You might also like

- Bohemia QDocument2 pagesBohemia QSaakshi TiwariNo ratings yet

- Chapter 13 Variable CostingDocument3 pagesChapter 13 Variable CostingJJ JaumNo ratings yet

- Ch8 Absorption Variable Costing Income ReportingDocument19 pagesCh8 Absorption Variable Costing Income ReportingIsra' I. SweilehNo ratings yet

- Income Effects of Alternative Cost Accumulation SystemsDocument4 pagesIncome Effects of Alternative Cost Accumulation SystemssserwaddaNo ratings yet

- Overview of absorption and variable costing methodsDocument3 pagesOverview of absorption and variable costing methodsAreeb Baqai100% (1)

- MAS Variable and Absorption CostingDocument11 pagesMAS Variable and Absorption CostingGwyneth TorrefloresNo ratings yet

- Bohemia IndustriesDocument13 pagesBohemia Industriesaman100% (1)

- Cost Accounting Questions and Their AnswersDocument5 pagesCost Accounting Questions and Their Answerszulqarnainhaider450_No ratings yet

- Chapter 10Document5 pagesChapter 10Ailene QuintoNo ratings yet

- Vendmart - TheDocument6 pagesVendmart - TheSagarrajaNo ratings yet

- Cost Accounting AssignmentDocument12 pagesCost Accounting Assignmentridhim khandelwalNo ratings yet

- As Hi SHDocument2 pagesAs Hi SHMISHRACOMNo ratings yet

- LandauDocument7 pagesLandauRoe PerNo ratings yet

- Issues in Management Accounting Lecture 27 and 28Document7 pagesIssues in Management Accounting Lecture 27 and 28Muqadas JavedNo ratings yet

- Absorption Costing Technique Is Also Termed As Traditional or Full Cost MethodDocument2 pagesAbsorption Costing Technique Is Also Termed As Traditional or Full Cost MethodPankaj2cNo ratings yet

- Management Accounting AssignmentDocument21 pagesManagement Accounting AssignmentAadi KaushikNo ratings yet

- Management Accounting AssignmentDocument21 pagesManagement Accounting AssignmentAadi KaushikNo ratings yet

- Manage Accounting Assignment Breakeven AnalysisDocument21 pagesManage Accounting Assignment Breakeven AnalysisAadi KaushikNo ratings yet

- Costing and Profit PlanningDocument27 pagesCosting and Profit PlanningSIDDHANT CHUGHNo ratings yet

- CHP 11Document14 pagesCHP 11angela babyNo ratings yet

- Marginal Costing: Understanding Key Concepts and ApplicationsDocument9 pagesMarginal Costing: Understanding Key Concepts and ApplicationsPratyush Pratim SahariaNo ratings yet

- MAS Absorption Costing/Variable Costing Study ObjectivesDocument6 pagesMAS Absorption Costing/Variable Costing Study ObjectivesMarjorie ManuelNo ratings yet

- Section - A 201: (I) Discuss About Accounting PrinciplesDocument7 pagesSection - A 201: (I) Discuss About Accounting PrinciplesPrem KumarNo ratings yet

- Variable CostingDocument32 pagesVariable CostingNicole J. CentenoNo ratings yet

- Costing Marginal Final Sem 2Document37 pagesCosting Marginal Final Sem 2Abdul Qadir EzzyNo ratings yet

- Landau CompanyDocument4 pagesLandau Companysherwinrs100% (2)

- Strategic ManagementDocument42 pagesStrategic ManagementElvira CuadraNo ratings yet

- Break Even Analysis: Costing Systems and Techniques For Engineering CompaniesDocument6 pagesBreak Even Analysis: Costing Systems and Techniques For Engineering Companiesasimrafiq12No ratings yet

- Group 6 PPT - MGT AccountingDocument24 pagesGroup 6 PPT - MGT Accountingahnaf khoiryNo ratings yet

