You might also like

- Direct Tax CodeDocument8 pagesDirect Tax CodeImran HassanNo ratings yet

- Unit 1Document5 pagesUnit 1piyush.birru25No ratings yet

- Vaishnavi ProjectDocument72 pagesVaishnavi ProjectAkshada DhapareNo ratings yet

- St. Mary'S Technical Campus, Kolkata Mba 3 Semester: Q1 Write Short Notes On (Any Five)Document22 pagesSt. Mary'S Technical Campus, Kolkata Mba 3 Semester: Q1 Write Short Notes On (Any Five)Barkha LohaniNo ratings yet

- TaxationDocument7 pagesTaxationAkshatNo ratings yet

- BASICS OF TAXATION (Income Tax Ordinance, 1984) Updated Till Finance Act. 2013 by Prof. Mahbubur RahmanDocument14 pagesBASICS OF TAXATION (Income Tax Ordinance, 1984) Updated Till Finance Act. 2013 by Prof. Mahbubur RahmansaadmansheedyNo ratings yet

- Direct Taxation: CA M. Ram Pavan KumarDocument60 pagesDirect Taxation: CA M. Ram Pavan KumarSravyaNo ratings yet

- Value Added Tax Black Book 2 2332Document47 pagesValue Added Tax Black Book 2 2332sanket yelaweNo ratings yet

- Employment Income TaxDocument10 pagesEmployment Income TaxHarsh Nahar100% (1)

- Income Tax - Income Tax Department, IT Returns, E-Filing, Tax Slab FY 2020-21Document11 pagesIncome Tax - Income Tax Department, IT Returns, E-Filing, Tax Slab FY 2020-21LAKSHMANARAO PNo ratings yet

- Direct Tax Vs Indirect TaxDocument44 pagesDirect Tax Vs Indirect TaxShuchi BhatiaNo ratings yet

- Direct Tax Vs Indirect TaxDocument44 pagesDirect Tax Vs Indirect TaxShuchi BhatiaNo ratings yet

- Tax Reforms in India: Static DimensionsDocument11 pagesTax Reforms in India: Static DimensionsLeela LazarNo ratings yet

- B9-057 - VanshPatel - Assignment 4Document6 pagesB9-057 - VanshPatel - Assignment 4Vansh PatelNo ratings yet

- TAX Definition - : Tax Is A Compulsory Contribution Imposed by The Government On ItsDocument22 pagesTAX Definition - : Tax Is A Compulsory Contribution Imposed by The Government On ItsSayanm MittalNo ratings yet

- Presenting: Direct Tax - Trends in IndiaDocument27 pagesPresenting: Direct Tax - Trends in IndiatusharNo ratings yet

- Corporate Income Taxes and Tax RatesDocument38 pagesCorporate Income Taxes and Tax RatesShaheen ShahNo ratings yet

- Indian Income Tax Calculator: Double Click The IT Calculator - IT Will Automatically Calculate The Taxable AmountDocument23 pagesIndian Income Tax Calculator: Double Click The IT Calculator - IT Will Automatically Calculate The Taxable AmountshankarinsideNo ratings yet

- 1) Explain GST and Its BenefitsDocument14 pages1) Explain GST and Its BenefitsRohit VishwakarmaNo ratings yet

- Taxation ProjectDocument83 pagesTaxation ProjectManish JaiswalNo ratings yet

- Unit 2Document5 pagesUnit 2piyush.birru25No ratings yet

- 05 Corporate Tax Planning and ManagementDocument34 pages05 Corporate Tax Planning and ManagementHimanshu SharmaNo ratings yet

- Taxation in IndiaDocument9 pagesTaxation in IndiaSiva BalanNo ratings yet

- Direct Tax CodeDocument10 pagesDirect Tax Codejgaurav80No ratings yet

- Tax Planning For Year 2010Document24 pagesTax Planning For Year 2010Mehak BhargavaNo ratings yet

- DTC - FinalDocument18 pagesDTC - FinalvjranavjNo ratings yet

- Tax Bulletin - Issue 2Document26 pagesTax Bulletin - Issue 2Sindura KuloNo ratings yet

- Tax PlanningDocument7 pagesTax PlanningJyoti SinghNo ratings yet

- Taxation System in IndiaDocument35 pagesTaxation System in IndiaSaif UddinNo ratings yet

- Corporate TaxDocument30 pagesCorporate TaxVijay KumarNo ratings yet

- The New Direct Tax Code (DTC)Document18 pagesThe New Direct Tax Code (DTC)aggarwalajay2No ratings yet

