You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Tops Bankruptcy DocumentsDocument83 pagesTops Bankruptcy DocumentsAnonymous vhwDL2u100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- BarclaysDocument1 pageBarclaysEtherikal CommanderNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Insurance Agency Business PlanDocument43 pagesInsurance Agency Business PlanJoin Riot100% (5)

- The Longest HatredDocument44 pagesThe Longest HatredRene SchergerNo ratings yet

- Direct Deposit Enrollment Form: The Bancorp Bank 123Document1 pageDirect Deposit Enrollment Form: The Bancorp Bank 123rita ggggggNo ratings yet

- Project Manager Construction Real Estate Development in Los Angeles CA Resume Rey AdalinDocument2 pagesProject Manager Construction Real Estate Development in Los Angeles CA Resume Rey AdalinReyAdalinNo ratings yet

- Luneta Motors CaseDocument4 pagesLuneta Motors CaseErikha AranetaNo ratings yet

- Metropolitan Bank Vs CabilzoDocument10 pagesMetropolitan Bank Vs CabilzoJoey MapaNo ratings yet

- 5-10-2022 Budget Hearing Presentation UpdatedDocument12 pages5-10-2022 Budget Hearing Presentation UpdatedRiverheadLOCALNo ratings yet

- Riverhead Town Proposed Battery Energy Storage CodeDocument10 pagesRiverhead Town Proposed Battery Energy Storage CodeRiverheadLOCALNo ratings yet

- RXR/GGV Qualified & Eligible Documents (Final 09.26.22)Document23 pagesRXR/GGV Qualified & Eligible Documents (Final 09.26.22)RiverheadLOCALNo ratings yet

- Draft Scope Riverhead Logistics CenterDocument20 pagesDraft Scope Riverhead Logistics CenterRiverheadLOCALNo ratings yet

- N.Y. Downtown Revitalization Initiative Round Five GuidebookDocument38 pagesN.Y. Downtown Revitalization Initiative Round Five GuidebookRiverheadLOCALNo ratings yet

- 2022 - 03 - 16 - EPCAL Resolution & Letter AgreementDocument9 pages2022 - 03 - 16 - EPCAL Resolution & Letter AgreementRiverheadLOCALNo ratings yet

- Riverhead Budget Presentation March 22, 2022Document14 pagesRiverhead Budget Presentation March 22, 2022RiverheadLOCALNo ratings yet

- Catherine KentDocument7 pagesCatherine KentRiverheadLOCALNo ratings yet

- Riverhead Town Police Monthly Report July 2021Document6 pagesRiverhead Town Police Monthly Report July 2021RiverheadLOCALNo ratings yet

- Riverhead Comprehensive Plan Update Public Outreach Compendium Feb 16, 2022Document7 pagesRiverhead Comprehensive Plan Update Public Outreach Compendium Feb 16, 2022RiverheadLOCALNo ratings yet

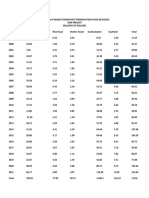

- Peconic Bay Region Community Preservation Fund Revenues 1999-2021Document1 pagePeconic Bay Region Community Preservation Fund Revenues 1999-2021RiverheadLOCALNo ratings yet

- Riverhead Town Board Comprehensive Plan Status Discussion Feb. 17, 2022Document30 pagesRiverhead Town Board Comprehensive Plan Status Discussion Feb. 17, 2022RiverheadLOCALNo ratings yet

- AKRF Public Outreach Report AttachmentsDocument126 pagesAKRF Public Outreach Report AttachmentsRiverheadLOCALNo ratings yet

- Yvette AguiarDocument10 pagesYvette AguiarRiverheadLOCALNo ratings yet

- Pediatric Covid-19 Hospitalization ReportDocument15 pagesPediatric Covid-19 Hospitalization ReportKevin TamponeNo ratings yet

- Robert E. KernDocument3 pagesRobert E. KernRiverheadLOCALNo ratings yet

- Kenneth RothwellDocument5 pagesKenneth RothwellRiverheadLOCALNo ratings yet

- 2021 General Election - Suffolk County Sample Ballot BookletDocument154 pages2021 General Election - Suffolk County Sample Ballot BookletRiverheadLOCALNo ratings yet

- Juan Micieli-MartinezDocument3 pagesJuan Micieli-MartinezRiverheadLOCALNo ratings yet

- Riverhead Town Police Report, March 2021Document6 pagesRiverhead Town Police Report, March 2021RiverheadLOCALNo ratings yet

- League of Women Voters of NYS 2021 Voters Guide: Ballot PropositionsDocument2 pagesLeague of Women Voters of NYS 2021 Voters Guide: Ballot PropositionsRiverheadLOCAL67% (3)

- Evelyn Hobson-Womack Campaign Finance DisclosureDocument3 pagesEvelyn Hobson-Womack Campaign Finance DisclosureRiverheadLOCALNo ratings yet

