Professional Documents

Culture Documents

Industry Report - 1

Uploaded by

api-3702531Original Description:

Copyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Industry Report - 1

Uploaded by

api-3702531Copyright:

Available Formats

MARKET AN ALYSIS

www.idc.com

Worldwide Security Software 2004–2008 Forecast and

2003 Vendor Shares

F.508.935.4015

Brian E. Burke Charles J. Kolodgy

Christian A. Christiansen Sally Hudson

IDC OPINION

P.508.872.8200

Security software spending remains a top priority in many organizations, and the

security software market achieved $8.4 billion in revenue in 2003, representing 17.5%

growth over 2002. IDC currently forecasts this market to reach $16.3 billion in

revenue in 2008, representing a compound annual growth rate (CAGR) of 14%.

Highlights are as follows:

Global Headquarters: 5 Speen Street Framingham, MA 01701 USA

! The growing reliance on IT for corporate operations and increasing government

and industry regulation is elevating security policy, adherence to best practices,

and measurement to a critical component of corporate governance. To meet

these needs, security and vulnerability management (SVM) products are being

released that can assist enterprises in handling policy creation, compliance

measurements and audits, and reporting.

! The costs associated with integrating heterogeneous authentication and

authorization systems have driven demand for a more comprehensive and

integrated identity and access management (IAM) solution that would help to not

only reduce costs, but also increase security and productivity.

! Viruses and worms continue to be the most serious threat facing corporations.

However, new threats like spyware and phishing attacks are quickly moving up

the priority list of corporate security concerns.

! Intrusion detection and prevention (ID&P) technology remains an important

component of an in-depth defense enterprise security program. ID&P products

have been gaining acceptance as a way to eliminate Internet worms and

maintain control over the internal working of enterprise networks and

applications.

! The enterprise software firewall market continues to shrink as more vendors

move to a pure appliance distribution model. As the network perimeter becomes

less defined, corporations will turn to desktop firewalls.

Filing Information: December 2004, IDC #32391, Volume: 1, Tab: Markets

Security Products: Market Analysis

T ABLE OF CONT ENT S

In This Study 1

Executive Summary.................................................................................................................................. 1

Methodology ............................................................................................................................................. 1

Security Software Market Definition.......................................................................................................... 1

S i t u a t i o n O ve r v i e w 5

Key Trends ............................................................................................................................................... 6

Leading Vendors in 2003.......................................................................................................................... 9

Future Outlook 16

Forecast and Assumptions ....................................................................................................................... 16

Essential Guidance 24

Learn More 25

Related Research ..................................................................................................................................... 25

#32391 ©2004 IDC

LIST OF T ABLES

P

1 Worldwide Security Software Revenue by Market, 2003–2008.................................................... 16

2 Worldwide Security Software Revenue by Region, 2003–2008 ................................................... 17

3 Key Forecast Assumptions for the Worldwide Security Software Market, 2004–2008 ................. 17

©2004 IDC #32391

LIST OF FIGURES

P

1 Threats to Enterprise Security...................................................................................................... 5

2 Worldwide Security Software Revenue for Top 10 Vendors, 2003............................................... 9

3 Worldwide Secure Content Management Software Revenue for Top 10 Vendors, 2003............. 10

4 Worldwide Identity and Access Management Software Revenue for Top 10 Vendors, 2003....... 11

5 Worldwide Security and Vulnerability Management Software Revenue for Top 10 Vendors,

2003 ............................................................................................................................................. 12

6 Worldwide Intrusion Detection and Prevention Software Revenue for Top 10 Vendors, 2003..... 13

7 Worldwide Firewall/VPN Software Revenue for Top 10 Vendors, 2003....................................... 14

8 Worldwide Other Security Software Revenue for Top 10 Vendors, 2003..................................... 15

#32391 ©2004 IDC

IN THIS STUDY

Executive Summary

This IDC study examines the worldwide security software market for the period 2003–

2008. Worldwide market sizes and trends are provided for 2003, and a five-year

growth forecast for this market is shown for 2004–2008. Vendor competitive analysis,

with vendor revenues and market shares of the leading vendors, is provided for 2003.

This study also identifies the characteristics that vendors will need to be successful in

the future.

Methodology

Please note the following:

! The information contained in this study was derived from the IDC Software

Market Forecaster database as of July 6, 2004.

! Total software revenue is defined as license revenue plus subscription

maintenance fees plus other software function–related services fees such as the

implicit or stated value of software included in an application service provider's

(ASP's) or other hosted software arrangement.

! IDC's revenue information for companies and software markets is based on

recognized revenue as defined in U.S. practice rather than on bookings. IDC

bases its reporting of, and forecasts for, the software market based on revenue

as defined by GAAP.

! All numbers in this document may not be exact due to rounding.

For more information on IDC's software definitions and methodology, see IDC's

Software Taxonomy, 2004 (IDC #30838, February 2004).

Security Software Market Definition

Secure Content Management

SCM is a market that reflects corporate customers' need for policy-based Internet

management tools that manage Web content, messaging security, virus protection,

and malicious code. SCM is a superset of three specific product areas:

! Antivirus software identifies and/or eliminates harmful software and macros.

Antivirus software scans hard drives, email attachments, floppy disks, Web

pages, and other types of electronic traffic (e.g., instant messaging [IM] and short

message service [SMS]) for any known or potential viruses, malicious code,

trojans, or spyware.

©2004 IDC #32391 1

! Web filtering software is used to screen and exclude from access or availability

Web pages that are deemed objectionable or not business related. Web filtering

is used by corporations to enforce corporate policy as well as by schools and

universities and home computer owners (for parental controls).

! Messaging security software is used to monitor, filter, and/or block messages

from different messaging applications (e.g., email, IM, SMS, and peer to peer)

containing spam, company confidential information, and objectionable content.