- IFBPDocument11 pagesIFBPmohanraokp2279No ratings yet

- Income Tax in IndiaDocument19 pagesIncome Tax in IndiaConcepts TreeNo ratings yet

- Taxation Law Project ON Effect of Specialized Taxation Slabs Under Start-Up IndiaDocument9 pagesTaxation Law Project ON Effect of Specialized Taxation Slabs Under Start-Up IndiaShaji SebastianNo ratings yet

- Tax PlanningDocument28 pagesTax PlanningDishaNo ratings yet

- Deloitte Tax Alert - Corporate Tax Rates Slashed and Fiscal Relief AnnouncedDocument4 pagesDeloitte Tax Alert - Corporate Tax Rates Slashed and Fiscal Relief AnnouncedSunil GidwaniNo ratings yet

- Income Tax - IT Returns, E Filing, Tax Saving, Income Tax Slabs, Rules & Laws - All About Income TaxDocument6 pagesIncome Tax - IT Returns, E Filing, Tax Saving, Income Tax Slabs, Rules & Laws - All About Income TaxLAKSHMANARAO P100% (1)

- Income Tax EXPLAINATIONDocument11 pagesIncome Tax EXPLAINATIONVishwas AgarwalNo ratings yet

- AX Lanning: by Anup K SuchakDocument27 pagesAX Lanning: by Anup K SuchakanupsuchakNo ratings yet

- IFRS-Deferred Tax Balance Sheet ApproachDocument8 pagesIFRS-Deferred Tax Balance Sheet ApproachJitendra JawalekarNo ratings yet

- Tax AuditDocument49 pagesTax AuditRebecca Mendes100% (1)

- Project Topic: Income Tax Systems in Pakistan, India & UKDocument53 pagesProject Topic: Income Tax Systems in Pakistan, India & UKAfzal RocksxNo ratings yet

- Fiscal PolicyDocument6 pagesFiscal PolicySourav KaranthNo ratings yet

- The Rigours of TDS - An OverviewDocument31 pagesThe Rigours of TDS - An OverviewShaleenPatniNo ratings yet

- Tax System in IndiaDocument18 pagesTax System in IndiaDEV HUGENNo ratings yet

- 1) How Income Tax Works in India?: GST Is One of The Biggest Indirect Tax Reforms in The CountryDocument21 pages1) How Income Tax Works in India?: GST Is One of The Biggest Indirect Tax Reforms in The Countryaher unnatiNo ratings yet

- Corporate Taxation in BangladeshDocument8 pagesCorporate Taxation in Bangladeshskn092No ratings yet

- DTC ProvisionsDocument3 pagesDTC ProvisionsrajdeeppawarNo ratings yet

- Summary of Thailand-Tax-Guide and LawsDocument34 pagesSummary of Thailand-Tax-Guide and LawsPranav BhatNo ratings yet

- CTP Unit 3Document10 pagesCTP Unit 3SANDEEP KUMARNo ratings yet

- Simply Cleaning: Taxation IssuesDocument10 pagesSimply Cleaning: Taxation IssuesadeelmuzaffaralamNo ratings yet

- Taxation System in IndiaDocument30 pagesTaxation System in IndiaSwapnil Pisal-DeshmukhNo ratings yet

- Interview QuestionsDocument12 pagesInterview QuestionsnadeemNo ratings yet

- Expectations From BudgetDocument8 pagesExpectations From BudgetNehaNo ratings yet

- Tax System: BY Arpita Pali Prachi Jaiswal Mansi MahaleDocument30 pagesTax System: BY Arpita Pali Prachi Jaiswal Mansi MahaleSiddharth SharmaNo ratings yet

- Finance Bill, 2012: Provisions Relating To Direct TaxesDocument36 pagesFinance Bill, 2012: Provisions Relating To Direct TaxessangeetsindanNo ratings yet

- "Comparative Study of DTC (Direct Tax Code) Effective From 1april 2012." 1. IntroductionDocument11 pages"Comparative Study of DTC (Direct Tax Code) Effective From 1april 2012." 1. IntroductionAnurag GuptaNo ratings yet

- Minimum Alternate TaxDocument20 pagesMinimum Alternate Taxmuskan khatriNo ratings yet

- Introduction To Indian Tax StructureDocument45 pagesIntroduction To Indian Tax StructureSadir AlamNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- FatturaNotaCredito 54035 2021 BZ PEDocument1 pageFatturaNotaCredito 54035 2021 BZ PEAdnan KotorićNo ratings yet

