BudgetDocument35 pagesSingapore Budgetlengyianchua206No ratings yet

- SJMS Associates Budget Highlights 2012Document42 pagesSJMS Associates Budget Highlights 2012Tharindu PereraNo ratings yet

- Percentage TaxDocument4 pagesPercentage TaxPATRICK JAMES BALOGBOG ROSARIONo ratings yet

- A Guide To Taxation in The PhilippinesDocument5 pagesA Guide To Taxation in The PhilippinesNathaniel MartinezNo ratings yet

- Perpajakan SingapurDocument22 pagesPerpajakan SingapurDio PatraNo ratings yet

- Trabaho BillDocument14 pagesTrabaho BillAvia ColorNo ratings yet

- Tax StructureDocument23 pagesTax StructureAsif Rasool ChannaNo ratings yet

- Budget 2016 KPMG PublicationDocument46 pagesBudget 2016 KPMG PublicationsmallvillethetraderNo ratings yet

- Deloitte - A Pocket Guide To Singapore Tax 2014 PDFDocument20 pagesDeloitte - A Pocket Guide To Singapore Tax 2014 PDFAlison YangNo ratings yet

- Tax Reductions Rebates and CreditsDocument15 pagesTax Reductions Rebates and Creditskhans827No ratings yet

- Highlights of The CREATE LawDocument3 pagesHighlights of The CREATE LawChristine Rufher FajotaNo ratings yet

- IFBPDocument11 pagesIFBPmohanraokp2279No ratings yet

- Corporate Recovery and Tax Incentives For EnterprisesDocument5 pagesCorporate Recovery and Tax Incentives For EnterprisesIvy BoseNo ratings yet

- Social Economic ZoneDocument3 pagesSocial Economic ZoneRakesh Raj SinghaniayaNo ratings yet

- Deloitte Tax Pocket Guide 2014Document20 pagesDeloitte Tax Pocket Guide 2014YHNo ratings yet

- Budget Chemistry 2010Document44 pagesBudget Chemistry 2010Aq SalmanNo ratings yet

- Nepal TaxationDocument19 pagesNepal TaxationVijay AgrahariNo ratings yet

- Nigeria Tax Data CardDocument44 pagesNigeria Tax Data CardF KNo ratings yet

- Comparative Analysis of Financial Bills: C C C CCDocument5 pagesComparative Analysis of Financial Bills: C C C CCpdabriwalNo ratings yet

- Ryan RemsDocument56 pagesRyan Remsmimi supasNo ratings yet

- TAX by MamalateoDocument38 pagesTAX by MamalateoTheresa Montales0% (1)

- Net of TaxDocument32 pagesNet of TaxAli GulzarNo ratings yet

- Singapore Tax System and Tax RatesDocument10 pagesSingapore Tax System and Tax RatesshafirasrjNo ratings yet

- Investing in Africa Angola: Page - 1Document9 pagesInvesting in Africa Angola: Page - 1odongochrisNo ratings yet

- Highlights of Budget 2011-2012: Compiled by:-CA. Puneet Duggal (F.C.A) M/S Fatehpuria Duggal & AssociatesDocument14 pagesHighlights of Budget 2011-2012: Compiled by:-CA. Puneet Duggal (F.C.A) M/S Fatehpuria Duggal & AssociatesPuneet DuggalNo ratings yet

- Budget 2009: KIA AssociatesDocument16 pagesBudget 2009: KIA Associatesalmas_sshahidNo ratings yet

- Income Tax AssignmentDocument9 pagesIncome Tax AssignmentPc NgNo ratings yet

- Tax Structure of Pakistan: (A Bird Eye View)Document16 pagesTax Structure of Pakistan: (A Bird Eye View)Kiran AliNo ratings yet

- Corporate Income Taxes and Tax RatesDocument38 pagesCorporate Income Taxes and Tax RatesShaheen ShahNo ratings yet

- Type Rate of Tax: Value-Added Tax (VAT) Donations Tax Unemployment Insurance ContributionsDocument2 pagesType Rate of Tax: Value-Added Tax (VAT) Donations Tax Unemployment Insurance Contributionsdiefenbaker13No ratings yet

- Income Tax - 4 NewDocument42 pagesIncome Tax - 4 Newrehan87100% (2)

- Budget 2012 TPDocument26 pagesBudget 2012 TPVimukthi TwkNo ratings yet

- Budget - Salient Features - 2011!12!28 (1) .02Document3 pagesBudget - Salient Features - 2011!12!28 (1) .02Ruchira SonawaneNo ratings yet

- CE22 - 14 - After Tax Economic AnalysisDocument50 pagesCE22 - 14 - After Tax Economic AnalysisNina MabantaNo ratings yet

- Tax Planning For Year 2010Document24 pagesTax Planning For Year 2010Mehak BhargavaNo ratings yet

- TaxationDocument15 pagesTaxationHani NazrinaNo ratings yet

- Direct Taxation: CA M. Ram Pavan KumarDocument60 pagesDirect Taxation: CA M. Ram Pavan KumarSravyaNo ratings yet

- Tax Assignment 1Document16 pagesTax Assignment 1Tunvir Islam Faisal100% (2)

- Tax Amendment Boolet Final 2020-2021-CompressedDocument40 pagesTax Amendment Boolet Final 2020-2021-CompressedCaesarKamanziNo ratings yet

- Guinea Tax 2Document6 pagesGuinea Tax 2Onur KopanNo ratings yet

- Income Tax AuthoritiesDocument12 pagesIncome Tax Authoritiesroni286No ratings yet

- SJMS Associates Budget Highlights 2014Document50 pagesSJMS Associates Budget Highlights 2014Tharindu PereraNo ratings yet

