You might also like

- House Budget Control ActDocument9 pagesHouse Budget Control ActMichael Robert HusseyNo ratings yet

- CBO - Congressional Budget Office - Analysis On Harry Reid Debt Ceiling Proposed Plan - July 27th 2011Document11 pagesCBO - Congressional Budget Office - Analysis On Harry Reid Debt Ceiling Proposed Plan - July 27th 2011Zim VicomNo ratings yet

- CBO Analysis Obama's Budget 2012 3/18Document22 pagesCBO Analysis Obama's Budget 2012 3/18Darla DawaldNo ratings yet

- The Budget Control Act of 2011: The Effects On Spending and The Budget Deficit When The Automatic Spending Cuts Are ImplementedDocument19 pagesThe Budget Control Act of 2011: The Effects On Spending and The Budget Deficit When The Automatic Spending Cuts Are ImplementedcaseywootenNo ratings yet

- CBO Letter March 5Document18 pagesCBO Letter March 5ZerohedgeNo ratings yet

- Us Cbo Budget DeficitsDocument18 pagesUs Cbo Budget Deficitswmartin46No ratings yet

- Rep Paul Ryan On Obamas 2012 Budget and BeyondDocument19 pagesRep Paul Ryan On Obamas 2012 Budget and BeyondKim HedumNo ratings yet

- Budget Update August 2005Document6 pagesBudget Update August 2005Committee For a Responsible Federal BudgetNo ratings yet

- US CBO Report: Fiscal Restraint That Is Scheduled To Occur in 2013 (May, 2012)Document10 pagesUS CBO Report: Fiscal Restraint That Is Scheduled To Occur in 2013 (May, 2012)wmartin46No ratings yet

- Analysis of CBO's August 2011 Baseline and Update of CRFB Realistic Baseline August 24, 2011Document6 pagesAnalysis of CBO's August 2011 Baseline and Update of CRFB Realistic Baseline August 24, 2011Committee For a Responsible Federal BudgetNo ratings yet

- Fy11 Supplemental Budget Plan As of 0701112Document10 pagesFy11 Supplemental Budget Plan As of 0701112aaron_m_morrisseyNo ratings yet

- DeficitReduction ScreenDocument46 pagesDeficitReduction ScreenPeggy W SatterfieldNo ratings yet

- Budget Update March 142006Document10 pagesBudget Update March 142006Committee For a Responsible Federal BudgetNo ratings yet

- CBO Score and Assessment To Repeal ObamacareDocument10 pagesCBO Score and Assessment To Repeal ObamacareDarla DawaldNo ratings yet

- DeficitReduction PrintDocument35 pagesDeficitReduction PrintPeggy W SatterfieldNo ratings yet

- FY 13 OMB JC Sequestration ReportDocument83 pagesFY 13 OMB JC Sequestration ReportCeleste KatzNo ratings yet

- Updated Estimates of The Fiscal Commission Proposal: June 29, 2011Document15 pagesUpdated Estimates of The Fiscal Commission Proposal: June 29, 2011Committee For a Responsible Federal BudgetNo ratings yet

- Sequestration and The Super Committee: Background On The Budget Control ActDocument4 pagesSequestration and The Super Committee: Background On The Budget Control Actwatton1217No ratings yet

- Updated Estimates of The Fiscal Commission Proposal: June 29, 2011Document15 pagesUpdated Estimates of The Fiscal Commission Proposal: June 29, 2011Committee For a Responsible Federal BudgetNo ratings yet

- Economic Impacts of Waiting To Resolve The Long Term Budget ImbalanceDocument12 pagesEconomic Impacts of Waiting To Resolve The Long Term Budget ImbalanceMilton RechtNo ratings yet

- Budget Response FY 2012 FINALDocument17 pagesBudget Response FY 2012 FINALCeleste KatzNo ratings yet

- J What Is SequestrationDocument3 pagesJ What Is SequestrationDanica BalinasNo ratings yet

- 2013 CB Sfaff OverviewDocument79 pages2013 CB Sfaff OverviewChris Capper LiebenthalNo ratings yet

- Eroding Our Foundation: Sequestration, R&D, Innovation and U.S. Economic GrowthDocument34 pagesEroding Our Foundation: Sequestration, R&D, Innovation and U.S. Economic GrowthAlex FitzpatrickNo ratings yet

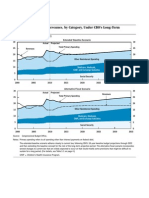

- Primary Spending and Revenues, by Category, Under CBO's Long-Term Budget ScenariosDocument25 pagesPrimary Spending and Revenues, by Category, Under CBO's Long-Term Budget ScenariosPeggy W SatterfieldNo ratings yet

