You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- BDO Pay Ultimate GuideDocument8 pagesBDO Pay Ultimate Guidejulius004No ratings yet

- NAB Classic Banking Account Balance and Transaction DetailsDocument4 pagesNAB Classic Banking Account Balance and Transaction DetailsAinur RahmanNo ratings yet

- Zelle Fraud Tutarial by Kaushal Pal 2023Document21 pagesZelle Fraud Tutarial by Kaushal Pal 2023RobNo ratings yet

- Guide To Proof of CashDocument3 pagesGuide To Proof of CashRose Ann Juleth LicayanNo ratings yet

- Bank Statement SummaryDocument4 pagesBank Statement SummaryDerene JohnsonNo ratings yet

- Sbi Statement 2 March 27 MarchDocument15 pagesSbi Statement 2 March 27 Marchjubin josephNo ratings yet

- Appraisal Memo Cash Credit LimitDocument23 pagesAppraisal Memo Cash Credit LimitMuana LalthlaNo ratings yet

- 10 10 2023-DocumentDocument6 pages10 10 2023-DocumentgarrettloehrNo ratings yet

- Buze Proposal NewDocument19 pagesBuze Proposal Newyared mulgetaNo ratings yet

- BCCBDocument104 pagesBCCBPrashanth Gowda100% (3)

- ReviewerDocument67 pagesReviewerKyungsoo DohNo ratings yet

- GroupAssignmentQuestion2Document2 pagesGroupAssignmentQuestion2Pankaj KhannaNo ratings yet

- HT - LTIP E-BillDocument4 pagesHT - LTIP E-BilljugalNo ratings yet

- The Fed's Press Release On Stress TestsDocument1 pageThe Fed's Press Release On Stress TestsDealBookNo ratings yet

- Check Encumberance Certificate To Verify Property TitleDocument2 pagesCheck Encumberance Certificate To Verify Property TitlePVV RAMA RAONo ratings yet

- FN 40 Under 40 Rising Stars in IBDocument14 pagesFN 40 Under 40 Rising Stars in IBEdna ConceiçãoNo ratings yet

- Islamic Finance Final ProjectDocument3 pagesIslamic Finance Final ProjectMohammad AbdulrehmanNo ratings yet

- Metrobank Card Terms in 40 CharactersDocument13 pagesMetrobank Card Terms in 40 CharactersMark Titus Montoya RamosNo ratings yet

- Ledger Name Opening BalanceDocument3 pagesLedger Name Opening BalanceArista TechnologiesNo ratings yet

- Cim Assignment 4Document24 pagesCim Assignment 4Shashwat VaidyaNo ratings yet

- SAYAKGHOSH 14093011220 Unlocked PDFDocument7 pagesSAYAKGHOSH 14093011220 Unlocked PDFRaidey RaideyNo ratings yet

- Lipsey Chap.20Document21 pagesLipsey Chap.20Khuzaimah AhmadNo ratings yet

- UPI Error and Response Codes 2 9Document73 pagesUPI Error and Response Codes 2 9shailshasabeNo ratings yet

- Current Asset Management Chapter SummaryDocument14 pagesCurrent Asset Management Chapter SummaryLokamNo ratings yet

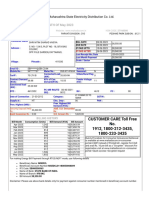

- Bill of Supply For The Month of Mar 2019: Maharashtra State Electricity Distribution Co - LTDDocument3 pagesBill of Supply For The Month of Mar 2019: Maharashtra State Electricity Distribution Co - LTDJyotsna TandelNo ratings yet

- H9 TK XFQK 7 SJ EXUrgDocument5 pagesH9 TK XFQK 7 SJ EXUrgmikeNo ratings yet

- Sedo GmbH Invoice for Order #3025091Document1 pageSedo GmbH Invoice for Order #3025091paul deaunaNo ratings yet

- Q2. Business and Consumer LoansDocument22 pagesQ2. Business and Consumer LoansCassy RabangNo ratings yet

- Corporate Finance Final ProjectDocument8 pagesCorporate Finance Final ProjectUsman ChNo ratings yet

- Account statement for Amit TiwariDocument2 pagesAccount statement for Amit TiwariAmit TiwariNo ratings yet