- Term Paper: Submitted ToDocument7 pagesTerm Paper: Submitted ToSwagy BoyNo ratings yet

- TempDocument28 pagesTempKIMBERLY MUKAMBANo ratings yet

- Marginal and Absorption CostingDocument3 pagesMarginal and Absorption CostingsyedzulqarnainhaiderNo ratings yet

- UGB253 Management Accounting Business FinalDocument15 pagesUGB253 Management Accounting Business FinalMohamed AzmalNo ratings yet

- Mas 2605Document6 pagesMas 2605John Philip CastroNo ratings yet

- BEP&CVPDocument10 pagesBEP&CVPNishanth PrabhakarNo ratings yet

- Managerial Accounting Case StudyDocument19 pagesManagerial Accounting Case StudyAnutaj NagpalNo ratings yet

- Ca 1 Costing TechniquesDocument6 pagesCa 1 Costing TechniquesORIYOMI KASALINo ratings yet

- Accounts Question - WIP - v1Document14 pagesAccounts Question - WIP - v1Manish KumarNo ratings yet

- Chapter 15 - Alternative Inventory Valuation MethodsDocument5 pagesChapter 15 - Alternative Inventory Valuation MethodsLemon VeinNo ratings yet

- Absorption CostingDocument23 pagesAbsorption Costingarman_277276271No ratings yet

- Chapter 2. - Activity Based Costing PPT Dec 2011Document5 pagesChapter 2. - Activity Based Costing PPT Dec 2011shemidaNo ratings yet

- Cost Accounting PresentationsDocument13 pagesCost Accounting PresentationsAdityaNo ratings yet

- Chapter 3 Accounting and Finance For ManagersDocument17 pagesChapter 3 Accounting and Finance For ManagersSiraj MohammedNo ratings yet

- Marginal Costing 300 Level-1Document23 pagesMarginal Costing 300 Level-1simon danielNo ratings yet

- Break Even AnalysisDocument16 pagesBreak Even Analysisapi-3723983100% (9)

- Marginal vs absorption costing: Understanding key differencesDocument5 pagesMarginal vs absorption costing: Understanding key differencesosama haseebNo ratings yet

- Absorption CostingDocument3 pagesAbsorption CostingThirayuth BeeNo ratings yet

- Absorption (Variable) Costing and Cost-Volume-Profit AnalysisDocument41 pagesAbsorption (Variable) Costing and Cost-Volume-Profit AnalysisPapsie PopsieNo ratings yet

- Assignment - Management AccountingDocument16 pagesAssignment - Management AccountingPriyaNo ratings yet

- Purpose of costing: value inventory, record costs, price products, make decisionsDocument13 pagesPurpose of costing: value inventory, record costs, price products, make decisionsSiddiqua KashifNo ratings yet

- Chapter 3 AkmenDocument28 pagesChapter 3 AkmenRomi AlfikriNo ratings yet

- Whiz Calculator Case StudyDocument4 pagesWhiz Calculator Case StudyKinjal MehtaNo ratings yet

- Breakeven AnalysisDocument16 pagesBreakeven AnalysisAbhinandan GolchhaNo ratings yet

- Absorption CostingDocument2 pagesAbsorption Costingvanessa claire abadNo ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Finance for Non-Financiers 2: Professional FinancesFrom EverandFinance for Non-Financiers 2: Professional FinancesNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Textbook of Urgent Care Management: Chapter 12, Pro Forma Financial StatementsFrom EverandTextbook of Urgent Care Management: Chapter 12, Pro Forma Financial StatementsNo ratings yet

- Salary (Proforma)Document15 pagesSalary (Proforma)Joshua Capa FrondaNo ratings yet

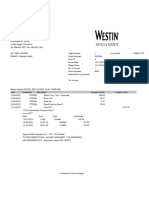

- Westin Hotels & Resorts - 2023-12-10 - 257.78Document2 pagesWestin Hotels & Resorts - 2023-12-10 - 257.78rahul.transcountsNo ratings yet

