You might also like

- Basic RiggingDocument156 pagesBasic Riggingkampit100% (18)

- WPS & PQRDocument84 pagesWPS & PQRjoseph.maquez24100% (4)

- The Intelligent REIT Investor: How to Build Wealth with Real Estate Investment TrustsFrom EverandThe Intelligent REIT Investor: How to Build Wealth with Real Estate Investment TrustsRating: 4.5 out of 5 stars4.5/5 (4)

- 6 (1) - NORSOK M601 Welding & Inspection PipingDocument24 pages6 (1) - NORSOK M601 Welding & Inspection PipingAnwar Jbali100% (1)

- N-001 Integrity of Offshore Structures (Rev. 8, September 2012) (30p)Document30 pagesN-001 Integrity of Offshore Structures (Rev. 8, September 2012) (30p)Lee EunseokNo ratings yet

- N-001 Integrity of Offshore Structures (Rev. 8, September 2012) (30p)Document30 pagesN-001 Integrity of Offshore Structures (Rev. 8, September 2012) (30p)Lee EunseokNo ratings yet

- Construction Materials Retail Price Index Primer - 20 PDFDocument2 pagesConstruction Materials Retail Price Index Primer - 20 PDFLevi Leonardo Abayon JuniorNo ratings yet

- US Economic Update - July11Document3 pagesUS Economic Update - July11timurrsNo ratings yet

- 01 - An Overview of Pipeline DesignDocument26 pages01 - An Overview of Pipeline Designkampit100% (1)

- 6.1 Price Inflation: Igcse /O Level EconomicsDocument11 pages6.1 Price Inflation: Igcse /O Level EconomicsAditya GhoshNo ratings yet

- Consumer Price Inflation Detailed Reference TablesDocument518 pagesConsumer Price Inflation Detailed Reference TablesoneoffgmxNo ratings yet

- Bits Drilling GuidelinesDocument8 pagesBits Drilling GuidelinesNeil46100% (2)

- Lloyd's Register Welding Procedure & Welder Qualification Review RP - tcm240-236457 PDFDocument30 pagesLloyd's Register Welding Procedure & Welder Qualification Review RP - tcm240-236457 PDFjos22231No ratings yet

- Asme 16.9Document58 pagesAsme 16.9kampit100% (2)

- (SMA) Strategic Management Analysis of StarbucksDocument24 pages(SMA) Strategic Management Analysis of StarbucksDennison Nanan100% (1)

- DB Breakeven Inflation Swap Guide v1.20101207Document3 pagesDB Breakeven Inflation Swap Guide v1.20101207Palmar SigurdssonNo ratings yet

- CuniDocument32 pagesCunikampit100% (1)

- NORSOK Z-001-Dcoument Content GuideDocument42 pagesNORSOK Z-001-Dcoument Content GuideneracaliNo ratings yet

- Economics AQA A2 Un 4 Workbook AnswersDocument28 pagesEconomics AQA A2 Un 4 Workbook AnswersJEFFREYNo ratings yet

- Offshore HyuNDAIDocument26 pagesOffshore HyuNDAIbetahita_80174No ratings yet

- Country Parks Business PlanDocument38 pagesCountry Parks Business PlangarycwkNo ratings yet

- Economics Group: Weekly Economic & Financial CommentaryDocument9 pagesEconomics Group: Weekly Economic & Financial Commentaryamberyin92No ratings yet

- Deloitte Corporate Finance Retail and Consumer Update q4 2011Document8 pagesDeloitte Corporate Finance Retail and Consumer Update q4 2011KofikoduahNo ratings yet

- HSBC 12072010 Vietnam MonitorDocument16 pagesHSBC 12072010 Vietnam MonitorNguyen Xuan QuangNo ratings yet

- 2011-06-10 LLOY UK Consumer Discretionary Sector AnalysisDocument3 pages2011-06-10 LLOY UK Consumer Discretionary Sector AnalysiskjlaqiNo ratings yet

- Comparing Bricks and Mortar Store Sales With Online Retail Sales August 2018Document11 pagesComparing Bricks and Mortar Store Sales With Online Retail Sales August 2018Alejandro CardonaNo ratings yet

- CBRE Cap Rate Survey August 2011Document30 pagesCBRE Cap Rate Survey August 2011CRE ConsoleNo ratings yet

- April 2010 U.S. Building Market Intelligence Report: Building Stats For The Real Estate Market For This MonthDocument9 pagesApril 2010 U.S. Building Market Intelligence Report: Building Stats For The Real Estate Market For This MonthdbeisnerNo ratings yet

- Housing Market IndexDocument7 pagesHousing Market IndexVijay SwamiNo ratings yet

- UK Economy & Property Market Chart Book September 2009Document13 pagesUK Economy & Property Market Chart Book September 2009ctraderNo ratings yet

- Oecd ReportDocument12 pagesOecd ReportStephen EmersonNo ratings yet

- PWC Valuation Index, 4Q2011, 5th Ed. Focus On Retail SectorDocument8 pagesPWC Valuation Index, 4Q2011, 5th Ed. Focus On Retail SectorkentselveNo ratings yet

