You might also like

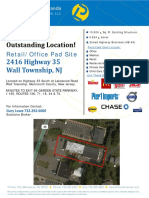

- 2416 Highway 35, Wall Township, NJ Data SheetDocument1 page2416 Highway 35, Wall Township, NJ Data SheetGary LoweNo ratings yet

- 2416 Hwy 35 Wall FlyerDocument1 page2416 Hwy 35 Wall FlyerGary LoweNo ratings yet

- Westwind Professional Plaza FlyerDocument1 pageWestwind Professional Plaza FlyerGary LoweNo ratings yet

- Costar Pricing Indices Point To Consistent Commercial Real Estate Pricing Growth and Improving Investor SentimentDocument9 pagesCostar Pricing Indices Point To Consistent Commercial Real Estate Pricing Growth and Improving Investor SentimentGary LoweNo ratings yet

- 1245 18th Ave FlyerDocument1 page1245 18th Ave FlyerGary LoweNo ratings yet

- Commercial Real Estate Prices Increase A Modest 1.1% in Fourth Quarter As Property Pricing Levels Off in DecemberDocument13 pagesCommercial Real Estate Prices Increase A Modest 1.1% in Fourth Quarter As Property Pricing Levels Off in DecemberGary LoweNo ratings yet

- Investors Go On Offense: A Special Research ReportDocument3 pagesInvestors Go On Offense: A Special Research ReportGary LoweNo ratings yet

- 595 Shrewsbury Ave InformationDocument3 pages595 Shrewsbury Ave InformationGary LoweNo ratings yet

- LPJ Commercial Industrial ListingsDocument1 pageLPJ Commercial Industrial ListingsGary LoweNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Print Preview - Preliminary Application: Project DescriptionDocument21 pagesPrint Preview - Preliminary Application: Project DescriptionRyan SloanNo ratings yet

- Contracts Outline, Bender, 2012-13Document70 pagesContracts Outline, Bender, 2012-13Laura CNo ratings yet

- 05 Acap v. CADocument2 pages05 Acap v. CAkmand_lustregNo ratings yet

- Car Lease AgreementDocument3 pagesCar Lease AgreementthiruNo ratings yet

- Notice To Terminate Tenancy AgreementDocument4 pagesNotice To Terminate Tenancy Agreementbackch9011No ratings yet

- Contractors Manual enDocument21 pagesContractors Manual enkrcdewanewNo ratings yet

- Shirokane Sanko Ancre - ApartmentDocument7 pagesShirokane Sanko Ancre - ApartmentkhannasankalpNo ratings yet

- Lee Nyan Hon & Bros SDN BHD V Metro Charm SDDocument19 pagesLee Nyan Hon & Bros SDN BHD V Metro Charm SDf.dnNo ratings yet

- Tenant Guarantor Form: 1. Tenancy DetailsDocument2 pagesTenant Guarantor Form: 1. Tenancy DetailsthulasiaravindkumarNo ratings yet

- Tamil Nadu Revenue Recovery Act, 1864 PDFDocument37 pagesTamil Nadu Revenue Recovery Act, 1864 PDFLatest Laws TeamNo ratings yet

- Dual Rate Taxed ValuationDocument11 pagesDual Rate Taxed ValuationJigesh MehtaNo ratings yet

- Als Pass 24: Roficiency Ssessment Upplementary HeetDocument2 pagesAls Pass 24: Roficiency Ssessment Upplementary HeetjinxNo ratings yet

- Prop ManDocument27 pagesProp Mansunith raiNo ratings yet

- Contract of Lease - ToDocument4 pagesContract of Lease - ToCelia GaiteNo ratings yet

- Lease Under Transfer of Property ActDocument11 pagesLease Under Transfer of Property Actdivyavishal75% (4)

- 8 The Cost of ProductionDocument2 pages8 The Cost of ProductionDaisy Marie A. RoselNo ratings yet

- Carmona - Contract To Lease - 1st Draft 1 1Document4 pagesCarmona - Contract To Lease - 1st Draft 1 1Jessie GarciaNo ratings yet

- Prem GanapathyDocument7 pagesPrem GanapathyAshwini PrabhakaranNo ratings yet

- Equipment Lease AgreementDocument2 pagesEquipment Lease AgreementmisyeldvNo ratings yet

- Module 6 Leasing (Final)Document74 pagesModule 6 Leasing (Final)Endrit MansakuNo ratings yet

- One To Four Family Residential Contract (Resale) : NOTICE: Not For Use For Condominium TransactionsDocument10 pagesOne To Four Family Residential Contract (Resale) : NOTICE: Not For Use For Condominium TransactionsRobert Glen Murrell JrNo ratings yet

- Space and Society in A Railroad Town: The Making of Renovo, Pennsylvania, 1863-1925.Document159 pagesSpace and Society in A Railroad Town: The Making of Renovo, Pennsylvania, 1863-1925.sbruce2100% (2)

- Week 4 IFRS 16 SlidesDocument19 pagesWeek 4 IFRS 16 SlideskoketsoNo ratings yet

- Financial Aspect of Agrivet Supplies in Lake Sebu, South CotabatoDocument9 pagesFinancial Aspect of Agrivet Supplies in Lake Sebu, South CotabatoNap MissionnaireNo ratings yet

- Total Drilling CostDocument23 pagesTotal Drilling CostDavid SantoNo ratings yet

- Ramvilas Bajaj Vs Ashok Kumar and Anr. On 30 April, 2007Document43 pagesRamvilas Bajaj Vs Ashok Kumar and Anr. On 30 April, 2007hitejoNo ratings yet

- January 2014Document13 pagesJanuary 2014Pumper TraderNo ratings yet

- Contract MAAGAPDocument4 pagesContract MAAGAPRidzsr DharhaidherNo ratings yet

- The Uttar Pradesh Urban Planning and Development ActDocument41 pagesThe Uttar Pradesh Urban Planning and Development ActABHISHNo ratings yet

- Finance SourcesDocument53 pagesFinance Sourcesnira_110100% (2)