You might also like

- How America was Tricked on Tax Policy: Secrets and Undisclosed PracticesFrom EverandHow America was Tricked on Tax Policy: Secrets and Undisclosed PracticesNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Tax TheoriesDocument5 pagesTax TheoriesIsmail Budiono IINo ratings yet

- The New Income Tax Scandal: How the Income Tax Cheats Workers out of Million$ Each Year and the Corrupt Reasons Why This HappensFrom EverandThe New Income Tax Scandal: How the Income Tax Cheats Workers out of Million$ Each Year and the Corrupt Reasons Why This HappensNo ratings yet

- Summary: Flat Tax Revolution: Review and Analysis of Steve Forbes's BookFrom EverandSummary: Flat Tax Revolution: Review and Analysis of Steve Forbes's BookNo ratings yet

- NhlanhlaNeneSpeechTax Indaba2018Document7 pagesNhlanhlaNeneSpeechTax Indaba2018Tiso Blackstar GroupNo ratings yet

- Constructing a Better Tomorrow: A Logical Look to Reform AmericaFrom EverandConstructing a Better Tomorrow: A Logical Look to Reform AmericaNo ratings yet

- Taxes Are Obsolete by Beardsley Ruml, Former FED ChairmanDocument5 pagesTaxes Are Obsolete by Beardsley Ruml, Former FED ChairmanPatrick O'SheaNo ratings yet

- American Tyranny: Our Tax-Apocalypse-Cause for the Fairtax and the Abolishment of the Irs?From EverandAmerican Tyranny: Our Tax-Apocalypse-Cause for the Fairtax and the Abolishment of the Irs?No ratings yet

- Westminster MiGa Neg Kentucky Round 4Document39 pagesWestminster MiGa Neg Kentucky Round 4EmronNo ratings yet

- Jobs, Jobs, Jobs: Follow What's Happening OnDocument4 pagesJobs, Jobs, Jobs: Follow What's Happening OnPAHouseGOPNo ratings yet

- Learning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxFrom EverandLearning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxNo ratings yet

- The Benefit and The Burden: Tax Reform-Why We Need It and What It Will TakeFrom EverandThe Benefit and The Burden: Tax Reform-Why We Need It and What It Will TakeRating: 3.5 out of 5 stars3.5/5 (2)

- PPI - Family Friendly Tax Reform (Weinstein 2005)Document13 pagesPPI - Family Friendly Tax Reform (Weinstein 2005)ppiarchiveNo ratings yet

- The Importance of Taxes To The Government and The EconomyDocument3 pagesThe Importance of Taxes To The Government and The EconomyClarice Kee100% (5)

- Harvest PlanDocument2 pagesHarvest PlanTime Warner Cable NewsNo ratings yet

- “Life” Saving Tax Solutions: Leave Your Legacy to Heirs for Generations to Come …Income-Tax-FreeFrom Everand“Life” Saving Tax Solutions: Leave Your Legacy to Heirs for Generations to Come …Income-Tax-FreeNo ratings yet

- Buque - Prelim Exam-Income TaxationDocument3 pagesBuque - Prelim Exam-Income TaxationVillanueva, Jane G.No ratings yet

- Community Bulletin - April 2013Document9 pagesCommunity Bulletin - April 2013State Senator Liz KruegerNo ratings yet

- Welfare Services Are Actions or Procedures That Cover The Basic Well-Being of The Individuals and TheDocument5 pagesWelfare Services Are Actions or Procedures That Cover The Basic Well-Being of The Individuals and ThekarenepacinaNo ratings yet

- A Real Estate Agent's Guide to Pay Less Tax & Build More WealthFrom EverandA Real Estate Agent's Guide to Pay Less Tax & Build More WealthNo ratings yet

- US Government Economics - Local, State and Federal | How Taxes and Government Spending Work | 4th Grade Children's Government BooksFrom EverandUS Government Economics - Local, State and Federal | How Taxes and Government Spending Work | 4th Grade Children's Government BooksNo ratings yet

- A Primer On National Tax Reform ProposalsDocument2 pagesA Primer On National Tax Reform ProposalsJoshua StokesNo ratings yet

- Constitutional Tax Structure: Why Most Americans Pay Too Much Federal Income TaxFrom EverandConstitutional Tax Structure: Why Most Americans Pay Too Much Federal Income TaxNo ratings yet

- HB 1776, The Property Tax Independence Act: A Solution That Makes Sense For PennsylvaniaDocument6 pagesHB 1776, The Property Tax Independence Act: A Solution That Makes Sense For PennsylvaniaOctorara_ReportNo ratings yet

- Freer Markets Within the Usa: Tax Changes That Make Trade Freer Within the Usa. Phasing-Out Supply-Side Subsidies and Leveling the Playing Field for the Working Person.From EverandFreer Markets Within the Usa: Tax Changes That Make Trade Freer Within the Usa. Phasing-Out Supply-Side Subsidies and Leveling the Playing Field for the Working Person.No ratings yet

- Forming A Policy For Tax Reform: by Thomas H. Spitters, CPADocument5 pagesForming A Policy For Tax Reform: by Thomas H. Spitters, CPAThomas H. SpittersNo ratings yet

