You might also like

- Hotel AccountsDocument374 pagesHotel AccountsBijo JacobNo ratings yet

- Financial Report of HotelDocument28 pagesFinancial Report of HotelShandya MaharaniNo ratings yet

- Asignment 3 Hotel Recovery AnalysisDocument24 pagesAsignment 3 Hotel Recovery AnalysisGAANo ratings yet

- Om - Monthly ReportDocument81 pagesOm - Monthly ReportRajeshbabhu Rajeshbabhu100% (1)

- Round 4-Team Goodness: Hotel Profitability and RatiosDocument10 pagesRound 4-Team Goodness: Hotel Profitability and RatiosAshish MishraNo ratings yet

- BHM 402T PDFDocument120 pagesBHM 402T PDFKamlesh HarbolaNo ratings yet

- Projected Financials - RAM Resorts and Hotels CorporationDocument12 pagesProjected Financials - RAM Resorts and Hotels CorporationCharlene Tiong100% (1)

- Hotel Budget SummaryDocument1 pageHotel Budget SummaryAlanSooNo ratings yet

- 02.hotel Initial - Revenue Projection - Revised IDocument145 pages02.hotel Initial - Revenue Projection - Revised Ianon_843580047No ratings yet

- Uniform System Of Accounts For The Lodging Industry | Major ChangesDocument8 pagesUniform System Of Accounts For The Lodging Industry | Major ChangestodowedeNo ratings yet

- EXCEL-P&L Mid MonthDocument2 pagesEXCEL-P&L Mid Monthrutley1No ratings yet

- Cost Accounting in HotelsDocument2 pagesCost Accounting in HotelsMuaaz ButtNo ratings yet

- Copy (2) of Marketing of Five Star HotelsDocument84 pagesCopy (2) of Marketing of Five Star HotelsSohil KotichaNo ratings yet

- A Rate StructureDocument12 pagesA Rate StructureAmeen IbraheemNo ratings yet

- Revpar & Market ShareDocument15 pagesRevpar & Market ShareroyrenaldoNo ratings yet

- Standard Procedure For Hotel Sales Team Incentives PlanDocument2 pagesStandard Procedure For Hotel Sales Team Incentives PlanImee S. Yu0% (1)

- Dokument - Pub 11th Edition Uniform Accounting Converted Flipbook PDFDocument317 pagesDokument - Pub 11th Edition Uniform Accounting Converted Flipbook PDFWahyu KusumaNo ratings yet

- Hampton Inn YTD Financial Statement ComparisonDocument9 pagesHampton Inn YTD Financial Statement Comparisonmohd_shaarNo ratings yet

- Qatar Review Q1 2016 enDocument6 pagesQatar Review Q1 2016 enahmedh_98No ratings yet

- Swimming Pool RULESDocument47 pagesSwimming Pool RULESNafas AqNo ratings yet

- Sha566 TurnadotDocument7 pagesSha566 TurnadotBambang JuliantoNo ratings yet

- Management: Things To Know AboutDocument28 pagesManagement: Things To Know AboutNataliaNo ratings yet

- Sales & Marketing Plan - CompletedDocument20 pagesSales & Marketing Plan - CompletedAna Nurul LailaNo ratings yet

- Functional Systems: 4 & 6 October 2010Document14 pagesFunctional Systems: 4 & 6 October 2010Ram PowruNo ratings yet

- What Is Revenue Management ProcessDocument6 pagesWhat Is Revenue Management ProcessREZ YieldNo ratings yet

- Pre-opening finance checklistDocument3 pagesPre-opening finance checklistQasimNo ratings yet

- Ebook - Pricing StrategyDocument28 pagesEbook - Pricing StrategySilvie Wacknbath100% (2)

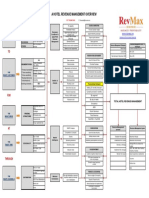

- A Hotel Revenue Management Overview - v4Document1 pageA Hotel Revenue Management Overview - v4Tó GonçalvesNo ratings yet

- Food and Beverage ManagerDocument3 pagesFood and Beverage ManagerQuy TranxuanNo ratings yet

