You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

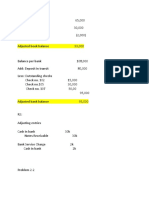

- CalculationDocument3 pagesCalculationShyama SatheesanNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hero MotoCorpDocument10 pagesHero MotoCorpShyama SatheesanNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- BRSDocument10 pagesBRSShyama SatheesanNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hostel ExpensesDocument45 pagesHostel ExpensesShyama SatheesanNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- MCQ Financial Management B Com Sem 5 PDFDocument17 pagesMCQ Financial Management B Com Sem 5 PDFRadhika Bhargava100% (2)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- ch04 SM RankinDocument23 pagesch04 SM RankinSTU DOC100% (2)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Rmo 12 2013 List of Unused Expired Orssiscis Annex D Docxdocx PDF FreeDocument2 pagesRmo 12 2013 List of Unused Expired Orssiscis Annex D Docxdocx PDF FreeShitake Mitsuki100% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- ACCO 101 Partnership Formation For Practice SolvingDocument2 pagesACCO 101 Partnership Formation For Practice SolvingFionna Rei DeGaliciaNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Bank ReconciliationDocument6 pagesBank Reconciliationclarisse jaramillaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Icaew Cfab Pot 2019 SyllabusDocument10 pagesIcaew Cfab Pot 2019 SyllabusAnonymous ulFku1vNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Accountant / Student Resume SampleDocument2 pagesAccountant / Student Resume Sampleresume7.com100% (6)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Zaida Lydia de Choudens v. The Government Development Bank of Puerto Rico, 801 F.2d 5, 1st Cir. (1986)Document8 pagesZaida Lydia de Choudens v. The Government Development Bank of Puerto Rico, 801 F.2d 5, 1st Cir. (1986)Scribd Government DocsNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Illustrative Examples - NCAHFS and Discontinued OperationsDocument2 pagesIllustrative Examples - NCAHFS and Discontinued OperationsMs QuiambaoNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Difference Between Financial and Managerial AccountingDocument1 pageThe Difference Between Financial and Managerial AccountingJonna LynneNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Chapter 25 - Merger & AcquisitionDocument42 pagesChapter 25 - Merger & AcquisitionmeidianizaNo ratings yet

- Uniform Format of Accounts For Central Automnomous BodiesDocument52 pagesUniform Format of Accounts For Central Automnomous Bodiesapk576563No ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Intermediate Accounting Volume 3 ValixDocument4 pagesIntermediate Accounting Volume 3 ValixVyonne Ariane EdiongNo ratings yet

- Accounts - Module 6 Provisions of The Companies Act 1956Document15 pagesAccounts - Module 6 Provisions of The Companies Act 19569986212378No ratings yet

- Cash Flow and Financial Planning: Learning GoalsDocument69 pagesCash Flow and Financial Planning: Learning GoalsJully GonzalesNo ratings yet

- MM-409 1st GURU JAMASWERUNIVERSITYDocument9 pagesMM-409 1st GURU JAMASWERUNIVERSITYvinodNo ratings yet

- Syllabus - Auditing in CIS EnvironmentDocument4 pagesSyllabus - Auditing in CIS Environmentgeee hoonNo ratings yet

- Ac102 ch2Document21 pagesAc102 ch2Fisseha GebruNo ratings yet

- Wakshum FinalDocument37 pagesWakshum FinalAddishiwot GebeyehuNo ratings yet

- Chapter 3: The Basic Accounting Equation and Double Entry SystemDocument3 pagesChapter 3: The Basic Accounting Equation and Double Entry SystemZwelithini MtsamaiNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- ch03 SM Leo 10eDocument72 pagesch03 SM Leo 10ePyae PhyoNo ratings yet

- Cost Accounting Horngren 15th Edition Test BankDocument5 pagesCost Accounting Horngren 15th Edition Test BankGene Mendoza100% (37)

- Chapter 1 - Page 18Document3 pagesChapter 1 - Page 18Ri Fi100% (1)

- Influence of Business Ethics Judgments of Malaysiaa AccountantsDocument16 pagesInfluence of Business Ethics Judgments of Malaysiaa AccountantsCyrilraincreamNo ratings yet

- 11 M 1 MasteryDocument1 page11 M 1 Masteryapi-35875119450% (4)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- IFRS 13 Fair Value Measurement FCPA Dr. James McFie 2017Document59 pagesIFRS 13 Fair Value Measurement FCPA Dr. James McFie 2017Rafik BelkahlaNo ratings yet

- Assignment - SolutionDocument15 pagesAssignment - SolutionWang Hon YuenNo ratings yet

- Midterm Abm 11Document4 pagesMidterm Abm 11Emarilyn BayotNo ratings yet

- Ndokwa Salale Resume - AccountantDocument5 pagesNdokwa Salale Resume - AccountantNdokwaNo ratings yet

- Trial Balance PD Jaya Ban Motor Before AdjusmentDocument1 pageTrial Balance PD Jaya Ban Motor Before AdjusmentHimmalatul Aslami100% (1)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)