- CBO On Minimum WageDocument17 pagesCBO On Minimum WageThe Western JournalNo ratings yet

- 2014-2015 City of Sacramento Budget OverviewDocument34 pages2014-2015 City of Sacramento Budget OverviewCapital Public RadioNo ratings yet

- An Update To The Budget and Economic Outlook: Fiscal Years 2012 To 2022Document75 pagesAn Update To The Budget and Economic Outlook: Fiscal Years 2012 To 2022api-167354334No ratings yet

- Tentative Budget - Final Friday Nov 12 RevDocument111 pagesTentative Budget - Final Friday Nov 12 RevAlfonso RobinsonNo ratings yet

- Connecticut 2014.01.09 Opm Debt Reduction ReportDocument17 pagesConnecticut 2014.01.09 Opm Debt Reduction ReportHelen BennettNo ratings yet

- CBO January 2015 Outlook On ObamacareDocument15 pagesCBO January 2015 Outlook On ObamacareZenger NewsNo ratings yet

- WA Senate Proposed Operating BudgetDocument34 pagesWA Senate Proposed Operating BudgetKING 5 NewsNo ratings yet

- Testimony On The 2013 Long-Term Budget OutlookDocument8 pagesTestimony On The 2013 Long-Term Budget OutlookSteven HansenNo ratings yet

- US General Accounting Office (GAO) Long Term Government Fiscal Outlook (March, 2001)Document12 pagesUS General Accounting Office (GAO) Long Term Government Fiscal Outlook (March, 2001)wmartin46No ratings yet

- Douglas W. Elmendorf, Director U.S. Congress Washington, DC 20515Document50 pagesDouglas W. Elmendorf, Director U.S. Congress Washington, DC 20515josephragoNo ratings yet

- OMB Sequestration Update Report To The President and Congress For Fiscal Year 2013 August 20, 2012Document22 pagesOMB Sequestration Update Report To The President and Congress For Fiscal Year 2013 August 20, 2012Peggy W SatterfieldNo ratings yet

- New Job Effects of Eliminating The Automatic Spending Reductions CBODocument3 pagesNew Job Effects of Eliminating The Automatic Spending Reductions CBOPatricia DillonNo ratings yet

- Congressional Budget Office U.S. Congress Washington, DC 20515Document17 pagesCongressional Budget Office U.S. Congress Washington, DC 20515api-26139761No ratings yet

- US Fiscal DujavuDocument20 pagesUS Fiscal DujavuAnuchaLorthongkhamNo ratings yet

- Fy 2013 July UpdateDocument281 pagesFy 2013 July UpdateNick ReismanNo ratings yet

- GNYHA Memo New York State Budget 2012Document12 pagesGNYHA Memo New York State Budget 2012ahawkins2865No ratings yet

- Democratic Budget Framework: A Balanced, Pro-Growth, and Fair Deficit Reduction PlanDocument4 pagesDemocratic Budget Framework: A Balanced, Pro-Growth, and Fair Deficit Reduction PlanInterActionNo ratings yet

- Highlights of The Governors Budget ProposalDocument44 pagesHighlights of The Governors Budget ProposalRichard Costigan IIINo ratings yet

- Senator Murray Budget Memo 1-24Document12 pagesSenator Murray Budget Memo 1-24Ezra Klein100% (1)

- Budget Analysis 2011 12Document7 pagesBudget Analysis 2011 12s lalithaNo ratings yet

- CBO Report On The Cost of The Breast Cancer Research Semi Postal StampDocument4 pagesCBO Report On The Cost of The Breast Cancer Research Semi Postal StampPostalReporter.comNo ratings yet

- Omb Sequestration ReportDocument394 pagesOmb Sequestration ReportJake GrovumNo ratings yet

- 2010 Budget Perspective: The Real Deficit Effect of The Health BillDocument5 pages2010 Budget Perspective: The Real Deficit Effect of The Health BillWashington ExaminerNo ratings yet

- BENTE RCSD Budget Analysis FinalDocument5 pagesBENTE RCSD Budget Analysis FinalmarybadamsNo ratings yet

- Budget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018From EverandBudget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018No ratings yet

- Strengthening Fiscal Decentralization in Nepal’s Transition to FederalismFrom EverandStrengthening Fiscal Decentralization in Nepal’s Transition to FederalismNo ratings yet

- Implementing Results-Based Budget Management Frameworks: An Assessment of Progress in Selected CountriesFrom EverandImplementing Results-Based Budget Management Frameworks: An Assessment of Progress in Selected CountriesNo ratings yet

- Fiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesFrom EverandFiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesNo ratings yet