- Tax Incentives & FDI Policy in Sri LankaDocument16 pagesTax Incentives & FDI Policy in Sri LankaNihmathullah Kalanther LebbeNo ratings yet

- Bangladesh Tax Handbook 2008-2009 PDFDocument53 pagesBangladesh Tax Handbook 2008-2009 PDFNur Md Al HossainNo ratings yet

- Indonesia: in Case of Branches of Foreign Companies, TheDocument2 pagesIndonesia: in Case of Branches of Foreign Companies, TheVioni HanifaNo ratings yet

- Budget Briefing 2015Document63 pagesBudget Briefing 2015Noor AliNo ratings yet

- Operating a Business and Employment in the United Kingdom: Part Three of The Investors' Guide to the United Kingdom 2015/16From EverandOperating a Business and Employment in the United Kingdom: Part Three of The Investors' Guide to the United Kingdom 2015/16No ratings yet

- Entrep q4 All LessonsDocument14 pagesEntrep q4 All LessonsANDREI ESCOTILLONNo ratings yet

- Introduction of Income TaxDocument47 pagesIntroduction of Income TaxVishwamittarNo ratings yet

- Manning Centre Report On Calgary City CouncilDocument41 pagesManning Centre Report On Calgary City CouncilCalgary HeraldNo ratings yet

- Fa Notes 2Document17 pagesFa Notes 2Pooja NNo ratings yet

- Ivan Gyulai Natural Resource Use Management PDFDocument28 pagesIvan Gyulai Natural Resource Use Management PDFatushemeza clinton tcoupNo ratings yet

- 39 - 2007 Income Tax VAT Treatment Security Agencies WithholdingDocument28 pages39 - 2007 Income Tax VAT Treatment Security Agencies WithholdingChristy SanguyuNo ratings yet

- Cambridge O Level: Economics 2281/12Document12 pagesCambridge O Level: Economics 2281/12Jack KowmanNo ratings yet

- Chapter 1 Introduction: Multiple-Choice QuestionsDocument192 pagesChapter 1 Introduction: Multiple-Choice QuestionsSZANo ratings yet

- Sources of Data (2) Purposes of Financial Analysis (For Making Decisions) How To Analyze Financial DataDocument5 pagesSources of Data (2) Purposes of Financial Analysis (For Making Decisions) How To Analyze Financial DataĐinh AnhNo ratings yet

- Philippines, Plaintiff, Versus Quirico Ungab, Accused " and To RestrainDocument5 pagesPhilippines, Plaintiff, Versus Quirico Ungab, Accused " and To RestrainLeBron DurantNo ratings yet

- HMWSSB Godavari Pipe Line ProjectDocument110 pagesHMWSSB Godavari Pipe Line ProjectSasidhar KatariNo ratings yet

- UP vs. City Treasurer of Quezon City, GR No. 214044, 19 Jun 2019Document2 pagesUP vs. City Treasurer of Quezon City, GR No. 214044, 19 Jun 2019Bernalyn Domingo AlcanarNo ratings yet

- In Partial Fulfilment For The Award of The Degree ofDocument15 pagesIn Partial Fulfilment For The Award of The Degree ofnithyaNo ratings yet

- Oregon Urban Renewal HistoryDocument70 pagesOregon Urban Renewal Historyনূরুন্নাহার চাঁদনীNo ratings yet

- Macro Economics Five Years QP NewDocument23 pagesMacro Economics Five Years QP Newprarabdh shivhareNo ratings yet

- Equal Protection ClauseDocument29 pagesEqual Protection ClauseSuiNo ratings yet

- Cost Sheet For 2 BHKDocument1 pageCost Sheet For 2 BHKBharat SharmaNo ratings yet

- 2643 Final Sample MCQDocument17 pages2643 Final Sample MCQDhivyaa ThayalanNo ratings yet

- Spamming FMTDocument14 pagesSpamming FMTJames RudigerNo ratings yet

- Calculate New Salary Tax by Ather SaleemDocument2 pagesCalculate New Salary Tax by Ather SaleemMalikKamranAsifNo ratings yet

- Supply VATDocument25 pagesSupply VATwakemeup143No ratings yet

- CV Anjali AswalDocument2 pagesCV Anjali AswalAditya Sai KumarNo ratings yet

- Problems 1st PartDocument17 pagesProblems 1st PartValentin JallaisNo ratings yet

- 24aaqfr5974c1zw GSTR2B 23122022Document62 pages24aaqfr5974c1zw GSTR2B 23122022DARTENO INDUSTRIESNo ratings yet

- Narrative Report - AdrianDocument8 pagesNarrative Report - AdrianTimpug Crystal JeanNo ratings yet

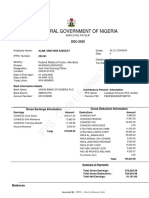

- IPPIS - Oracle E-Business Suite: Federal Government of NigeriaDocument1 pageIPPIS - Oracle E-Business Suite: Federal Government of NigeriaAlimi kehinde100% (1)

- Joint Venture AgreementDocument7 pagesJoint Venture AgreementMarx de Chavez100% (1)

- City of Hamilton Cemeteries Business Plan Strateg - PW15075AppADocument26 pagesCity of Hamilton Cemeteries Business Plan Strateg - PW15075AppAThe Hamilton SpectatorNo ratings yet

- Woodford-Public Debt As Private LiquidityDocument8 pagesWoodford-Public Debt As Private LiquidityjohnNo ratings yet

- Circular Refund 142 11 2020Document3 pagesCircular Refund 142 11 2020Gulrana AlamNo ratings yet