- Economic Update Nov201Document12 pagesEconomic Update Nov201admin866No ratings yet

- Commodities-Mostly Up On European Optimism, US DataDocument5 pagesCommodities-Mostly Up On European Optimism, US DataUmesh ShanmugamNo ratings yet

- Q3 Earnings in Line, But See Limited Triggers For Further Market Rerating: Siddhartha KhemkaDocument2 pagesQ3 Earnings in Line, But See Limited Triggers For Further Market Rerating: Siddhartha KhemkaghodababuNo ratings yet

- Pioneer 082013Document6 pagesPioneer 082013alphathesisNo ratings yet

- KoreaDocument2 pagesKoreaDavid4564654No ratings yet

- Market Outlook 16th December 2011Document6 pagesMarket Outlook 16th December 2011Angel BrokingNo ratings yet

- MSR - Monthly Statistics Release - December 2011Document4 pagesMSR - Monthly Statistics Release - December 2011Bertrand FontaneauNo ratings yet

- On Our Minds - : Week AheadDocument28 pagesOn Our Minds - : Week AheadnoneNo ratings yet

- Olympic Glow Hides Economic Gloom: Residential Market UpdateDocument2 pagesOlympic Glow Hides Economic Gloom: Residential Market Updateapi-159978715No ratings yet

- RWC Current IssuesDocument6 pagesRWC Current Issuesdkjity7431No ratings yet

- HsbcpmidecDocument2 pagesHsbcpmidecChrisBeckerNo ratings yet

- Weekly Wrap - Equity 31 Oct 2011 To 04 Nov 2011Document8 pagesWeekly Wrap - Equity 31 Oct 2011 To 04 Nov 2011sumit142No ratings yet

- Are Indias Cities in A Housing BubbleDocument9 pagesAre Indias Cities in A Housing BubbleAshwinBhandurgeNo ratings yet

- Costar Pricing Indices Point To Consistent Commercial Real Estate Pricing Growth and Improving Investor SentimentDocument9 pagesCostar Pricing Indices Point To Consistent Commercial Real Estate Pricing Growth and Improving Investor SentimentGary LoweNo ratings yet

- Monetary PolicyDocument28 pagesMonetary PolicycoetranslationNo ratings yet

- TaiwanDocument2 pagesTaiwanDavid4564654No ratings yet

- 3 Eco Forecast LaymanDocument21 pages3 Eco Forecast LaymanVikas BhatterNo ratings yet

- Investec The BriefDocument8 pagesInvestec The Briefapi-296258777No ratings yet

- Buy-to-Let Index Q1 2014: What A Difference A Year Makes!Document4 pagesBuy-to-Let Index Q1 2014: What A Difference A Year Makes!TheHallPartnershipNo ratings yet

- Eco Project UKDocument16 pagesEco Project UKPankesh SethiNo ratings yet

- Weekly Economic Commentary: Beige Book: Window On Main StreetDocument7 pagesWeekly Economic Commentary: Beige Book: Window On Main Streetapi-136397169No ratings yet

- Weekly Economic Commentar 10-17-11Document4 pagesWeekly Economic Commentar 10-17-11monarchadvisorygroupNo ratings yet

- Strategy Radar - 2012 - 1005 XX Peak CarDocument3 pagesStrategy Radar - 2012 - 1005 XX Peak CarStrategicInnovationNo ratings yet

- Monthly Wholesale Trade: Sales and Inventories, October 2018Document6 pagesMonthly Wholesale Trade: Sales and Inventories, October 2018Ganelotreman LevangeloNo ratings yet

- Make More - Oct 2011Document8 pagesMake More - Oct 2011vidithrt143No ratings yet

- Uk Trade StatisticsDocument7 pagesUk Trade Statisticsapi-53255207No ratings yet

- LuxuryGoodsWorldwideMarketStudy - Spring 2011 UpdateDocument18 pagesLuxuryGoodsWorldwideMarketStudy - Spring 2011 UpdateChristopher WhiteNo ratings yet

- FEL Newsletter October 2009Document4 pagesFEL Newsletter October 2009FirstEquityLtdNo ratings yet

- Van Hoisington Letter, Q3 2011Document5 pagesVan Hoisington Letter, Q3 2011Elliott WaveNo ratings yet

- Spending Slows To A Crawl: Economic InsightsDocument2 pagesSpending Slows To A Crawl: Economic InsightsLauren FrazierNo ratings yet

- PHP C8 EVP2Document8 pagesPHP C8 EVP2fred607No ratings yet

- Morningstar - RobertDocument7 pagesMorningstar - Robertcfasr_programsNo ratings yet

- Welch Retail Trade 2012Document26 pagesWelch Retail Trade 2012WelchOKNo ratings yet

- London Housing Bubble 2014Document2 pagesLondon Housing Bubble 2014harshal7788No ratings yet

- Data Scan: China July Expenditure DataDocument3 pagesData Scan: China July Expenditure Dataapi-162199694No ratings yet