Messaging security is also used by certain industries to enforce compliance with

privacy regulations (e.g., HIPAA, Gramm-Leach-Bliley, and SEC) by monitoring

electronic messages for compliance violations. This market also includes secure

(encrypted) email.

Firewall/VPN Software

The firewall/VPN market consists of software that identifies and blocks access to

certain applications and data. These products may also include virtual private network

(VPN) encryption as an option. Software firewalls fall into two distinct categories:

enterprise and desktop. The desktop firewall is itself divided into corporate and

consumer categories. In more detail:

! Enterprise firewall/VPN software is robust enterprise-class software that

inspects IP packets as they enter a network. The inspection is to determine if the

packet conforms to a policy (i.e., an acceptable protocol). The result of the

inspection will be to allow the packet or to reject the packet.

! Desktop firewalls cost less than $100 and are used to determine if a given IP

packet should be passed to the desktop device. Generally, the products are used

to control what desktop applications can communicate with the Internet. They are

also evolving to control the functionality of the Web browser. The desktop firewall

market is divided into those sold to the corporate customer and those sold to

consumers.

! Corporate desktop firewalls are generally used to maintain the corporate

desktop security policy. Many of the corporate desktop firewalls incorporate

remote management and policy. Through the use of a central management

console, enterprises or service providers can manage the firewall to ensure that it

remains within a stated policy, receives software updates, and has virtual private

network management. Revenue in this market includes any management servers

used to serve the corporate policy.

! Consumer desktop firewalls are generally used to protect home and small

business offices that have a high-speed, always-on connection through a cable

or DSL modem. These products have the same technology as those of the

corporate desktop firewall, but remote management of these products is not

possible.

2 #32391 ©2004 IDC

Intrusion Detection and Prevention Software

! Intrusion detection products provide continuous monitoring of devices or

networks and react to malicious activity. A device or agent on a network or a

system, respectively, will compare current activity with a list of signatures known

to represent malicious activity, or it will use other detection methods such as

protocol analysis, anomaly, behavioral, or heuristics to discover unauthorized

network activity. Intrusion detection products are passive systems that do not

interact directly with the datastream or application calls. They can direct other

security products such as firewalls to activate a preestablished automated

response to policy-violating activities.

! Intrusion prevention is a subset of intrusion detection because you must be

able to detect before you can prevent. Prevention products perform the same

tasks as detection products; however, to qualify as a prevention product, they

must be inline (have direct access to traffic and commands) and have the ability

to proactively prohibit malicious activity. Although prevention products are

considerably different in function than pure intrusion detection, the two categories

are being tracked together because they compete for the same budget.

Security and Vulnerability Management Software

(SVM) is a comprehensive set of solutions that includes the following:

! Security information and event management (SIM/SEM): Security event

management collects and correlates events, and security information

management adds security intelligence to the mix, provides proactive alerts, and

suggests fixes. Vendors in this market include Computer Associates, NetIQ, IBM,

netForensics, ArcSight, Symantec, eSecurity, Network Intelligence, OpenService,

Intellitactics, and Guardednet.

! Patch and remediation management (PRM): PRM solutions automate or

semiautomate the process of discovering systems on the network, identifying

missing patches and installing those patches across the enterprise immediately

or on a scheduled basis. Vendors in this market include Patchlink, Shavlik, St.

Bernard Software, Computer Associates, NetIQ, Microsoft, and Citadel Security.

! Policy and compliance management (PCM): Policy and compliance products

are designed to allow organizations to quickly create, assess, update, and, in

some cases, enforce security policy. PCM products generally provide best

practices and regulation templates to help create and measure policy for

compliance. Vendors in this market include IBM, NetIQ, Consul Risk

Management, BindView, Citadel Security Software, Intellitactics, Meta Security

Group, Preventsys, Polivec, Pedestal Software, and Securify.

! Security systems and configuration management: Security systems and

configuration management products are established products that contain

security elements and include vendors such as HP OpenView, Computer

Associates (Unicenter), IBM/Tivoli, BMC Software, Evidian, VeriSign, Cisco,

Ubizen, Utimaco, Sun Microsystems, Enterasys, Candle, and MicroMuse. These

©2004 IDC #32391 3

security solutions have traditionally dominated the security management market

by leveraging the strength of their network and system management products

into this area.

! Network forensics: Network forensics solutions capture real-time network data

and identify how business assets are affected by network exploits, internal data

theft, and security or HR policy violations. Vendors in this market include

Guidance Software, Computer Associates, and Network Intelligence.

! Vulnerability assessment: Vulnerability assessment products are batch-level

products that determine the configuration, structure, security attributes, network

user accounts, directories, servers, workstations, and other devices. This

information is compared with a database of known security holes and best

practices for security configuration management. More sophisticated vulnerability

assessment products can test for both known and unknown vulnerabilities by

looking at both the common Web vulnerabilities and application-specific

vulnerabilities of those defects that exist in the actual business logic of the site.

! Vulnerability management: Vulnerability management products expand upon

vulnerability scanning by integrating additional features to provide risk

management and policy compliance. The additional features often integrate

security policy creation, maintenance, and enforcement. Vulnerability

management solutions also assist in patching activities, provide data to other

security devices, and provide detailed audit reports for compliance with

government regulations.

Identity and Access Management

Identity and access management software is a comprehensive set of solutions used

to identify users in a system (employees, customers, contractors, etc.) and control

their access to resources within that system by associating user rights and restrictions

with the established identity.

Web SSO, host SSO, user provisioning, advanced authentication, legacy

authorization, public key infrastructure (PKI), and directory services are all critical

components of identity and access management.

Other Security Software

Other security software covers emerging security functions that do not fit well into an

existing category. It also covers some of the underlying functions, such as encryption

tools and algorithms, that are the basis for many security capabilities found in other

software and hardware products. Also included in this category will be products that fit

a specific need but have yet to become established in the marketplace.