- The Problem With Our Tax System and How It Affects UsDocument65 pagesThe Problem With Our Tax System and How It Affects Ussan pedro jailNo ratings yet

- 10 Good ReasonsDocument2 pages10 Good ReasonsApeironNo ratings yet

- Are Taxes EvilDocument5 pagesAre Taxes Evilpokeball0010% (1)

- Fair Taxation: The Starting Point For Fair EconomicsDocument10 pagesFair Taxation: The Starting Point For Fair EconomicsFairnessCoalitionNo ratings yet

- Summary: The Fair Tax Book: Review and Analysis of Neal Boortz and John Linder's BookFrom EverandSummary: The Fair Tax Book: Review and Analysis of Neal Boortz and John Linder's BookNo ratings yet

- Nevada Planning To End Taxation 2014Document5 pagesNevada Planning To End Taxation 2014enerchi1111No ratings yet

- Importance of Tax in EconomyDocument7 pagesImportance of Tax in EconomyAbdul WahabNo ratings yet

- Tax Shifting With BohacDocument6 pagesTax Shifting With BohaclightseekerNo ratings yet

- Behind Tax Policy Controversies: Social, Legal and Economic FoundationsFrom EverandBehind Tax Policy Controversies: Social, Legal and Economic FoundationsNo ratings yet

- The IRS Problem Solver: From Audits to Assessments—How to Solve Your Tax Problems and Keep the IRS Off Your Back ForeverFrom EverandThe IRS Problem Solver: From Audits to Assessments—How to Solve Your Tax Problems and Keep the IRS Off Your Back ForeverRating: 2 out of 5 stars2/5 (1)

- Module 15 Assignment 1Document3 pagesModule 15 Assignment 1Bea De ChavezNo ratings yet

- Dave Hickernell: Dear NeighborDocument4 pagesDave Hickernell: Dear NeighborPAHouseGOPNo ratings yet

- Let's Understand Social Security and Stimulate Investment: Or Separating Economic Voodoo from the TruthFrom EverandLet's Understand Social Security and Stimulate Investment: Or Separating Economic Voodoo from the TruthNo ratings yet

- Tax Inefficiencies and Alternative SolutionsDocument13 pagesTax Inefficiencies and Alternative SolutionsAbdullahNo ratings yet

- Next Level Tax Course: The only book a newbie needs for a foundation of the tax industryFrom EverandNext Level Tax Course: The only book a newbie needs for a foundation of the tax industryNo ratings yet

- Tax Inefficiencies and Alternative SolutionsDocument13 pagesTax Inefficiencies and Alternative SolutionsAbdullahNo ratings yet

- Octorara Administration Office: Thomas L. Newcome II, Ed.DDocument2 pagesOctorara Administration Office: Thomas L. Newcome II, Ed.DOctorara_ReportNo ratings yet

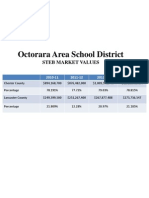

- 2013-14 Budget PResentation II Page 19Document1 page2013-14 Budget PResentation II Page 19Octorara_ReportNo ratings yet

- Octorara Administration Office: Thomas L. Newcome II, Ed.DDocument5 pagesOctorara Administration Office: Thomas L. Newcome II, Ed.DOctorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 16Document1 page2013-14 Budget PResentation II Page 16Octorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 20Document1 page2013-14 Budget PResentation II Page 20Octorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 12Document1 page2013-14 Budget PResentation II Page 12Octorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 14Document1 page2013-14 Budget PResentation II Page 14Octorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 7Document1 page2013-14 Budget PResentation II Page 7Octorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 8Document1 page2013-14 Budget PResentation II Page 8Octorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 18Document1 page2013-14 Budget PResentation II Page 18Octorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 13Document1 page2013-14 Budget PResentation II Page 13Octorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 21Document1 page2013-14 Budget PResentation II Page 21Octorara_ReportNo ratings yet

- Policy 011 11.21.11Document5 pagesPolicy 011 11.21.11Octorara_ReportNo ratings yet

- Ten ReasonsDocument3 pagesTen ReasonsOctorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 5Document1 page2013-14 Budget PResentation II Page 5Octorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 6Document1 page2013-14 Budget PResentation II Page 6Octorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 4Document1 page2013-14 Budget PResentation II Page 4Octorara_ReportNo ratings yet

- Newcome Response0001Document10 pagesNewcome Response0001Octorara_ReportNo ratings yet

- 2013-14 Budget PResentation II Page 3Document1 page2013-14 Budget PResentation II Page 3Octorara_ReportNo ratings yet

- HB 1776, The Property Tax Independence Act: A Solution That Makes Sense For PennsylvaniaDocument6 pagesHB 1776, The Property Tax Independence Act: A Solution That Makes Sense For PennsylvaniaOctorara_ReportNo ratings yet

- Policy 707-App A 11.21.11Document2 pagesPolicy 707-App A 11.21.11Octorara_ReportNo ratings yet

- Policy 707 11.21.11Document9 pagesPolicy 707 11.21.11Octorara_ReportNo ratings yet

