You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- (Prelim 3RD Lesson) Customers' Meal Experience and Desired Attributes of Food and Beverage Service PersonnelDocument26 pages(Prelim 3RD Lesson) Customers' Meal Experience and Desired Attributes of Food and Beverage Service PersonnelLiza MaryNo ratings yet

- A Systematic Review of Biochar Use in Animal Waste CompostingDocument10 pagesA Systematic Review of Biochar Use in Animal Waste CompostingRoberto José Haro SevillaNo ratings yet

- Quizzer-CAPITAL BUDGETING - Non-Discounted (With Solutions)Document3 pagesQuizzer-CAPITAL BUDGETING - Non-Discounted (With Solutions)Ferb Cruzada80% (5)

- Lakme: Latest Quarterly/Halfyearly As On (Months)Document7 pagesLakme: Latest Quarterly/Halfyearly As On (Months)Vikas UpadhyayNo ratings yet

- G09-23 QuotationDocument5 pagesG09-23 QuotationRonish ChandraNo ratings yet

- Upendra Son Tirkey: Mail: inDocument3 pagesUpendra Son Tirkey: Mail: inTriptiNo ratings yet

- Csec Poa January 2012 p2Document9 pagesCsec Poa January 2012 p2Renelle RampersadNo ratings yet

- Letter From Sir Andrew Dilnot To Chris Leslie MP On The National Infrastructure PlanDocument4 pagesLetter From Sir Andrew Dilnot To Chris Leslie MP On The National Infrastructure PlanpoliticshomeukNo ratings yet

- Protecting Legacy The Value of A Family OfficeDocument25 pagesProtecting Legacy The Value of A Family OfficeRavi BabuNo ratings yet

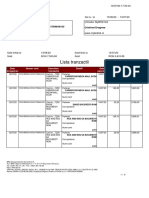

- Lista Tranzactii: Cristinel Dragnea RO81BRDE410SV31789944100 RON Cristinel DragneaDocument6 pagesLista Tranzactii: Cristinel Dragnea RO81BRDE410SV31789944100 RON Cristinel DragneaSebastian PSNo ratings yet

- Erwin DI Business Glossary Management GuideDocument149 pagesErwin DI Business Glossary Management GuideleoluiNo ratings yet

- Ipripak Org Justification For More Provinces PDFDocument8 pagesIpripak Org Justification For More Provinces PDFIshfa UmarNo ratings yet

- PRIMAMAJU R® Steel Product BrochureDocument8 pagesPRIMAMAJU R® Steel Product BrochurekongkokkingNo ratings yet

- ABC Audit Representation LetterDocument3 pagesABC Audit Representation LetterMatthew TsangNo ratings yet

- Elanza Export Private Limited: Company ProfileDocument9 pagesElanza Export Private Limited: Company ProfileKapil SinghNo ratings yet

- Test Bank For Multinational Business Finance 15th by EitemanDocument36 pagesTest Bank For Multinational Business Finance 15th by Eitemandiodontmetacism.0jw2al100% (37)

- International Student Exchange Programme Indicative Grade Point Average (iGPA) Fall 2021Document3 pagesInternational Student Exchange Programme Indicative Grade Point Average (iGPA) Fall 2021Koh Zi YangNo ratings yet

- Box Breakout System Trading ManualDocument11 pagesBox Breakout System Trading ManualAramaii TiNo ratings yet

- CFP Investment Planning Study Notes SampleDocument28 pagesCFP Investment Planning Study Notes SampleMeenakshi67% (3)

- Chapter 4 - Form of OwnershipDocument25 pagesChapter 4 - Form of OwnershipSabra NadeemNo ratings yet

- Seminar 15Document23 pagesSeminar 15Chann ChannNo ratings yet

- Kenya Electricity Billing ExplainedDocument4 pagesKenya Electricity Billing Explainedford merfordNo ratings yet

- Confluence 101: Getting Started in ConfluenceDocument22 pagesConfluence 101: Getting Started in ConfluenceKent TipanNo ratings yet

- Chapter 05 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Document196 pagesChapter 05 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Awais Azeemi100% (3)

- Tanzania High Court Ruling on Company Lawsuit ObjectionsDocument15 pagesTanzania High Court Ruling on Company Lawsuit ObjectionsdavidNo ratings yet

- Avoiding Theoretical Stagnation - A Systematic Review and Framework For Measuring Public ValueDocument19 pagesAvoiding Theoretical Stagnation - A Systematic Review and Framework For Measuring Public ValuezooopsNo ratings yet

- 2020 Sustainable Agriculture Standard Farm Requirements Rainforest AllianceDocument86 pages2020 Sustainable Agriculture Standard Farm Requirements Rainforest AllianceSofia MontañezNo ratings yet

- Chapter (5) : Public CorporationsDocument18 pagesChapter (5) : Public Corporationskhant ooNo ratings yet

- Vechicle Rental ModulesDocument3 pagesVechicle Rental ModulesKeerthi Vasan LNo ratings yet

- Teaching Note - Customer Analytics at FlipkartDocument12 pagesTeaching Note - Customer Analytics at FlipkartARPAN100% (1)