You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- SMC Simplified by TJRTRADESDocument37 pagesSMC Simplified by TJRTRADESmangoz1224No ratings yet

- Southeast Texas EmploymentDocument1 pageSoutheast Texas EmploymentCharlie FoxworthNo ratings yet

- Southeast Texas Economic Update Jan 2012Document4 pagesSoutheast Texas Economic Update Jan 2012Charlie FoxworthNo ratings yet

- Dr. Ted Jones Economic Update Beaumont January 2012Document51 pagesDr. Ted Jones Economic Update Beaumont January 2012Charlie FoxworthNo ratings yet

- Southeast Texas Employment January 2012Document1 pageSoutheast Texas Employment January 2012Charlie FoxworthNo ratings yet

- HowHotAirRises REMAXDocument2 pagesHowHotAirRises REMAXCharlie FoxworthNo ratings yet

- Beaumont Port Arthur MSA Labor Stats November 2011Document1 pageBeaumont Port Arthur MSA Labor Stats November 2011Charlie FoxworthNo ratings yet

- National Economic Trends March 2011 ExternalDocument5 pagesNational Economic Trends March 2011 ExternalCharlie FoxworthNo ratings yet

- May Statistics For Beaumont MLSDocument1 pageMay Statistics For Beaumont MLSCharlie FoxworthNo ratings yet

- The Setx Times: EconomicDocument4 pagesThe Setx Times: EconomicCharlie FoxworthNo ratings yet

- Beaumont/Port Arthur Employment Data For AprilDocument1 pageBeaumont/Port Arthur Employment Data For AprilCharlie FoxworthNo ratings yet

- Employment Beaumont Port Arthur May 2011Document1 pageEmployment Beaumont Port Arthur May 2011Charlie FoxworthNo ratings yet

- Economic Trends December 2010 by Richard Haley From EntergyDocument4 pagesEconomic Trends December 2010 by Richard Haley From EntergyCharlie FoxworthNo ratings yet

- TrackingTxEcon3 11Document2 pagesTrackingTxEcon3 11Charlie FoxworthNo ratings yet

- SETEDF Newsletter 2011.2Document4 pagesSETEDF Newsletter 2011.2Charlie FoxworthNo ratings yet

- Dr. Mark Dotzour Presentation To Beaumont Board of RealtorsDocument21 pagesDr. Mark Dotzour Presentation To Beaumont Board of RealtorsCharlie FoxworthNo ratings yet

- Census Cities in Jefferson CountyDocument78 pagesCensus Cities in Jefferson CountyCharlie FoxworthNo ratings yet

- Southeast Texas January Unemployment ReportDocument1 pageSoutheast Texas January Unemployment ReportCharlie FoxworthNo ratings yet

- Southeast Texas Labor StatisticsDocument1 pageSoutheast Texas Labor StatisticsCharlie FoxworthNo ratings yet

- Economic Trends From Entergy's Richard LynchDocument3 pagesEconomic Trends From Entergy's Richard LynchCharlie FoxworthNo ratings yet

- Southeast Texas Regional Economic ReportDocument5 pagesSoutheast Texas Regional Economic ReportCharlie FoxworthNo ratings yet

- Beaumont Port Arthur Labor StatisticsDocument1 pageBeaumont Port Arthur Labor StatisticsCharlie FoxworthNo ratings yet

- November National Economic Trends Report - by Richard Lynch - From EntergyDocument4 pagesNovember National Economic Trends Report - by Richard Lynch - From EntergyCharlie FoxworthNo ratings yet

- SETEDF Newsletter 2011.1Document4 pagesSETEDF Newsletter 2011.1Charlie FoxworthNo ratings yet

- Cash Budget PracticeDocument4 pagesCash Budget PracticeSavana AndiraNo ratings yet

- D&D 5.0 - Aventura (Nível 7) O Refúgio Perdido Do ArquimagoDocument30 pagesD&D 5.0 - Aventura (Nível 7) O Refúgio Perdido Do ArquimagoMurilo TeixeiraNo ratings yet

- MainstaySuites FF&EDocument77 pagesMainstaySuites FF&ELi WangNo ratings yet

- OLA BillDocument3 pagesOLA BillPradeepNo ratings yet

- Crop and Seed Identification Removal Examination ResultDocument2 pagesCrop and Seed Identification Removal Examination ResultYvonnee LauronNo ratings yet