Products in this category will grow into their own categories or eventually be

incorporated into the other market segments. For 2003, areas covered by other

security software include, but are not restricted to, encryption toolkits, file encryption

products, database security, storage security, standalone VPN and VPN clients,

wireless security, Web services security, and secure operating systems. In addition,

4 #32391 ©2004 IDC

readers should be aware that the products that are covered here (especially for

wireless and Web services) are only those that do not qualify for one of the more

established categories.

SITUATION OVERVIEW

Viruses and worms continue to be the most serious threat facing corporations today.

According to a 2004 IDC survey of 600 firms across North America, 31% of

respondents indicated that viruses, trojans, and malicious code were the single

greatest threat, and another 10% indicated that network worms were the greatest

threat, as shown in Figure 1. The interesting finding in the study was that spyware

ranked fourth on the list of single greatest threats in 2004. This clearly shows that

spyware is moving up the priority list of corporate security concerns.

FIGURE 1

Threats to Enterprise Security

Trojans, viruses, and other

malicious code

Employee error (unintentional)

Internet worms

Spyware

Hackers

Sabotage by current employee

or business partner

Application vulnerabilities

Spam

Cyberterrorism

Inability to meet government

regulatory mandates

Other

0 5 10 15 20 25 30 35

(% of respondents)

n = 606

Source: IDC, 2004

©2004 IDC #32391 5

Key Trends

Security and Vulnerability Management Market Trends

IDC believes there were several key factors that drove the need for more

comprehensive security and vulnerability management solutions, not the least of

which are improved security and lower administration costs. Integration of security

with current system and network management systems, assurance of high uptime for

network and applications, administrative cost reduction (help desk), and a singular

view of the IT environment were all key factors in the convergence of security and

vulnerability management solutions.

The problem of coordinating and managing multiple security technologies across the

enterprise is a major obstacle facing organizations today. A growing number of

security products across the enterprise require frequent upgrades and

reconfigurations as new threats and vulnerabilities are detected. The time and costs

associated with coordinating and managing the updates and upgrades for the various

security technologies are overwhelming IS departments and corporate executives

alike. In the past, organizations commonly standardized on a "short list" of best-of-

breed antivirus, firewall, VPN, vulnerability assessment, and intrusion detection

technologies. Since the best-of-breed products often came from different vendors, the

technologies worked independently of one another and each technology had its own

individual management console. As security technologies became more complex,

manageability of large networks that integrated a variety of point products became

significantly more difficult and more costly.

Today's ebusiness world requires fully integrated and more comprehensive security

management solutions to deal with the multiple security products implemented across

the enterprise. Consolidated consoles for managing various security solutions along

with aggregated reporting, analysis, and control functions can reduce IT

administration chores and costs as well as personnel costs.

Identity and Access Management Market Trends

In the past, the mix of in-house, open source, and partner software was presented to

customers as 3A, but these disparate products had little affinity for one another. As a

result, system integration costs were very high. Customers soon began to demand a

more comprehensive set of solutions to not just reduce costs, but also increase

security and productivity. Three or four years ago, systems integration (SI) costs for

3A solutions were a multiple of the initial purchase price of the license and annual

software support contract. In fact, this SI multiple often reached 7–10x the purchase

price of the software. Over the last year, customers pushed vendors for greater

integration within their own products and their partners. As a result, IDC saw the shift

toward IAM solutions and the SI multiples fall to 3–5x in large corporate

environments. In small and medium-sized businesses (SMBs), however, customers

will only tolerate a 1.5x multiple because they worry about their reseller's ability to

6 #32391 ©2004 IDC

handle large integration projects and they lack budget for this kind of work. Overall,

customers increasingly demanded a high level of integration right out of the box. This

drove 3A vendors to develop more integrated IAM solutions.

IDC expects to see more and more hardware in the identity management area.

Tokens, smart cards, and biometrics, to a lesser extent, will become parts of

comprehensive identity and access management solutions.

Secure Content Management Market Trends

Spyware is the newest pest wreaking havoc of corporate and consumer users alike.

Spyware is no longer just a consumer nuisance; it is quickly becoming a major

concern in the corporate environment. The fact that spyware can gather information

about an employee or organization without their knowledge is causing corporate

security departments to take notice. Spyware is often installed without the user's

consent, as a drive-by download, or as the result of clicking some option in a

deceptive pop-up window. What concerns corporate security departments is that

spyware can also be used to monitor keystrokes, scan files, install additional

spyware, reconfigure Web browsers, and snoop email and other applications. Some

of the more sophisticated spyware can even capture screenshots or turn on

Webcams.

The challenge of controlling electronic communications as they flow into and out of an

organization is becoming increasingly more critical. Government and industry

regulations such as HIPAA, Sarbanes-Oxley, Gramm-Leach-Bliley, and SEC have

placed unprecedented pressure on corporations to secure the use of their electronic

communications. Each of these regulations can carry criminal penalties and/or civil

penalties.

The convenience and efficiency of electronic mail has been dramatically reduced by

the extremely rapid growth in the volume of unsolicited commercial electronic mail.

Spam has become more than just a nuisance; it is quickly becoming both a major

productivity drain and potential legal liability in organizations across the globe. Spam

fills networks, servers and inboxes with unwanted and often offensive content. The

business impact of spam only grows more serious as the volume of spam continues

to rise. The volume of spam sent worldwide every day will jump from 7 billion in 2002

to 23 billion in 2004, according to IDC estimates.

Firewall/VPN Market Trends

Software firewall/VPN products have considerable challenges brought on by the

popularity of appliances and new infrastructures and technologies. The market will

need to transform to remain a central part of an enterprise security posture. There are

two directions, caused by the segmentation of the market, that the firewall market will

take.