- Local Public Finance Management in the People's Republic of China: Challenges and OpportunitiesFrom EverandLocal Public Finance Management in the People's Republic of China: Challenges and OpportunitiesNo ratings yet

- Fossil Fuel Subsidies in Indonesia: Trends, Impacts, and ReformsFrom EverandFossil Fuel Subsidies in Indonesia: Trends, Impacts, and ReformsNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Read Trump's Letter To PelosiDocument6 pagesRead Trump's Letter To Pelosikballuck194% (95)

- Fifth Circuit Obamacare RulingDocument98 pagesFifth Circuit Obamacare RulingLaw&CrimeNo ratings yet

- Equal Rights Amendment LawsuitDocument24 pagesEqual Rights Amendment LawsuitMike Cason0% (1)

- Judiciary Impeachment ProcessDocument55 pagesJudiciary Impeachment ProcessM Mali100% (1)

- El Paso County Et Al v. Trump Et Al Permanent InjunctionDocument21 pagesEl Paso County Et Al v. Trump Et Al Permanent InjunctionDoug MataconisNo ratings yet

- California Et Al v. Trump Et Al OpinionDocument47 pagesCalifornia Et Al v. Trump Et Al OpinionDoug MataconisNo ratings yet

- Jackson Women's Health v. Dobbs OpinionDocument32 pagesJackson Women's Health v. Dobbs OpinionDoug MataconisNo ratings yet

- Articles of ImpeachmentDocument9 pagesArticles of ImpeachmentKelli R. Grant67% (3)

- White House Response To HJC - Impeachment Groundwork HearingDocument5 pagesWhite House Response To HJC - Impeachment Groundwork HearingThe Conservative Treehouse91% (11)

- Full Report Hpsci Impeachment Inquiry - 20191203Document300 pagesFull Report Hpsci Impeachment Inquiry - 20191203Mollie Reilly100% (36)

- George Zimmerman LawsuitDocument36 pagesGeorge Zimmerman LawsuitPeterBurkeNo ratings yet

- N.Y.S. Rifle & Pistol Assn v. New YorkDocument81 pagesN.Y.S. Rifle & Pistol Assn v. New YorkDoug MataconisNo ratings yet

- 2019-12-02 Report of Evidence in The Democrats' Impeachment Inquiry in The House of RepresentativesDocument123 pages2019-12-02 Report of Evidence in The Democrats' Impeachment Inquiry in The House of Representativesheather timmonsNo ratings yet

- WatchdogDocument476 pagesWatchdogblc88No ratings yet

- Kelly Mehlenbacher's Resignation LetterDocument1 pageKelly Mehlenbacher's Resignation LetterDeep ClipsNo ratings yet

- House Judiciary Chairman Jerry Nadler's Letter To TrumpDocument13 pagesHouse Judiciary Chairman Jerry Nadler's Letter To TrumpStefan BecketNo ratings yet

- Trump v. Vance Et Al OpinopmDocument34 pagesTrump v. Vance Et Al OpinopmDoug Mataconis0% (1)

- Robinson Et Al v. Marshall Et Al Preliminary InjunctionDocument19 pagesRobinson Et Al v. Marshall Et Al Preliminary InjunctionDoug MataconisNo ratings yet

- California Supreme Court On Tax ReturnsDocument53 pagesCalifornia Supreme Court On Tax ReturnsLaw&CrimeNo ratings yet

- David Holmes TestimonyDocument12 pagesDavid Holmes TestimonyVictor I NavaNo ratings yet

- Amb.. William Taylor TestimonyDocument17 pagesAmb.. William Taylor TestimonyDoug MataconisNo ratings yet

- Gordon Sondland Opening StatementDocument23 pagesGordon Sondland Opening StatementDoug MataconisNo ratings yet

- Petition For WritDocument179 pagesPetition For WritMeghashyam MaliNo ratings yet

- Judiciary Committee v. McGahn Et AlDocument120 pagesJudiciary Committee v. McGahn Et AlDoug Mataconis100% (2)

- Signal 2019 11 21 001355 3Document8 pagesSignal 2019 11 21 001355 3Anonymous CT8HyGhM100% (2)

- Dept. of Homeland Security Et Al v. Regents of Univ. of California Et AlDocument102 pagesDept. of Homeland Security Et Al v. Regents of Univ. of California Et AlDoug MataconisNo ratings yet

- Alexander Vindman StatementDocument6 pagesAlexander Vindman StatementKaroliNo ratings yet

- Mueller Report MaterialDocument75 pagesMueller Report MaterialDanny ChaitinNo ratings yet

- Trump Et Al v. Mazars Et AlDocument7 pagesTrump Et Al v. Mazars Et AlDoug MataconisNo ratings yet