- Mathematical Economics - Economics Stack ExchangeDocument5 pagesMathematical Economics - Economics Stack ExchangeJoseph JungNo ratings yet

- Cost Accounting Tutorial 8 - PROBLEMDocument3 pagesCost Accounting Tutorial 8 - PROBLEMelgaavNo ratings yet

- NEXO Sliding SleeveDocument3 pagesNEXO Sliding SleevetongsabaiNo ratings yet

- (Advances in Strategic Management) SZULANSKI ET AL - Strategy Process (Advances in Strategic Management Vol. 22) - Emerald Group Publishing Limited (2005)Document553 pages(Advances in Strategic Management) SZULANSKI ET AL - Strategy Process (Advances in Strategic Management Vol. 22) - Emerald Group Publishing Limited (2005)Andra ModreanuNo ratings yet

- holorib en-1.25mm厚铝板参考Document8 pagesholorib en-1.25mm厚铝板参考石银雷No ratings yet

- Penilaian Tengah Semester (PTS) Ganjil: Madrasah Ibtidaiyah Al-Islamiyyah Campurejo Sambit PonorogoDocument9 pagesPenilaian Tengah Semester (PTS) Ganjil: Madrasah Ibtidaiyah Al-Islamiyyah Campurejo Sambit PonorogoJadon SancoNo ratings yet

- Transunion Cibil ReportDocument39 pagesTransunion Cibil ReportSHREYAS KHANOLKARNo ratings yet

- Slope Word Problems: Name: - Class: - Date: - Id: ADocument5 pagesSlope Word Problems: Name: - Class: - Date: - Id: ACece SantosNo ratings yet

- Subject: GEC 8 The Contemporary World Chapter 1: Introduction To Globalization (3 Hours)Document6 pagesSubject: GEC 8 The Contemporary World Chapter 1: Introduction To Globalization (3 Hours)Cj DasallaNo ratings yet

- Transport Geography White H P and Senior M L London Longman 1983Document1 pageTransport Geography White H P and Senior M L London Longman 1983Sorin DinuNo ratings yet

- Professional Abridgement Previous Organizational Highlights: Jindal Naturecure Institute, Bangalore, IndiaDocument3 pagesProfessional Abridgement Previous Organizational Highlights: Jindal Naturecure Institute, Bangalore, IndiaAdditya ChauhanNo ratings yet

- TCS Health Insurance - Contact Matrix - Address For Claim SubmissionDocument2 pagesTCS Health Insurance - Contact Matrix - Address For Claim SubmissionKarthikNo ratings yet

- Profit & Loss - Maruti Suzuki India LTD.: PrintDocument5 pagesProfit & Loss - Maruti Suzuki India LTD.: PrintPushkar VermaNo ratings yet

- Elasticity of DemandDocument6 pagesElasticity of DemandVaibhav MishraNo ratings yet

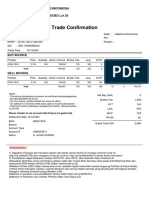

- Trade ConfirmationDocument1 pageTrade ConfirmationHavid KurniaNo ratings yet

- Edited - No Claim BonusDocument1 pageEdited - No Claim BonuslupolupoNo ratings yet

- Application Format For Scheme For Creation/expansion of Food Processing & Preservation CapacitiesDocument3 pagesApplication Format For Scheme For Creation/expansion of Food Processing & Preservation CapacitiesA RahmanNo ratings yet

- Unit 6 - Comparing and Scaling: HW: 2.3 ACEDocument4 pagesUnit 6 - Comparing and Scaling: HW: 2.3 ACEAditya SahuNo ratings yet

- Economics A: Thursday 16 May 2019Document32 pagesEconomics A: Thursday 16 May 2019Afifa At SmartEdgeNo ratings yet

- COSMDocument2 pagesCOSMRuchi Rabuya BaclayonNo ratings yet

- Especificacion Palas (Cucharas para Pala)Document1 pageEspecificacion Palas (Cucharas para Pala)jose chaveroNo ratings yet

- Ahsanullah University of Science and Technology: AssignmentDocument7 pagesAhsanullah University of Science and Technology: AssignmentSudip TalukdarNo ratings yet

- Cost Acc. Final-CollierDocument15 pagesCost Acc. Final-CollierKathya SilvaNo ratings yet

- Data Interpretation - 02 Handout - 1756591Document3 pagesData Interpretation - 02 Handout - 1756591Girish KumarNo ratings yet