The first is that enterprise firewall/VPN software will gradually become part of a threat

management security market. This market will incorporate the firewall/VPN software,

along with firewall/VPN security appliances, and intrusion detection and prevention.

This is already happening in that all enterprise-level firewalls (both software and

hardware) are incorporating more sophisticated intrusion and worm protection

©2004 IDC #32391 7

capabilities. The creation of a threat management market will allow security vendors

more opportunity to develop the products that best support enterprise network

security needs. The second major impact is that desktop firewalls are also more

involved in threat management. The desktop products are becoming complete

endpoint security solutions that incorporate intrusion prevention (especially at the

application layer), worm protection, and being tied to antivirus and other content

security capabilities.

Intrusion Detection and Prevention Market Trends

The ID&P market is slowly making a transition from pure detection to prevention. As

IDC has stated, the technologies are complementary — prevention requires

detection. What is happening is the technology is advancing to the point that

customers are more comfortable using the prevention capabilities of the products.

Host intrusion prevention has been successful because its use does not shut down a

network. However, network intrusion prevention is increasing in acceptance as false

alerts are reduced and attacks become more damaging. IDC research estimates that

about 80% of those purchasing intrusion prevention–capable products are using

some of the blocking features in the product. Only a fraction (about a third) of the total

prevention features are being used at this time, but as confidence levels grow, so

should the level of prevention enabled. Vendors are not missing this adoption curve.

Many vendors are releasing prevention within their detection products. In this way a

customer can purchase a product for detection now and eventually and gradually

institute prevention.

To increase ID&P performance and manageability, vendors and customers are

turning to appliance-based network ID&P products. IDC expects that the usage of

dedicated appliances will dwarf the software-only market. The software will probably

only be that delivered to appliance vendors under an OEM arrangement.

8 #32391 ©2004 IDC

Leading Vendors in 2003

Figure 2 shows the top 10 vendors in the security software market for 2003.

FIGURE 2

Worldwide Security Software Revenue for Top 10 Vendors, 2003

Symantec

McAfee

Computer

Associates

Check Point

Software

Trend Micro

IBM

VeriSign

Internet Security

Systems

Microsoft

RSA Security

0 200 400 600 800 1,000 1,200 1,400 1,600

($M)

Secure content management

Firewall/VPN

Intrustion detection and prevention

Identity and access management

Security and vulnerability management

Other

Source: IDC, 2004

©2004 IDC #32391 9

Secure Content Management Software

Figure 3 shows vendor market shares in the secure content management software

market for 2003.

FIGURE 3

Worldwide Secure Content Management Software Revenue for

Top 10 Vendors, 2003

Symantec

McAfee

Trend Micro

Sophos

Websense

SurfControl

Computer Associates

Panda Software

Sybari Software

F-Secure

0 200 400 600 800 1,000 1,200

($M)

Source: IDC, 2004

10 #32391 ©2004 IDC

Identity and Access Management Software

Figure 4 shows vendor market shares in the identity and access management

software market for 2003.

FIGURE 4

Worldwide Identity and Access Management Software Revenue

for Top 10 Vendors, 2003

Computer Associates

IBM

VeriSign

RSA Security

Netegrity

Entrust

Novell

Fujitsu

Hitachi

AOL

0 50 100 150 200 250 300 350

($M)

Source: IDC, 2004

©2004 IDC #32391 11

Security and Vulnerability Management Software

Figure 5 shows vendor market shares in the security and vulnerability management

software market for 2003.

FIGURE 5

Worldwide Security and Vulnerability Management Software

Revenue for Top 10 Vendors, 2003

Computer Associates

Symantec

NetIQ

HP

BindView

Internet Security Systems

Cisco Systems

Enterasys Networks

Ubizen

Evidian (Groupe Bull)

0 20 40 60 80 100

($M)

Source: IDC, 2004

12 #32391 ©2004 IDC

Intrusion Detection and Prevention Software

Figure 6 shows vendor market shares in the intrusion detection and prevention

software market for 2003.

FIGURE 6

Worldwide Intrusion Detection and Prevention Software

Revenue for Top 10 Vendors, 2003

Internet Security Systems

Symantec

Tripwire

Cisco

Ubizen

Computer Associates

NFR

Secos

Enterasys Networks

AirDefense

0 20 40 60 80 100 120

($M)

Source: IDC, 2004

©2004 IDC #32391 13

Firewall/VPN Software

Figure 7 shows vendor market shares in the firewall/VPN software market for 2003.

FIGURE 7

Worldwide Firewall/VPN Software Revenue for Top 10 Vendors,

2003

Check Point Software

Microsoft

Symantec

ZoneLabs (acquired by Check Point)

Novell

Internet Security Systems

Secure Computing

Sun Microsystems

Sygate Technologies

StoneSoft

0 100 200 300 400 500

($M)

Source: IDC, 2004

14 #32391 ©2004 IDC

Other Security Software

Figure 8 shows vendor market shares in the "other" security software market for

2003.

FIGURE 8

Worldwide Other Security Software Revenue for Top 10

Vendors, 2003

Certicom

RSA Security

Hitachi

Network Associates

F-Secure

Fujitsu

Finsiel

SSH Communications Security

Oullim Information Technology

Gemplus International

0 5 10 15 20 25 30 35

($M)

Source: IDC, 2004

©2004 IDC #32391 15

FUTURE OUTLOOK

Forecast and Assumptions

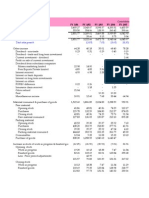

The worldwide security software market achieved $8.4 billion in revenue in 2003, a

17.5% growth over 2002. IDC currently forecasts the security software market to

reach $16.3 billion in revenue in 2008, representing a compound annual growth rate

(CAGR) of 14% (see Tables 1 and 2). Key forecast assumptions for the security

software market are shown in Table 3.