- Read Impeachment ResolutionDocument8 pagesRead Impeachment Resolutionkballuck1100% (2)

- Child Protection Case Management Sop - Final - 18 April 2016Document50 pagesChild Protection Case Management Sop - Final - 18 April 2016AmshinwariNo ratings yet

- Town of Rosthern Coucil Minutes October 2008Document4 pagesTown of Rosthern Coucil Minutes October 2008LGRNo ratings yet

- PINAY Maurice-pseud.-The Secret Driving Force of Communism 1963 PDFDocument80 pagesPINAY Maurice-pseud.-The Secret Driving Force of Communism 1963 PDFneirotsih75% (4)

- History NewsletterDocument2 pagesHistory Newsletterapi-731025032No ratings yet

- Staff Sample IPCRsDocument10 pagesStaff Sample IPCRsJocelyn Herrera0% (1)

- TerrorismDocument33 pagesTerrorismRitika Kansal100% (1)

- IAS Compass - Current Affairs Compilation For Mains - Polity Governance2023Document206 pagesIAS Compass - Current Affairs Compilation For Mains - Polity Governance2023Anurag TiwariNo ratings yet

- M商贸签证所需资料ENGDocument2 pagesM商贸签证所需资料ENG焦建致No ratings yet

- Nestor-İskender: Historians of The Ottoman EmpireDocument8 pagesNestor-İskender: Historians of The Ottoman EmpireMirikaaNo ratings yet

- Political Conflicts Hamper Bangladesh's Economy While Taiwan ThrivesDocument6 pagesPolitical Conflicts Hamper Bangladesh's Economy While Taiwan Thrivesscribd1314No ratings yet

- Jusmag V NLRCDocument4 pagesJusmag V NLRCOliveros DMNo ratings yet

- 0011 Voters - List. Bay, Laguna - Brgy Bitin - Precint.0133aDocument5 pages0011 Voters - List. Bay, Laguna - Brgy Bitin - Precint.0133aIwai MotoNo ratings yet

- Vigilantibus Et Non Dormientibus Jura SubveniuntDocument3 pagesVigilantibus Et Non Dormientibus Jura SubveniuntferozekasNo ratings yet

- NEWS ARTICLE and SHOT LIST-Ugandan Peacekeeping Troops in Somalia Mark Tarehe Sita' DayDocument6 pagesNEWS ARTICLE and SHOT LIST-Ugandan Peacekeeping Troops in Somalia Mark Tarehe Sita' DayATMISNo ratings yet

- Zafra Vs PeopleDocument4 pagesZafra Vs PeopleKling King100% (1)

- Philippine Politics and Government Quiz ReviewDocument3 pagesPhilippine Politics and Government Quiz ReviewJundee L. Carrillo100% (1)

- Ss Curriculum OverviewDocument6 pagesSs Curriculum Overviewapi-246087744No ratings yet

- The History and Political Transition of Zimbabwe From Mugabe To Mnangagwa 1st Ed 9783030477325 9783030477332 CompressDocument469 pagesThe History and Political Transition of Zimbabwe From Mugabe To Mnangagwa 1st Ed 9783030477325 9783030477332 CompressMaurice GavhureNo ratings yet

- JapanDocument8 pagesJapanDavora LopezNo ratings yet

- The National Security Agency and The EC-121 Shootdown (S-CCO)Document64 pagesThe National Security Agency and The EC-121 Shootdown (S-CCO)Robert ValeNo ratings yet

- Constitutional MonarchyDocument3 pagesConstitutional MonarchyCeleste Marie Serrano RosalesNo ratings yet

- BBOC NoticeDocument2 pagesBBOC NoticeQueen DTNo ratings yet

- Comelec ResolutionsDocument23 pagesComelec ResolutionsRavenFoxNo ratings yet

- Strategies To Practice Liberation Strategies To Dismantle OppressionDocument2 pagesStrategies To Practice Liberation Strategies To Dismantle OppressionAri El VoyagerNo ratings yet

- Japan China Relations Troubled Water To Calm SeasDocument9 pagesJapan China Relations Troubled Water To Calm SeasFrattazNo ratings yet

- Contract EssentialsDocument3 pagesContract EssentialsNoemiAlodiaMoralesNo ratings yet

- 1 - StatutesDocument4 pages1 - Statutessaloni gargNo ratings yet

- The Role of Religion in The Yugoslav WarDocument16 pagesThe Role of Religion in The Yugoslav Warapi-263913260100% (1)

- Tabogon, CebuDocument2 pagesTabogon, CebuSunStar Philippine NewsNo ratings yet

- History of R.A. 9163 (NSTP)Document7 pagesHistory of R.A. 9163 (NSTP)Vlad LipsamNo ratings yet