- Tanishq Brand Research ProjectDocument70 pagesTanishq Brand Research ProjectYashi Gupta0% (2)

- Klasifikasi Akurasi EstimasiDocument4 pagesKlasifikasi Akurasi EstimasiAdwina DesyandriNo ratings yet

- CSE4DSS Lecture 1 Decision Support and Business IntelligenceDocument53 pagesCSE4DSS Lecture 1 Decision Support and Business IntelligenceAbdulaziz AlaliNo ratings yet

- Jakarta Property Market Research Report Q3 2019Document16 pagesJakarta Property Market Research Report Q3 2019Deni MuliyawanNo ratings yet

- Muhammad Hassan Muhammad Hassan: ObjectiveDocument2 pagesMuhammad Hassan Muhammad Hassan: ObjectiveMohammad Hassan GhumroNo ratings yet

- 1b. Sustainment Unit Capability PE - Available Sustainment Units (v1)Document2 pages1b. Sustainment Unit Capability PE - Available Sustainment Units (v1)Steve RichardsNo ratings yet

- 1.1. Giấy chứng nhận BRCDocument1 page1.1. Giấy chứng nhận BRCTran HungNo ratings yet

- 183601fb151b9f5741a7fe66505ccc3dDocument35 pages183601fb151b9f5741a7fe66505ccc3dLeonardo BritoNo ratings yet

- OHSAS 18001 GuideDocument10 pagesOHSAS 18001 Guidevij2009No ratings yet

- Totem Catalogue 1Document28 pagesTotem Catalogue 1RevanNo ratings yet

- Balance SheetDocument1 pageBalance Sheetdhuvad.2004No ratings yet

- International Capital MovementDocument37 pagesInternational Capital MovementAnonymous tvdt6znW3No ratings yet

- Toyota Shaw Dispute Over Delivery of VehicleDocument6 pagesToyota Shaw Dispute Over Delivery of Vehiclemanol_salaNo ratings yet

- PaymentNotification ZHN7CF9B13 FNBRSA02 PDFDocument1 pagePaymentNotification ZHN7CF9B13 FNBRSA02 PDFManzini Mlebogeng100% (1)

- Prospectus 2013 MT Kenya University KINGDOMDocument34 pagesProspectus 2013 MT Kenya University KINGDOMJennifer WelchNo ratings yet

- MusharakaDocument29 pagesMusharakaNauman AminNo ratings yet

- Telenor Easypaisa Market ShareDocument11 pagesTelenor Easypaisa Market ShareSyed Nawazish Mehdi Zaidi100% (1)

- Payables Open Interface Import in Oracle Apps R12Document11 pagesPayables Open Interface Import in Oracle Apps R12sudharshan79No ratings yet

- Arslan Khan 1 Pager CV PDFDocument1 pageArslan Khan 1 Pager CV PDFImran KhanNo ratings yet

- Press Release (Company Update)Document3 pagesPress Release (Company Update)Shyam SunderNo ratings yet

- Westlaw India Delivery SummaryDocument8 pagesWestlaw India Delivery SummaryBenjamin BallardNo ratings yet

- Auditing Trs by IcapDocument53 pagesAuditing Trs by IcapArif AliNo ratings yet

- Analysis AssignmentDocument3 pagesAnalysis AssignmentmadyanoshieNo ratings yet

- Make My TripDocument4 pagesMake My TripAhmad NoorNo ratings yet

- PT Prima Elektronik Journal Entries December 2015Document1 pagePT Prima Elektronik Journal Entries December 2015Syoheh PamujiNo ratings yet

- Training Syllabus 2 Days Makers InstituteDocument4 pagesTraining Syllabus 2 Days Makers InstitutePriyo SudarsonoNo ratings yet

- CB MEC Group 1Document51 pagesCB MEC Group 1Jessa Mae VelardeNo ratings yet

- HW 1accountingDocument2 pagesHW 1accountingMarjorie PalmaNo ratings yet