T ABLE 1

Worldwide Security Software Revenue by Market, 2003–2008 ($M)

2003 2008

Share 2003–2008 Share

2003 2004 2005 2006 2007 2008 (%) CAGR (%) (%)

Secure content 3,427 4,206 4,994 5,815 6,665 7,477 40.6 16.9 46.0

management

Identity and access 2,213 2,408 2,642 2,904 3,195 3,508 26.2 9.7 21.6

management

Security and 1,210 1,489 1,809 2,176 2,593 3,043 14.3 20.3 18.7

vulnerability

management

Intrusion detection 366 374 381 391 402 416 4.3 2.6 2.6

and prevention

Firewall/VPN 912 982 1,041 1,098 1,153 1,203 10.8 5.7 7.4

Other 307 354 412 476 548 623 3.6 15.2 3.8

Total 8,435 9,813 11,279 12,860 14,555 16,270 100.0 14.0 100.0

Note: See Table 3 for key forecast assumptions.

Source: IDC, 2004

16 #32391 ©2004 IDC

T ABLE 2

Worldwide Security Software Revenue by Region, 2003–2008 ($M)

2003 2008

Share 2003–2008 Share

2003 2004 2005 2006 2007 2008 (%) CAGR (%) (%)

North America 4,133 4,790 5,478 6,180 6,898 7,614 49.0 13.0 46.8

Western Europe 2,556 2,983 3,446 3,980 4,585 5,206 30.3 15.3 32.0

Asia/Pacific 1,324 1,548 1,787 2,049 2,333 2,619 15.7 14.6 16.1

ROW 422 493 568 651 739 830 5.0 14.5 5.1

Worldwide 8,435 9,813 11,279 12,860 14,555 16,270 100.0 14.0 100.0

Note: See Table 3 for key forecast assumptions.

Source: IDC, 2004

T ABLE 3

Key Forecast Assumptions for the Worldwide Security Software Market,

2004–2008

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

Macroeconomics

Economy Worldwide economic growth Moderate. Economic growth

will continue to recover slowly will begin to have a positive

↑

from 2001 levels to traditional impact on IT spending.

levels, which will be slightly

####$

below those in Consensus

Economics' April 4 forecast.

Policy Alan Greenspan is saying that Moderate. The deficit and

the deficit may be dangerous, rising interest rates could result

hinting that interest rates may in net-new IT spending if

rise. It is possible that the real

estate bubble will burst.

compliance projects don't

displace other IT projects on a

↓ ####$

Healthcare costs will continue 1:1 basis.

to rise.

Profits Pretax profits will be more than Moderate. IT spending will

↑

10% in the United States. begin to increase as individual

Consensus Economics' April 4 company profits improve.

####$

forecast will hold.

©2004 IDC #32391 17

T ABLE 3

Key Forecast Assumptions for the Worldwide Security Software Market,

2004–2008

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

Iraq The war in Iraq will continue, Low. Economic uncertainty

with Saddam Hussein deposed over Iraq will impact IT

and discredited. Travel spending.

restrictions will be lifted, and

the aura of uncertainty affecting

business decisions will

↓ ###$$

dissipate. The war is still being

financed with U.S. government

debt.

Post-Iraq There will be no Iraq-like war Low. There will be no impact.

and no abnormal activity one

way or the other.

↔ ###$$

Contagion There are no major contagions Low. The impact of any

on the immediate horizon. outbreaks will likely be limited

to small local areas. The

exception could be the

discovery of substantial mad

↔ ####$

cow disease in the United

States.

Other geopolitics The threat of terrorism at home Moderate. Business decisions

↔

and other potential armed and project initiation will begin

political conflict will neither in line with a better economic

###$$

escalate nor abate. outlook.

U.S. elections U.S. elections are a wild card Moderate. Traditionally,

↔

for the forecast period in the election years have been good

short term. for the economy; the issue will

####$

be what happens in 2005.

Energy Oil prices are on the rise. High. Oil prices are less

predictable, which is not so ↓ ####$

good for business.

18 #32391 ©2004 IDC

T ABLE 3

Key Forecast Assumptions for the Worldwide Security Software Market,

2004–2008

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

Inflation Inflation will remain under Moderate. Business

control. Over the next three confidence will be unaffected.

years (according to Consensus

Economics), expectations for

the United States, Western

↔

Europe, and Asia/Pacific are

that consumer prices will rise

####$

by less than 2%. Eastern

Europe and Latin America,

however, will continue to see

double-digit inflation. There will

be no deflation.

Unemployment Unemployment will slowly tail Moderate. More employment

off but remain above 5% in the will drive more need for IT

United States and flat in infrastructure and is a lagging

↑

Europe. There will not be a lot indicator of an economic

of job creation in the United recovery; job creation should

###$$

States. be accompanied by a

willingness to invest in other

areas.

↔

Telecom The telecom industry will begin Low. The IT industry has

to recover. already factored this in.

####$

Government and Government budget deficits Moderate. The strengthening

trade and trade imbalances will of the dollar may help U.S.

remain neutral in their impact software companies somewhat.

on IT. The dollar may

↔

strengthen somewhat. The

mood of Europe toward the

###$$

United States is a concern;

anger over the war in Iraq may

create an informal

protectionism.

Scandals The Enron, WorldCom, Tyco, Low. There will be no change.

and Parmalat scandals will

recede into memory, and ↔ ####$

business and consumer

confidence will begin to return.

©2004 IDC #32391 19

T ABLE 3

Key Forecast Assumptions for the Worldwide Security Software Market,

2004–2008

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

Exchange rates Improved profits in the United Moderate. This may accelerate

States, with the possibility of IT exports from exporting

interest rates going up, may countries into the United

↔

strengthen the U.S. dollar States.

somewhat. Top IT vendors'

###$$

growth will be attributable

mainly to the decline in the

dollar.