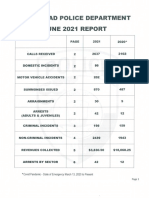

- Riverhead Town Police Monthly Report, June 2021Document6 pagesRiverhead Town Police Monthly Report, June 2021RiverheadLOCALNo ratings yet

- NYSED Health and Safety Guide For The 2021 2022 School YearDocument21 pagesNYSED Health and Safety Guide For The 2021 2022 School YearNewsChannel 9100% (2)

- "The Case of The DIsappering Landfill, or To Mine or Not To Mine" by Carl E. Fritz JR., PEDocument10 pages"The Case of The DIsappering Landfill, or To Mine or Not To Mine" by Carl E. Fritz JR., PERiverheadLOCALNo ratings yet

- Riverhead Town Police Report, August 2021Document6 pagesRiverhead Town Police Report, August 2021RiverheadLOCALNo ratings yet

- Riverhead Town Police Report, January 2021Document6 pagesRiverhead Town Police Report, January 2021RiverheadLOCALNo ratings yet

- Aguiar-Kent Campaign Finance Report 32-Day Pre GeneralDocument2 pagesAguiar-Kent Campaign Finance Report 32-Day Pre GeneralRiverheadLOCALNo ratings yet

- Old Steeple Church Time CapsuleDocument4 pagesOld Steeple Church Time CapsuleRiverheadLOCALNo ratings yet

- Navy Environmental Concerns Survey For CalvertonDocument3 pagesNavy Environmental Concerns Survey For CalvertonRiverheadLOCALNo ratings yet

- Pnadk 970Document64 pagesPnadk 970Kasolo DerrickNo ratings yet

- Al Dhaid Trading & Contracting Al Dhaid Trading ContractingDocument5 pagesAl Dhaid Trading & Contracting Al Dhaid Trading ContractingAbi JithNo ratings yet

- Life Insurance Needs CalculatorDocument6 pagesLife Insurance Needs CalculatorNakkolopNo ratings yet

- Lucknow Unoiversity Syllabus of BBA-302 & BBA-503Document2 pagesLucknow Unoiversity Syllabus of BBA-302 & BBA-503shailesh tandonNo ratings yet

- ASPIRE Home Finance Corp. LTD - PD ReportDocument6 pagesASPIRE Home Finance Corp. LTD - PD Reportsushant1903No ratings yet

- Abstract:: Financial Institutions and Their Role in The Development and Financing of Small Individual ProjectsDocument14 pagesAbstract:: Financial Institutions and Their Role in The Development and Financing of Small Individual ProjectsRamona Georgiana IonițăNo ratings yet

- Al Arafah Islamic BankDocument8 pagesAl Arafah Islamic Bankmd. Piar Ahamed100% (1)

- Internship Report On MCB Bank Limited: Introduction of Banking Industry What Is Bank?Document55 pagesInternship Report On MCB Bank Limited: Introduction of Banking Industry What Is Bank?Muhammad BurhanNo ratings yet

- PDFDocument4 pagesPDFShreya AgrawalNo ratings yet

- Worksheet 2019Document1,366 pagesWorksheet 2019Lex AmarieNo ratings yet

- UntitledDocument10 pagesUntitledHien HaNo ratings yet

- Background of The CompaniesDocument7 pagesBackground of The CompaniesJerhome LunaNo ratings yet

- Response To Comments On Sh. Ashish Gupta MemorandumDocument5 pagesResponse To Comments On Sh. Ashish Gupta MemorandumShaurya SinghNo ratings yet

- Haj Application - 2012 - (Print in Legal Size Only)Document6 pagesHaj Application - 2012 - (Print in Legal Size Only)Loved HerNo ratings yet

- A PresentationDocument6 pagesA Presentationmosa2486No ratings yet

- OpTransactionHistoryTpr17 09 2019 PDFDocument2 pagesOpTransactionHistoryTpr17 09 2019 PDFSonu DangiNo ratings yet

- Corporate Action Processing: What Are The Risks?: Sponsored By: The Depository Trust & Clearing CorporationDocument45 pagesCorporate Action Processing: What Are The Risks?: Sponsored By: The Depository Trust & Clearing CorporationMalcolm MacCollNo ratings yet

- Assignment of Mortgage Assignment OF MortgageDocument4 pagesAssignment of Mortgage Assignment OF MortgageHelpin HandNo ratings yet

- Acca Paper F3 Financial Accounting Mock Exam Prepared By: MR Yeo Hong AnnDocument23 pagesAcca Paper F3 Financial Accounting Mock Exam Prepared By: MR Yeo Hong AnnOrion0088No ratings yet

- "Customer Attitude Towards COMMERCIAL LOANDocument58 pages"Customer Attitude Towards COMMERCIAL LOANPulkit SachdevaNo ratings yet

- Fast Facts Mastercard New Payments Index 2022Document1 pageFast Facts Mastercard New Payments Index 2022jefcheung19No ratings yet

- Synopsis Tittle of The Project: A Study of Rural Banking in A State (Maharashtra)Document4 pagesSynopsis Tittle of The Project: A Study of Rural Banking in A State (Maharashtra)Rohit UbaleNo ratings yet