- The Hotel Revenue Managers Essential Guide To SegmentationDocument18 pagesThe Hotel Revenue Managers Essential Guide To SegmentationAmalia L StefanNo ratings yet

- Basic Hotel Investment and DevelopmentDocument45 pagesBasic Hotel Investment and DevelopmentYuri AndhikaNo ratings yet

- Establishing Hotel Room RatesDocument4 pagesEstablishing Hotel Room RatesNiharNo ratings yet

- Revenue Management For DummiesDocument4 pagesRevenue Management For DummiesAna BuduNo ratings yet

- Family Business Succession A Strategic Planning ModelDocument4 pagesFamily Business Succession A Strategic Planning Modelleopedrazac22No ratings yet

- HOSPA Finance Community USALI PDFDocument56 pagesHOSPA Finance Community USALI PDFVanjB.Payno100% (1)

- DHR Co Fi Sop 007 Vat SalesDocument3 pagesDHR Co Fi Sop 007 Vat SalesDeo Patria HerdriantoNo ratings yet

- Daily LogDocument1 pageDaily LogTarun MaudgalyaNo ratings yet

- Career Path at Hotels (Draft)Document63 pagesCareer Path at Hotels (Draft)SPHM HospitalityNo ratings yet

- Hotel SWOTDocument5 pagesHotel SWOTLove AuteNo ratings yet

- Hotel Management Fees Miss The MarkDocument9 pagesHotel Management Fees Miss The MarkMiguel RiveraNo ratings yet

- Business Plan Name Institution DateDocument9 pagesBusiness Plan Name Institution Dateapi-611376322No ratings yet

- USALI ChangesDocument4 pagesUSALI ChangesYayat MiharyaNo ratings yet

- Inside IHG: Start ReadingDocument16 pagesInside IHG: Start ReadingSven SerkowskiNo ratings yet

- Hotel Operations-1 (Chapter-6)Document14 pagesHotel Operations-1 (Chapter-6)VishnuNarayanan Viswanatha PillaiNo ratings yet

- USALI 10th VS 11th EditionDocument7 pagesUSALI 10th VS 11th EditionvictoregomezNo ratings yet

- Mipim2014 Programme at A GlanceDocument33 pagesMipim2014 Programme at A GlanceChristian Hôtel Le FlorianNo ratings yet

- Hotel Sales OfficeDocument14 pagesHotel Sales OfficeAgustinus Agus PurwantoNo ratings yet

- Hotel JargonsDocument5 pagesHotel JargonsChristine Joy GelicameNo ratings yet

- Evolution of The Hospitality Asset Management - 6-7-8 - FinalDocument27 pagesEvolution of The Hospitality Asset Management - 6-7-8 - FinalĐàoMinhPhươngNo ratings yet

- The Hubbart FormulaDocument5 pagesThe Hubbart FormulaBenjaminRyan100% (1)

- Hotel Success Handbook Action ListDocument27 pagesHotel Success Handbook Action Listaliko555No ratings yet

- Restaurant Entrepreneur Project-Student RequirementsDocument1 pageRestaurant Entrepreneur Project-Student Requirementsapi-262218593No ratings yet

- Assistant Property Manager/ Residential Concierge ManagerDocument2 pagesAssistant Property Manager/ Residential Concierge Managerapi-77174907No ratings yet

- Irfs and Us GaapDocument7 pagesIrfs and Us Gaapabissi67No ratings yet

- Financial Analysis - Sonesta International Hotels CorporationDocument11 pagesFinancial Analysis - Sonesta International Hotels CorporationAishaNo ratings yet

- Hotels and ReseDocument200 pagesHotels and ReseCathrina Joy MacalmaNo ratings yet

- Hotel Budget Spreadsheet ExcelDocument16 pagesHotel Budget Spreadsheet ExcelLinn Htet OoNo ratings yet

- Presented By:-Shruti Agrawal (046) Ridhima Kapoor (040) Saloni Monga (043) Kunal Pokarna (024) Priyanka Ghosh Ashish JainDocument22 pagesPresented By:-Shruti Agrawal (046) Ridhima Kapoor (040) Saloni Monga (043) Kunal Pokarna (024) Priyanka Ghosh Ashish JainShruti AgrawalNo ratings yet