Expansion of the Increases will need to manage Low. There will be a balance of

eurozone business automation and spending, with jobs/production

↔

integration. moving to Eastern Europe

(shutting down of some existing

####$

systems), freeing up alternative

IT spending in Western Europe.

Compliance With regulations such as Moderate. Compliance

Sarbanes-Oxley, Basel II, and regulations may begin to have

HIPAA, increased compliance an effect on software spending

legislation within the United in 2005 and beyond.

States and Western Europe will Compliance will affect areas of

↑

increase transparency in many infrastructure software and

industries. services such as security and

####$

storage and applications areas

such as records management,

content management, and

business performance

management (to name a few).

Technology/

service

developments

Software Years of add-on and point-to- Moderate. The complexity

complexity point integration strategies crisis will maintain the need for

have resulted in an overly integration, but the demand for

complex infrastructure. high quality and productivity

Demand for simplicity and

agility will require a focus on

could deter skeptical buyers

from existing product offerings.

↔ ####$

business process as opposed Increasingly, this functionality

to technology itself. may be delivered as an IT or

business service.

20 #32391 ©2004 IDC

T ABLE 3

Key Forecast Assumptions for the Worldwide Security Software Market,

2004–2008

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

Linux Technical IT users will lead Low. This will have a

application deployment, with downward impact on price

↔

homegrown applications pressures.

moving first. Mainstream

####$

software is also moving toward

application serving on Linux.

Mobility Application and user-focused Low. This will have a low

mobile deployments are now impact on overall software

addressing business needs, growth.

which are being driven by line

of business. The need for more

↑ ####$

devices with useful applications

will continue.

Utility computing Multinational vendors will Low. This will have a low near-

continue to drive the concept of term impact on software

utility computing in various revenue. Software spending ↑ ##$$$

forms, but the concept is not may pick up toward the end of

well defined in the marketplace. the forecast period.

Killer apps New technology (e.g., Web Moderate. No killer apps or

services, wireless LANs, new technologies will come to

storage area networks, drive overall industry growth in

clustering, and high-growth the same way Windows and

↔

software areas) will help drive Office suites did in the 1980s or

price performance to attractive the Internet did in the late

####$

levels that support new IT 1990s. Web services will

spending growth. continue to be mostly a

software development

technique.

Labor supply

Productivity Job creation in the United Moderate. This will impact

management States and Europe will not be

prevalent.

increasing software revenue

growth.

↑ ###$$

Offshoring Skill supplies will be fulfilled Low. This will have little impact

with offshore software on overall software growth. The

↔

development. Developer jobs job market and pricing pressure

will not be returning to the are already major factors in

####$

United States or Western Western Europe.

Europe.

©2004 IDC #32391 21

T ABLE 3

Key Forecast Assumptions for the Worldwide Security Software Market,

2004–2008

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

Capitalization

Venture Venture funding will begin to Low. Money will continue to

pick up, but funding amounts open up. ↑ ####$

will be smaller.

Stocks There will be a modest upward Moderate. This will create

trend worldwide, but the U.S. decreased business confidence

↓

stock market may be in the United States.

overpriced and may go down,

##$$$

causing some small increases

in inflation in the United States.

Market

characteristics

Large enterprise There will be extreme price Moderate. This will have an

software renewals pressure on large enterprise

software renewals.

impact on changing software

revenue growth.

↓ ####$

Software licensing Attention to building predictable Moderate. Short term, there

revenue streams through will be less of an impact on

↑

nontraditional software overall software revenue.

licensing models will increase. Toward the back end of the

#####

forecast period, the impact on

software revenue will be higher.

U.S. homeland There will be an increase in Low. Security spending is not

security government programs to significantly on software yet;

↔

improve homeland security and spending is currently on

protect against terrorism. physical security. Software

###$$

growth will be affected beyond

the five-year forecast period.

Services-oriented Services-oriented architectures Moderate. In the short term,

architectures will allow companies to speed existing systems will be

the development of rearchitected and new

modularized applications and integration technologies will be

respond faster to new business

pressure.

deployed, which will improve

business processes/

↑ ####$

automation. In the midterm,

applications will begin to be

replaced.

22 #32391 ©2004 IDC

T ABLE 3

Key Forecast Assumptions for the Worldwide Security Software Market,

2004–2008

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

Application There will be demand for clear High. This demand will require

verticalization and unique software vendor vendors to develop more

↔

product differentiation, faster sophisticated partnerships and

implementation, and more increase market applicability of

####$

relevant "out of box" solutions. offered solutions (particularly to

SMEs).

Market ecosystem

Services IT services will continue to grow Moderate. These trends are

as companies attempt to already factored in.

concentrate on what they do

best and rely on IT services to

handle complexity they cannot.

Companies clearly see the

advantages of using outside ↔ ####$

services and outsourcers. IT

services will grow faster than

the overall IT market as

budgets shift from internal

spending to external

companies.

Consumption

Buying sentiment IT buyers will begin to Moderate. These trends are

moderately spend again as the already factored in.

economy improves; CIOs will

begin to replace hardware and

operating systems, begin to

↑

spend on mobility, and regain

the attitude that IT spending is

####$

critical to the well-being of a

company (or household). IT

spending as a percentage of

revenue (or income) will

increase.

Saturation PC and Internet markets will Moderate. These trends are

continue to saturate, but already factored in.

↔

emerging geographies will

invest and new applications will

####$

drive users to multiplatform

usage.