- Carmel Real Estate Sales Market Report For June 2015Document4 pagesCarmel Real Estate Sales Market Report For June 2015Nicole TruszkowskiNo ratings yet

- 1st Tier UK Retail ReportDocument170 pages1st Tier UK Retail Reportjackooo98No ratings yet

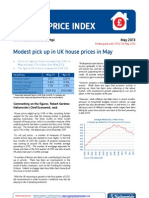

- Modest Pick Up in UK House Prices in MayDocument3 pagesModest Pick Up in UK House Prices in Mayapi-219138607No ratings yet

- London Real Estate MarketDocument16 pagesLondon Real Estate MarketDaniel100% (1)

- BDS - 2010 - CBRE - Toan Canh Thi Truong HA NOI (En) Q2 2010 - 06 07 2010Document28 pagesBDS - 2010 - CBRE - Toan Canh Thi Truong HA NOI (En) Q2 2010 - 06 07 2010ac2000No ratings yet

- Imla The New Normalprospects For 2020 and 2021 1Document25 pagesImla The New Normalprospects For 2020 and 2021 1Aminul IslamNo ratings yet

- February 2011 Index ReportDocument26 pagesFebruary 2011 Index ReportAsouha SougadNo ratings yet

- Carmel Real Estate Sales Market Report For July 2015Document4 pagesCarmel Real Estate Sales Market Report For July 2015Nicole TruszkowskiNo ratings yet

- Key Points: JANUARY 2010 The Outlook For Commercial PropertyDocument7 pagesKey Points: JANUARY 2010 The Outlook For Commercial Propertysekar_smrNo ratings yet

- 3) Current Market InformationDocument6 pages3) Current Market Informationjwingo1No ratings yet

- 2010 0113 EconomicDataDocument11 pages2010 0113 EconomicDataArikKanasNo ratings yet

- CIS100110048293Document4 pagesCIS100110048293B MansbridgeNo ratings yet

- Money - Important in All Economies Because It Is A MeansDocument76 pagesMoney - Important in All Economies Because It Is A MeansDiamondNo ratings yet

- Toiletries 2011Document144 pagesToiletries 2011yash_modi1No ratings yet

- Chelsea Euro Dream Dies at Man United: Champions LeagueDocument28 pagesChelsea Euro Dream Dies at Man United: Champions LeagueCity A.M.No ratings yet

- Tieng Anh Kinh Te - Full Giáo Trình - EditedDocument118 pagesTieng Anh Kinh Te - Full Giáo Trình - Editednguyenphuongnhung887No ratings yet

- Edoc - Pub - Igcse Economics NotesDocument26 pagesEdoc - Pub - Igcse Economics NotesKostas 2No ratings yet

- Macroeconomics Tutorial Answers 1Document3 pagesMacroeconomics Tutorial Answers 1Puja TulsyanNo ratings yet

- Annual Report: National Statistics Office, Malta 2012Document76 pagesAnnual Report: National Statistics Office, Malta 2012tomisnellmanNo ratings yet

- Monetary Policy in Extraordinary Times: SlidesDocument16 pagesMonetary Policy in Extraordinary Times: SlidescreditplumberNo ratings yet

- Chapter 4 - Project Cash Flows NRR Oct2017Document44 pagesChapter 4 - Project Cash Flows NRR Oct2017adib assoliNo ratings yet

- Fuel and Tax Costs 1970 To 2008Document14 pagesFuel and Tax Costs 1970 To 2008Drivers' AllianceNo ratings yet

- 2281 s13 Er PDFDocument14 pages2281 s13 Er PDFatiatmilkyNo ratings yet

- UK Government Guide To GiltsDocument32 pagesUK Government Guide To GiltsFuzzy_Wood_PersonNo ratings yet

- Economics Knowledge Organisers Macroeconomics Year 1Document12 pagesEconomics Knowledge Organisers Macroeconomics Year 1Jhanvi ParekhNo ratings yet

- Destination Unknown Summer 2012 - "For Disabled People The Worst Is Yet To Come"Document110 pagesDestination Unknown Summer 2012 - "For Disabled People The Worst Is Yet To Come"Paul SmithNo ratings yet

- More Than A Minimum: The Final ReportDocument54 pagesMore Than A Minimum: The Final ReportResolutionFoundationNo ratings yet

- Worksheet 4Document4 pagesWorksheet 4JabarrioMykaelHolligan0% (2)

- Macro Revision NotesDocument1 pageMacro Revision NotesThaminah ThassimNo ratings yet

- F2 Past Paper - Question06-2002Document8 pagesF2 Past Paper - Question06-2002ArsalanACCANo ratings yet

- The National Minimum Wage in 2022Document17 pagesThe National Minimum Wage in 2022Amiralitis TassosNo ratings yet

- Cambridge Ordinary LevelDocument12 pagesCambridge Ordinary LevelkazamNo ratings yet

- Chapter 4 - National Income AccountingDocument24 pagesChapter 4 - National Income AccountingChelsea Anne VidalloNo ratings yet