You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Mortgage and Pivot Table-RepuelaDocument2 pagesMortgage and Pivot Table-RepuelaFrancis Loie RepuelaNo ratings yet

- PUBLIC SECTOR BANKS Consolidated Balance SheetsDocument2 pagesPUBLIC SECTOR BANKS Consolidated Balance SheetsJogenderNo ratings yet

- Gorton and MetrikDocument43 pagesGorton and MetrikJustin EpsteinNo ratings yet

- Contingent Liabilities Meaning and TypesDocument2 pagesContingent Liabilities Meaning and Typesi readyNo ratings yet

- FM Group 4Document21 pagesFM Group 4Jerus CruzNo ratings yet

- Valuation of Fixed IncomeDocument45 pagesValuation of Fixed IncomeANKIT AGARWALNo ratings yet

- 1 - Week 3 Assignment Module 3 Bond Valuation WorksheetDocument2 pages1 - Week 3 Assignment Module 3 Bond Valuation WorksheetAhmad S YuddinNo ratings yet

- Non-Bank Gfis: GoccsDocument35 pagesNon-Bank Gfis: GoccsAnalyn Grace BasayNo ratings yet

- Valuing BondsDocument26 pagesValuing BondsMohammad Taqiyuddin RahmanNo ratings yet

- Working Capital: Apl Apollo Tubes LTDDocument17 pagesWorking Capital: Apl Apollo Tubes LTDDhirajsharma123No ratings yet

- Kerine DennisDocument99 pagesKerine Dennisalicewilliams83nNo ratings yet

- What Is A Coupon BondDocument3 pagesWhat Is A Coupon BondNazrul IslamNo ratings yet

- Sample Questions For SWAPDocument4 pagesSample Questions For SWAPKarthik Nandula100% (1)

- Assignment 2Document2 pagesAssignment 2Joseph OndariNo ratings yet

- Simple Interest-Simple DiscountDocument55 pagesSimple Interest-Simple DiscountSharmaine BeranNo ratings yet

- NBFC Thematic On Securitisation - Spark - 25nov19Document35 pagesNBFC Thematic On Securitisation - Spark - 25nov19chetankvoraNo ratings yet

- Comparative AnalysisDocument6 pagesComparative AnalysisKathryn Bianca AcanceNo ratings yet

- Perjanjian Pinjaman Polisi: Policy Loan AgreementDocument2 pagesPerjanjian Pinjaman Polisi: Policy Loan Agreementlimited legacyNo ratings yet

- Case 7 SolutionsDocument3 pagesCase 7 SolutionsMichale Jacomilla50% (2)

- Credit TransactionsDocument46 pagesCredit TransactionsKyla DabalmatNo ratings yet

- Case 5 IBC Akshay Jhunjhunwala Anr. Vs Union of India Calcutta High CourtDocument26 pagesCase 5 IBC Akshay Jhunjhunwala Anr. Vs Union of India Calcutta High CourtsasNo ratings yet

- Credit and CollectionDocument2 pagesCredit and CollectionApple Cabalse Rimando100% (1)

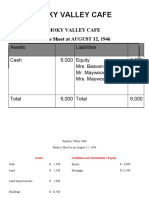

- Smoky Valley CafeDocument3 pagesSmoky Valley CafeRajkumar KrishnamoorthyNo ratings yet

- 2022 Aug T1Document6 pages2022 Aug T1mustardNo ratings yet

- Gen Math Q2 W1 2 QADocument34 pagesGen Math Q2 W1 2 QAarneahagacoscos090No ratings yet

- Simple Interest - 2021-2022Document23 pagesSimple Interest - 2021-2022racquel bagaNo ratings yet

- Contract of Loan SheDocument2 pagesContract of Loan SheFrancis LayagNo ratings yet

- 2 SampleDocument23 pages2 Sampleaaaaammmmm8900% (1)

- Bihar Stamp Duty and Registration Charges BiharDocument1 pageBihar Stamp Duty and Registration Charges BiharAkshansh NegiNo ratings yet

- Bad Boy Guaranties - Does The Punishment Fit The CrimeDocument3 pagesBad Boy Guaranties - Does The Punishment Fit The CrimeKarate BarbieNo ratings yet