Legend: #$$$$ very low, ##$$$ low, ###$$ moderate, ####$ high, ##### very high

Source: IDC, July 2004

©2004 IDC #32391 23

ESSENTIAL GUIDANCE

The 2003 onslaught of viruses and worms such as Blaster, Nachi, and SoBig not only

highlights the importance of keeping security solutions up to date, it also shines a

spotlight on the growing need for more proactive security products and services. The

rapid infection by these new worm and virus attacks means that slow responses will

cripple most customer environments because they will not be able to get ahead of the

initial infection and the far more serious reinfections. Malicious hackers are getting

much more sophisticated and faster at exploiting application vulnerabilities. Zero-day

attacks that take advantage of software vulnerabilities for which there are no available

fixes are starting to be viewed as a major threat to data security.

Intrusion detection and preventions products will continue to gain acceptance as a

way to eliminate Internet worms and maintain control over the internal working of

enterprise networks and applications. A new segment of ID&P products designed

specifically to protect and segment the internal network is beginning to emerge. IDC

is dubbing this the "FireDoor" market. FireDoor's will primarily use behavioral or

anomaly detection and policy rules to identify variations and unexpected events that

signal attacks, anomalous behavior, and misuse and abuse. They also can be very

good for worm detection, segmentation of virtual domains for protection of proprietary

or sensitive information, and verification of authentication credentials. The FireDoor

products will eventually include much more prevention as they are used to seal off

network segments from worms and other automated attacks recognized within a

company's network.

Firewall/VPN software products must be able to have smooth integration with

complementary security products, such as intrusion detection and content security. In

doing so, the software firewall/VPN can evolve into the unified threat management

space that is emerging in the appliances market. Vendors should also look closely at

partnering with managed service providers. These service providers will eventually

provide firewalls as an embedded service; to succeed, the software vendor must

capture some of this market. Software vendors must also offer options that can

compete with the faster-growing firewall/VPN security appliance market. Licensing

and partnerships will be required to remain strong in this market.

Government and industry regulations will continue to put unprecedented pressure on

corporations to secure access to information and applications not just with

employees, but also with customers, partners, and contractors. Moreover, budgetary

and staffing constraints will continue to drive organizations to look for better ways to

cost effectively manage their security infrastructure. Security solutions that can

simplify the complexity associated with managing multiple security solutions, while at

the same time increasing the effectiveness of protection will be key.

24 #32391 ©2004 IDC

LE ARN MORE

Related Research

! Worldwide Antispam 2004–2008 Forecast Update and 2003 Vendor Shares

(forthcoming)

! Worldwide Identity and Access Management 2004–2008 Forecast and 2003

Competitive Vendor Shares: The Death of Security 3A, Part I (IDC #31997,

November 2004)

! Worldwide Security and Vulnerability Management 2004–2008 Forecast and

2003 Vendor Shares: The Death of Security 3A, Part II (IDC #32008, November

2004)

! Worldwide Vulnerability Assessment and Management 2004–2008 Forecast and

2003 Vendor Shares: Assessing Risk and Compliance (IDC #32026, October

2004)

! Worldwide Intrusion Detection and Prevention 2004–2008 Forecast and 2003

Vendor Shares: Introducing the FireDoor (IDC #32004, October 2004)

! Worldwide Threat Management Security Appliances 2004–2008 Forecast and

2003 Vendor Shares: The Rise of the Unified Threat Management Security

Appliance (IDC #31840, September 2004)

! Worldwide Firewall Software 2004–2008 Forecast and 2003 Vendor Shares:

Desktop Firewalls on the Move (IDC #31839, September 2004)

! Worldwide Antivirus 2004–2008 Forecast and 2003 Vendor Shares (IDC #31737,

August 2004)

! Worldwide Secure Content Management 2004–2008 Forecast Update and 2003

Vendor Shares: A Holistic View of Antivirus, Web Filtering, and Messaging

Security (IDC #31598, August 2004)

! IDC's Software Taxonomy, 2004 (IDC #30838, February 2004)

©2004 IDC #32391 25

Copyright Notice

This IDC research document was published as part of an IDC continuous intelligence

service, providing written research, analyst interactions, telebriefings, and

conferences. Visit www.idc.com to learn more about IDC subscription and consulting

services. To view a list of IDC offices worldwide, visit www.idc.com/offices. Please

contact the IDC Hotline at 800.343.4952, ext. 7988 (or +1.508.988.7988) or

sales@idc.com for information on applying the price of this document toward the

purchase of an IDC service or for information on additional copies or Web rights.

Copyright 2004 IDC. Reproduction is forbidden unless authorized. All rights reserved.

Published Under Services: Security Products; 3As Security; Secure Content

Management; Intrusion Detection and Vulnerability Assessment; Firewalls and

Security Appliances; Mobile Security Software

26 #32391 ©2004 IDC

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Saks SKSDocument1 pageSaks SKSapi-3702531100% (1)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Indian Insider Buyings June 19, 2008-DhananDocument2 pagesIndian Insider Buyings June 19, 2008-Dhananapi-3702531No ratings yet

- Dillard DDSDocument1 pageDillard DDSapi-3702531100% (2)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- SMG PLC - ProfileDocument4 pagesSMG PLC - Profileapi-3702531No ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Walmart WMTDocument1 pageWalmart WMTapi-3702531100% (2)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- BSE Special Situations 19th June 2008Document5 pagesBSE Special Situations 19th June 2008api-3702531No ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Half Yearly Report 2007-08Document44 pagesHalf Yearly Report 2007-08api-3702531No ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- GilletteDocument14 pagesGilletteapi-3702531No ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Avon Product AVPDocument1 pageAvon Product AVPapi-3702531100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Dabur IndiaDocument43 pagesDabur Indiaapi-3702531No ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Fem CareDocument16 pagesFem Careapi-3702531No ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Colgate AR March 2006Document76 pagesColgate AR March 2006api-3702531No ratings yet

- Dabur India - 2Document51 pagesDabur India - 2api-3702531No ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- DUBARINDIAAR200708Document164 pagesDUBARINDIAAR200708Santosh KumarNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Annual Report 2007 2008Document84 pagesAnnual Report 2007 2008api-3702531No ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- March 2008 Consolidated ResultsDocument1 pageMarch 2008 Consolidated Resultsapi-3702531No ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Dabur IndiaDocument43 pagesDabur Indiaapi-3702531No ratings yet

