You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Lacerte - e - File - Returns (Wazhua - Com)Document58 pagesLacerte - e - File - Returns (Wazhua - Com)haiderabbaskhattakNo ratings yet

- 1 PaySlipDocument1 page1 PaySlipUpal RajNo ratings yet

- Evaluation of Import Policy Order 2021-2024Document6 pagesEvaluation of Import Policy Order 2021-2024Mohammad Shahjahan SiddiquiNo ratings yet

- Form 16 PDFDocument3 pagesForm 16 PDFkk_mishaNo ratings yet

- IMF and Reforms in BangladeshDocument4 pagesIMF and Reforms in BangladeshMohammad Shahjahan SiddiquiNo ratings yet

- Evaluation of Bangladesh's Data Protection BillDocument4 pagesEvaluation of Bangladesh's Data Protection BillMohammad Shahjahan SiddiquiNo ratings yet

- How Insiders Are Manipulating Dollar RatesDocument4 pagesHow Insiders Are Manipulating Dollar RatesMohammad Shahjahan SiddiquiNo ratings yet

- About Doing Business' ReportDocument4 pagesAbout Doing Business' ReportMohammad Shahjahan SiddiquiNo ratings yet

- Post Clearance Customs AuditDocument3 pagesPost Clearance Customs AuditMohammad Shahjahan SiddiquiNo ratings yet

- Pandemic Recession and Employment CrisisDocument4 pagesPandemic Recession and Employment CrisisMohammad Shahjahan SiddiquiNo ratings yet

- At Last Asset Management CompanyDocument3 pagesAt Last Asset Management CompanyMohammad Shahjahan SiddiquiNo ratings yet

- The Inflow and Outflow of CapitalDocument4 pagesThe Inflow and Outflow of CapitalMohammad Shahjahan SiddiquiNo ratings yet

- Need For A Payment System ActDocument4 pagesNeed For A Payment System ActMohammad Shahjahan SiddiquiNo ratings yet

- Mutualisation of Public ServicesDocument4 pagesMutualisation of Public ServicesMohammad Shahjahan SiddiquiNo ratings yet

- When Women & Men Will Be EqualDocument3 pagesWhen Women & Men Will Be EqualMohammad Shahjahan SiddiquiNo ratings yet

- Banning Rickshaw Without Alternate Transport!Document4 pagesBanning Rickshaw Without Alternate Transport!Mohammad Shahjahan SiddiquiNo ratings yet

- A. Legal Owner Information: EIN - SSN 578-17-7124Document2 pagesA. Legal Owner Information: EIN - SSN 578-17-7124Trevor AlexanderNo ratings yet

- Annexure To Form 16 Part B (2020)Document3 pagesAnnexure To Form 16 Part B (2020)Dharmendra ParmarNo ratings yet

- P 46Document2 pagesP 46Charlotte JamesNo ratings yet

- EAG 036 Financial Managment Cash Vs Accrual AccountingDocument4 pagesEAG 036 Financial Managment Cash Vs Accrual AccountingMICHAEL USTARENo ratings yet

- Taxation Law - Leonen Case DigestsDocument53 pagesTaxation Law - Leonen Case DigestsInna Franchesca S. VillanuevaNo ratings yet

- IRS Form 4868Document4 pagesIRS Form 4868Anil AletiNo ratings yet

- Sales Tax System in IndiaDocument7 pagesSales Tax System in IndiaKarthi_docNo ratings yet

- Chapter 6. Income From Property v2Document6 pagesChapter 6. Income From Property v2LEARN FROM MENo ratings yet

- Billing Summary Customer Details: Total Amount Due (PKR) : 2,831Document1 pageBilling Summary Customer Details: Total Amount Due (PKR) : 2,831Shazil ShahNo ratings yet

- Fiscal Policy: Expansionary Fiscal Policy When The Government Spend More Then It Receives in Order ToDocument2 pagesFiscal Policy: Expansionary Fiscal Policy When The Government Spend More Then It Receives in Order TominhaxxNo ratings yet

- Instructions For Form CT-1: Department of The TreasuryDocument4 pagesInstructions For Form CT-1: Department of The TreasuryIRSNo ratings yet

- Solved Phyllis Sued Martin S Estate and Won A 65 000 SettlementDocument1 pageSolved Phyllis Sued Martin S Estate and Won A 65 000 SettlementAnbu jaromiaNo ratings yet

- Barrel Quote - 20211110 - 0001Document1 pageBarrel Quote - 20211110 - 0001RAVEENDRA OFFICENo ratings yet

- INA43913Document1 pageINA43913playht791No ratings yet

- Tax I R K FINAL AS AT 20 2 06Document315 pagesTax I R K FINAL AS AT 20 2 06Adarsh. UdayanNo ratings yet

- FabHotels BTGKV 2324 00287 Invoice ZRPFLQDocument2 pagesFabHotels BTGKV 2324 00287 Invoice ZRPFLQMohanGuptaNo ratings yet

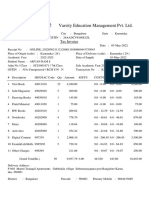

- Period: Salary Statement For Fy-2021-2022 of S.Ragini, (SGT), Id No: 1354755, Mpps KumsaraDocument6 pagesPeriod: Salary Statement For Fy-2021-2022 of S.Ragini, (SGT), Id No: 1354755, Mpps KumsaraNagesh AdumullaNo ratings yet

- 227 Tax AnalysisDocument25 pages227 Tax AnalysisBurton PhillipsNo ratings yet

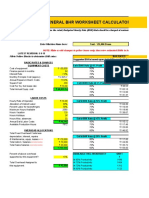

- General BHR Worksheet CalculatorDocument2 pagesGeneral BHR Worksheet CalculatorEmba MadrasNo ratings yet

- Payslip Jan 2023Document1 pagePayslip Jan 2023Palanivelan KamarajNo ratings yet

- BapaDocument12 pagesBapaJeni LagahitNo ratings yet

- Chapter 1: Basic Concepts: Cma Vipul ShahDocument27 pagesChapter 1: Basic Concepts: Cma Vipul ShahsmitaNo ratings yet

- Tax Invoice Trucks and BuyersDocument2 pagesTax Invoice Trucks and BuyersSyam JamiNo ratings yet

- Laxmi Timber 2 BillDocument1 pageLaxmi Timber 2 BillAcma Renu SinghaniaNo ratings yet

- Online 645Document2 pagesOnline 645Aishwarya SenthilNo ratings yet

- Branch Teller: Use SCR 008765 Deposit Fee Collection State Bank CollectDocument1 pageBranch Teller: Use SCR 008765 Deposit Fee Collection State Bank CollectShivani MishraNo ratings yet

- Your Invoice No. RE200143606Document1 pageYour Invoice No. RE200143606Erick MetzNo ratings yet