You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Analysis of Financial Performance Ratios for HP, IBM and DELL from 2008-2010Document35 pagesAnalysis of Financial Performance Ratios for HP, IBM and DELL from 2008-2010Husban Ahmed Chowdhury100% (2)

- Factors Creating Health Hazard & Dysfunctional Stress in NSUDocument12 pagesFactors Creating Health Hazard & Dysfunctional Stress in NSUHusban Ahmed ChowdhuryNo ratings yet

- Banglalink Inspire Banglalink Business Banglalink Sme: Post-PaidDocument7 pagesBanglalink Inspire Banglalink Business Banglalink Sme: Post-PaidHusban Ahmed ChowdhuryNo ratings yet

- Ethical Strategy Policy For A RMG CompanyDocument2 pagesEthical Strategy Policy For A RMG CompanyHusban Ahmed ChowdhuryNo ratings yet

- City Bank's comprehensive financing and trade solutionsDocument6 pagesCity Bank's comprehensive financing and trade solutionsHusban Ahmed ChowdhuryNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- GFS CourseDocument2 pagesGFS CoursealiNo ratings yet

- Simple InterestDocument26 pagesSimple InterestVicencia GalbizoNo ratings yet

- Q6682-240312-001Document3 pagesQ6682-240312-001ing.jmatiasNo ratings yet

- Money SupplyDocument15 pagesMoney Supplyhasan jamiNo ratings yet

- Commercial Banks FunctionsDocument14 pagesCommercial Banks FunctionsSudheer Kumar SNo ratings yet

- Audit 2Document6 pagesAudit 2Frances Mikayla EnriquezNo ratings yet

- Construction Tender Notice for Grampanchayat BuildingDocument2 pagesConstruction Tender Notice for Grampanchayat BuildingSD TECHNo ratings yet

- GUINTO - Activity 1 - Loans and Impairment ReceivableDocument4 pagesGUINTO - Activity 1 - Loans and Impairment ReceivableGUINTO, DAN FRANCIS B.No ratings yet

- MD Zulhaidi 1Document1 pageMD Zulhaidi 1limcheeshin94No ratings yet

- Account Statement 010421 310322Document1 pageAccount Statement 010421 310322Suraj choudharyNo ratings yet

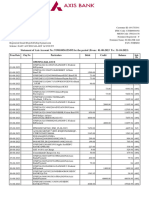

- Statement of Axis Account No:919010056153495 For The Period (From: 01-08-2023 To: 31-10-2023)Document5 pagesStatement of Axis Account No:919010056153495 For The Period (From: 01-08-2023 To: 31-10-2023)pooja.acharyaNo ratings yet

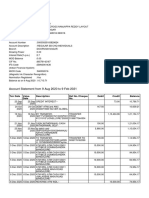

- Account Statement From 9 Aug 2020 To 9 Feb 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument5 pagesAccount Statement From 9 Aug 2020 To 9 Feb 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSuma0% (1)

- International Payment Methods UoSDocument2 pagesInternational Payment Methods UoSJusticeNo ratings yet

- Tajikistan's Leading Microfinance InstitutionDocument24 pagesTajikistan's Leading Microfinance InstitutionTyler DurdenNo ratings yet

- Office of The Adjudicating Officer, Government of Gujarat,: Kop QI MDocument10 pagesOffice of The Adjudicating Officer, Government of Gujarat,: Kop QI MAmrith RajNo ratings yet

- SSC CGL Aao Book by Tej PratapDocument135 pagesSSC CGL Aao Book by Tej Pratapsonumahour2408No ratings yet

- G. H. Bhakta Management Academy: A ON General Study OF at Surat Submitted ToDocument43 pagesG. H. Bhakta Management Academy: A ON General Study OF at Surat Submitted Toayush zadooNo ratings yet

- Kisan Credit CardDocument4 pagesKisan Credit CardBabuNo ratings yet

- List of Executive DirectorDocument5 pagesList of Executive DirectorYogesh ChhaprooNo ratings yet

- Commercial and Cooperative BanksDocument18 pagesCommercial and Cooperative BanksDODONo ratings yet

- Ringkasan Saham-20201120Document64 pagesRingkasan Saham-2020112012gogNo ratings yet

- TraveleenDocument5 pagesTraveleenshahrukhNo ratings yet

- Uplive Basic Policy With Detail NEW August 2022Document4 pagesUplive Basic Policy With Detail NEW August 2022just crizNo ratings yet

- Applying For A Business LoanDocument5 pagesApplying For A Business LoanAhmed AlhaddadNo ratings yet

- Al Kafalah Assignment Ctu 351 PDFDocument16 pagesAl Kafalah Assignment Ctu 351 PDFPiqsamNo ratings yet

- Rundown 2023Document15 pagesRundown 2023Ngurah YukaNo ratings yet

- Unit IV 2 Analytics in Business Support FunctionsDocument14 pagesUnit IV 2 Analytics in Business Support FunctionsKenil DoshiNo ratings yet

- BankCodeExposed 2Document624 pagesBankCodeExposed 2Property Wave100% (6)

- Banking Industry in India Central Bank of India CCDocument57 pagesBanking Industry in India Central Bank of India CCAmit PasiNo ratings yet

- A Proposal On Liquidity Analysis of Nepal Investment Bank Limited (Nibl)Document6 pagesA Proposal On Liquidity Analysis of Nepal Investment Bank Limited (Nibl)Samira ShakyaNo ratings yet