- AR March 2007Document147 pagesAR March 2007api-3702531No ratings yet

- AR March 2003 - Only ConsolidatedDocument17 pagesAR March 2003 - Only Consolidatedapi-3702531No ratings yet

- AR March 2004 - Only ConsolidatedDocument17 pagesAR March 2004 - Only Consolidatedapi-3702531No ratings yet

- ColgateDocument32 pagesColgateapi-3702531No ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- ColgateDocument32 pagesColgateapi-3702531No ratings yet

- Colgate AR March 2007Document88 pagesColgate AR March 2007api-3702531No ratings yet

- AR March 2005Document116 pagesAR March 2005api-3702531No ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- AR March 2006Document36 pagesAR March 2006api-3702531No ratings yet

- Colgate AR March 2004Document72 pagesColgate AR March 2004api-3702531No ratings yet

- Colgate AR March 2005Document72 pagesColgate AR March 2005ashusingh0141No ratings yet

- 4q07 08Document1 page4q07 08api-3702531No ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Colgate AR March 2003Document72 pagesColgate AR March 2003api-3702531No ratings yet

- Colgate AR March 2002Document88 pagesColgate AR March 2002api-3702531No ratings yet

- Grandstream Networks, Inc.: HA100 High Availability Kit For UCM6510Document11 pagesGrandstream Networks, Inc.: HA100 High Availability Kit For UCM6510MOhamedNo ratings yet

- RAN Engineer PDFDocument4 pagesRAN Engineer PDFRadu Tudor ParaschivNo ratings yet

- Cmos 0 To 44 MHZ Single Chip 8-Bit Microntroller: DescriptionDocument20 pagesCmos 0 To 44 MHZ Single Chip 8-Bit Microntroller: DescriptionJoel Hauk HaukNo ratings yet

- MSBI Training Plans: Plan A Plan B Plan CDocument14 pagesMSBI Training Plans: Plan A Plan B Plan CVeerendra ReddyNo ratings yet

- Maya Lab 1Document1 pageMaya Lab 1MonoNo ratings yet

- Project 1 Creating A Dynamic Web Page: Header - PHP Footer - PHPDocument4 pagesProject 1 Creating A Dynamic Web Page: Header - PHP Footer - PHPIvan PangitNo ratings yet

- SBWP Customization (Tip For Inbox Customization)Document8 pagesSBWP Customization (Tip For Inbox Customization)koisakNo ratings yet

- Pillars of EcommerceDocument8 pagesPillars of EcommerceShaik YusafNo ratings yet

- Course Outline Software ArchitectureDocument3 pagesCourse Outline Software ArchitectureahmedNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Parallel Computers Networking PDFDocument48 pagesParallel Computers Networking PDFHemprasad BadgujarNo ratings yet

- Artificial Intelligence and PrivacyDocument14 pagesArtificial Intelligence and PrivacyVivekKumarNo ratings yet

- The Coca Cola Company PLC Official Yearly Prize Award Winners NotificationDocument7 pagesThe Coca Cola Company PLC Official Yearly Prize Award Winners NotificationHckron Farm1100% (1)

- (Object Oriented Programming) : CCS0023LDocument8 pages(Object Oriented Programming) : CCS0023LKross FordNo ratings yet

- Course Guide-CMSC311Document5 pagesCourse Guide-CMSC311Mark BernardinoNo ratings yet

- Datasheet Allplan Engineering PDFDocument2 pagesDatasheet Allplan Engineering PDFRafael PopaNo ratings yet

- Chapter 5 TableDocument106 pagesChapter 5 TableFOO POH YEENo ratings yet

- Health IT Security Risk Assessment ToolDocument57 pagesHealth IT Security Risk Assessment ToolTUP BOXNo ratings yet

- Google AdsDocument15 pagesGoogle AdsRituNo ratings yet

- Ds Oop Lab ManualDocument63 pagesDs Oop Lab ManualramaNo ratings yet

- Computer Technician Training CourseDocument8 pagesComputer Technician Training CourseApnhs ApequeñoNo ratings yet

- 07 Laboratory Exercise 1Document5 pages07 Laboratory Exercise 1kwalwalgud21No ratings yet

- Ai Engine Development For Versal: Olivier Tremois, PHD SW Technical Marketing Ai Engine ToolsDocument30 pagesAi Engine Development For Versal: Olivier Tremois, PHD SW Technical Marketing Ai Engine ToolsAliNo ratings yet

- ICT Lecture 08 Computer SoftwareDocument32 pagesICT Lecture 08 Computer SoftwareNasir Faraz KalmatiNo ratings yet

- Apple IIgs Demo SamplerDocument6 pagesApple IIgs Demo SamplerduesenNo ratings yet

- Ccnpv7.1 Switch Lab3-1 Vlan-trunk-Vtp StudentDocument20 pagesCcnpv7.1 Switch Lab3-1 Vlan-trunk-Vtp StudentItamar Zimmerman0% (1)

- Introduction To Embedded Systems: Melaku MDocument150 pagesIntroduction To Embedded Systems: Melaku MTalemaNo ratings yet

- Teracom Training Institute Ilt CatalogDocument16 pagesTeracom Training Institute Ilt CatalognebubuNo ratings yet

- Log View User GuideDocument53 pagesLog View User GuideSerhiiNo ratings yet

- PM Debug InfoDocument256 pagesPM Debug InfoGreg Edimilson GregNo ratings yet

- 02 - CCM - Functionality KeyCapabilities - EN - V1 2docxDocument31 pages02 - CCM - Functionality KeyCapabilities - EN - V1 2docxAnoop Kumar67% (3)