- Income Tax Ordinance 1984 - Amended Upto July 2022Document382 pagesIncome Tax Ordinance 1984 - Amended Upto July 2022Sumit GNo ratings yet

- Assessment Task 2 - BSBHRM513Document44 pagesAssessment Task 2 - BSBHRM513Xavar Xan0% (3)

- Nurse Call RegDocument96 pagesNurse Call RegRAJESH THAMPYNo ratings yet

- PEDRO DA MOTTA VEIGA (Foreign Direct Investment in Brazil Regulation, Flows and Contribution To Development, 2004)Document55 pagesPEDRO DA MOTTA VEIGA (Foreign Direct Investment in Brazil Regulation, Flows and Contribution To Development, 2004)apto123100% (1)

- Qiagen Business ServicesDocument2 pagesQiagen Business ServicesGuile Gabriel AlogNo ratings yet

- Activity 1 Wih AnswersDocument2 pagesActivity 1 Wih AnswersDianna Tercino IINo ratings yet

- Benefits of GSTDocument18 pagesBenefits of GSTHiteshi AggarwalNo ratings yet

- GGSR (Chapter 2-Organizations-Their Political, Structural and Economic Environment)Document17 pagesGGSR (Chapter 2-Organizations-Their Political, Structural and Economic Environment)Princess Alay-ay100% (2)

- Tax Cases FinalsDocument21 pagesTax Cases FinalsAngie DouglasNo ratings yet

- Nishit MarvaniaDocument3 pagesNishit Marvaniaone_and_only_you0076406No ratings yet

- 24-7 Intouch India Private LimitedDocument1 page24-7 Intouch India Private LimitedMohammed Adnan ShariefNo ratings yet

- Inbutax Fundamentals of Income TaxationDocument21 pagesInbutax Fundamentals of Income TaxationAsh AdoNo ratings yet

- Protecting Legacy The Value of A Family OfficeDocument25 pagesProtecting Legacy The Value of A Family OfficeRavi BabuNo ratings yet

- Nit75 PMC BhopalDocument64 pagesNit75 PMC BhopalFaisal KhanNo ratings yet

- 2018 Substative PeocedureDocument6 pages2018 Substative PeocedureAliNo ratings yet

- Complete 420 Manual SIS Unit 89Document231 pagesComplete 420 Manual SIS Unit 89Tri Wahyuningsih100% (1)

- Global Cash Card - Paystub Detail PDFDocument1 pageGlobal Cash Card - Paystub Detail PDFVerónica Del RioNo ratings yet

- Invoice 7538177918Document1 pageInvoice 7538177918Venu Gopal ReddyNo ratings yet

- The Daily Tar Heel For April 8, 2014Document10 pagesThe Daily Tar Heel For April 8, 2014The Daily Tar HeelNo ratings yet

- Books AmazonDocument1 pageBooks AmazonmohitNo ratings yet

- Personal Finance ActivitiesDocument32 pagesPersonal Finance ActivitiesRonald CatapangNo ratings yet

- Adopt-A-School Program Kit 2019Document30 pagesAdopt-A-School Program Kit 2019Winny FelipeNo ratings yet

- Cases On Lifting of Corporate VeilDocument9 pagesCases On Lifting of Corporate VeiltheutsavsharmaNo ratings yet

- Adampak AR 09Document74 pagesAdampak AR 09diffsoftNo ratings yet

- DRAFT Stay of Demand by CA NITIN KANWARDocument13 pagesDRAFT Stay of Demand by CA NITIN KANWARAmandeep Vats91% (11)

- Estate and Donor Rrs and RamoDocument12 pagesEstate and Donor Rrs and Ramocmv mendozaNo ratings yet

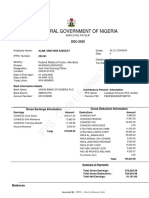

- IPPIS - Oracle E-Business Suite: Federal Government of NigeriaDocument1 pageIPPIS - Oracle E-Business Suite: Federal Government of NigeriaAlimi kehinde100% (1)

- Cisco Case StudyDocument10 pagesCisco Case Studywillie.erasmus7023No ratings yet

- Dabistan-e-Ijtihaad - 99 Names of Holy Prophet Muhammad (Saw)Document2 pagesDabistan-e-Ijtihaad - 99 Names of Holy Prophet Muhammad (Saw)Salman MirzaNo ratings yet