- Octorara Area School DistrictDocument4 pagesOctorara Area School DistrictOctorara_ReportNo ratings yet

- Policy 004 11.21.11Document7 pagesPolicy 004 11.21.11Octorara_ReportNo ratings yet

- Policy 008 11.21.11Document1 pagePolicy 008 11.21.11Octorara_ReportNo ratings yet

- Policy 006 11.21.11Document12 pagesPolicy 006 11.21.11Octorara_ReportNo ratings yet

- Policy 007 11.21.11Document3 pagesPolicy 007 11.21.11Octorara_ReportNo ratings yet

- Policy 005 11.21.11Document5 pagesPolicy 005 11.21.11Octorara_ReportNo ratings yet

- Managing Brands GloballyDocument13 pagesManaging Brands GloballySonam SinghNo ratings yet

- ACCT1501 Perdisco 1-3Document20 pagesACCT1501 Perdisco 1-3alwaysyjae86% (7)

- Audit of The Capital Acquisition and Repayment CycleDocument7 pagesAudit of The Capital Acquisition and Repayment Cyclerezkifadila2No ratings yet

- Oz Shy - Industrial Organization: Theory and Applications - Instructor's ManualDocument60 pagesOz Shy - Industrial Organization: Theory and Applications - Instructor's ManualJewggernaut67% (3)

- ECONDocument10 pagesECONChristine Mae MataNo ratings yet

- Illustration: The Following Data Were Reported For 200A Business Activities of Western UniversitiesDocument3 pagesIllustration: The Following Data Were Reported For 200A Business Activities of Western UniversitiesCarlo QuiambaoNo ratings yet

- Book On Making Money, The - Steve OliverezDocument177 pagesBook On Making Money, The - Steve Oliverezpipe_boy100% (1)

- Michael Milakovich - Improving Service Quality in The Global Economy - Achieving High Performance in Public and Private Sectors, Second Edition-Auerbach Publications (2005) PDFDocument427 pagesMichael Milakovich - Improving Service Quality in The Global Economy - Achieving High Performance in Public and Private Sectors, Second Edition-Auerbach Publications (2005) PDFCahaya YustikaNo ratings yet

- S AshfaqDocument45 pagesS AshfaqCMA-1013 V.NAVEENNo ratings yet

- Heritage Tourism: Submitted By, Krishna Dev A.JDocument5 pagesHeritage Tourism: Submitted By, Krishna Dev A.JkdboygeniusNo ratings yet

- REFLECTION PAPER (CAPEJANA VILLAGE) FinalDocument3 pagesREFLECTION PAPER (CAPEJANA VILLAGE) FinalRon Jacob AlmaizNo ratings yet

- CSR STPDocument7 pagesCSR STPRavi Shonam KumarNo ratings yet

- Cost Concept and ApplicationDocument11 pagesCost Concept and ApplicationGilbert TiongNo ratings yet

- Morong Executive Summary 2016Document6 pagesMorong Executive Summary 2016Ed Drexel LizardoNo ratings yet

- Procurement WorkDocument8 pagesProcurement WorkbagumaNo ratings yet

- OM Assignment Sec 2grp 3 Assgn2Document24 pagesOM Assignment Sec 2grp 3 Assgn2mokeNo ratings yet

- Recap: Globalization: Pro-Globalist vs. Anti-Globalist DebateDocument5 pagesRecap: Globalization: Pro-Globalist vs. Anti-Globalist DebateRJ MatilaNo ratings yet

- Project On Ibrahim Fibers LTDDocument53 pagesProject On Ibrahim Fibers LTDumarfaro100% (1)

- Sap TutorialDocument72 pagesSap TutorialSurendra NaiduNo ratings yet

- Statement 08 183 197 8Document6 pagesStatement 08 183 197 8Olwethu NgwanyaNo ratings yet

- INTERESTSDocument15 pagesINTERESTSAnastasia EnriquezNo ratings yet

- (Routledge International Studies in Money and Banking) Dirk H. Ehnts - Modern Monetary Theory and European Macroeconomics-Routledge (2016)Document223 pages(Routledge International Studies in Money and Banking) Dirk H. Ehnts - Modern Monetary Theory and European Macroeconomics-Routledge (2016)Felippe RochaNo ratings yet

- Business Plan Template 2023Document8 pagesBusiness Plan Template 2023Anecita OrocioNo ratings yet

- Independent University of Bangladesh: An Assignment OnDocument18 pagesIndependent University of Bangladesh: An Assignment OnArman Hoque SunnyNo ratings yet

- Case 7Document2 pagesCase 7Manas Kotru100% (1)

- Module Session 10 - CompressedDocument8 pagesModule Session 10 - CompressedKOPERASI KARYAWAN URBAN SEJAHTERA ABADINo ratings yet

- Unemployment ProblemDocument12 pagesUnemployment ProblemMasud SanvirNo ratings yet

- Ahmad FA - Chapter4Document1 pageAhmad FA - Chapter4ahmadfaNo ratings yet

- ch1 BPP Slide f1 ACCADocument95 pagesch1 BPP Slide f1 ACCAIskandar Budiono100% (1)