You might also like

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- US Internal Revenue Service: F1120pol - 2004Document6 pagesUS Internal Revenue Service: F1120pol - 2004IRSNo ratings yet

- COC Checklist FormDocument1 pageCOC Checklist Formfuel stationNo ratings yet

- The Aynak Copper Tender: Implications For Afghanistan and The WestDocument78 pagesThe Aynak Copper Tender: Implications For Afghanistan and The Westeasterncampaign100% (1)

- Electoral System in Great BritainDocument9 pagesElectoral System in Great BritainJennifer CampbellNo ratings yet

- PAYMENT FOR RIGHT OF WAY DOES NOT TRANSFER OWNERSHIPDocument2 pagesPAYMENT FOR RIGHT OF WAY DOES NOT TRANSFER OWNERSHIPyurets929No ratings yet

- (European Studies Series) Janine Garrisson (Auth.) - A History of Sixteenth-Century France, 1483-1598 - Renaissance, Reformation and Rebellion (1995, Macmillan Education UK)Document445 pages(European Studies Series) Janine Garrisson (Auth.) - A History of Sixteenth-Century France, 1483-1598 - Renaissance, Reformation and Rebellion (1995, Macmillan Education UK)Andr ValdirNo ratings yet

- Pahud v. CADocument3 pagesPahud v. CAdelayinggratificationNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- US Internal Revenue Service: F1120pol - 1999Document4 pagesUS Internal Revenue Service: F1120pol - 1999IRSNo ratings yet

- US Internal Revenue Service: F1120pol - 1994Document4 pagesUS Internal Revenue Service: F1120pol - 1994IRSNo ratings yet

- US Internal Revenue Service: F1120pol - 2000Document6 pagesUS Internal Revenue Service: F1120pol - 2000IRSNo ratings yet

- US Internal Revenue Service: F1120pol - 2001Document5 pagesUS Internal Revenue Service: F1120pol - 2001IRSNo ratings yet

- US Internal Revenue Service: f1120 - 1998Document4 pagesUS Internal Revenue Service: f1120 - 1998IRSNo ratings yet

- US Internal Revenue Service: F1120rei - 1999Document4 pagesUS Internal Revenue Service: F1120rei - 1999IRSNo ratings yet

- US Internal Revenue Service: F1120rei - 2001Document4 pagesUS Internal Revenue Service: F1120rei - 2001IRSNo ratings yet

- US Internal Revenue Service: F1120a - 1995Document2 pagesUS Internal Revenue Service: F1120a - 1995IRSNo ratings yet

- US Internal Revenue Service: F1120a - 2000Document2 pagesUS Internal Revenue Service: F1120a - 2000IRSNo ratings yet

- US Internal Revenue Service: F1120ric - 1996Document4 pagesUS Internal Revenue Service: F1120ric - 1996IRSNo ratings yet

- US Internal Revenue Service: f1120h - 2001Document4 pagesUS Internal Revenue Service: f1120h - 2001IRSNo ratings yet

- US Internal Revenue Service: f1120h - 1996Document4 pagesUS Internal Revenue Service: f1120h - 1996IRSNo ratings yet

- US Internal Revenue Service: f1120 - 1996Document4 pagesUS Internal Revenue Service: f1120 - 1996IRSNo ratings yet

- US Internal Revenue Service: f1120 - 2000Document4 pagesUS Internal Revenue Service: f1120 - 2000IRSNo ratings yet

- US Internal Revenue Service: f1120 - 2001Document4 pagesUS Internal Revenue Service: f1120 - 2001IRSNo ratings yet

- US Internal Revenue Service: F1120a - 1996Document2 pagesUS Internal Revenue Service: F1120a - 1996IRSNo ratings yet

- US Internal Revenue Service: F1120a - 1992Document2 pagesUS Internal Revenue Service: F1120a - 1992IRSNo ratings yet

- US Internal Revenue Service: f1120 - 1995Document4 pagesUS Internal Revenue Service: f1120 - 1995IRSNo ratings yet

- US Internal Revenue Service: f1120 - 2002Document4 pagesUS Internal Revenue Service: f1120 - 2002IRSNo ratings yet

- US Internal Revenue Service: f1120h - 1993Document4 pagesUS Internal Revenue Service: f1120h - 1993IRSNo ratings yet

- US Internal Revenue Service: f1120h - 2004Document6 pagesUS Internal Revenue Service: f1120h - 2004IRSNo ratings yet

- US Internal Revenue Service: f1065 - 1991Document4 pagesUS Internal Revenue Service: f1065 - 1991IRSNo ratings yet

- U.S. Return of Income For Electing Large Partnerships: Taxable Income or Loss From Passive Loss Limitation ActivitiesDocument5 pagesU.S. Return of Income For Electing Large Partnerships: Taxable Income or Loss From Passive Loss Limitation ActivitiesIRSNo ratings yet

- US Internal Revenue Service: F1120ric - 2001Document4 pagesUS Internal Revenue Service: F1120ric - 2001IRSNo ratings yet

- US Internal Revenue Service: F1120rei - 2000Document4 pagesUS Internal Revenue Service: F1120rei - 2000IRSNo ratings yet

- US Internal Revenue Service: f1120h - 1994Document4 pagesUS Internal Revenue Service: f1120h - 1994IRSNo ratings yet

- US Internal Revenue Service: F1120rei - 2005Document4 pagesUS Internal Revenue Service: F1120rei - 2005IRSNo ratings yet

- US Internal Revenue Service: F1120ric - 2000Document4 pagesUS Internal Revenue Service: F1120ric - 2000IRSNo ratings yet

- US Internal Revenue Service: f1065 - 1995Document4 pagesUS Internal Revenue Service: f1065 - 1995IRSNo ratings yet

- US Internal Revenue Service: F1120rei - 2004Document4 pagesUS Internal Revenue Service: F1120rei - 2004IRSNo ratings yet

- US Internal Revenue Service: F1120rei - 1993Document4 pagesUS Internal Revenue Service: F1120rei - 1993IRSNo ratings yet

- US Internal Revenue Service: f1066 - 1997Document4 pagesUS Internal Revenue Service: f1066 - 1997IRSNo ratings yet

- US Internal Revenue Service: f1066 - 2001Document4 pagesUS Internal Revenue Service: f1066 - 2001IRSNo ratings yet

- US Internal Revenue Service: F1120rei - 1992Document4 pagesUS Internal Revenue Service: F1120rei - 1992IRSNo ratings yet

- US Internal Revenue Service: f1120pc - 1998Document8 pagesUS Internal Revenue Service: f1120pc - 1998IRSNo ratings yet

- US Internal Revenue Service: f1065 AccessibleDocument4 pagesUS Internal Revenue Service: f1065 AccessibleIRSNo ratings yet

- US Internal Revenue Service: f1120s - 1992Document4 pagesUS Internal Revenue Service: f1120s - 1992IRSNo ratings yet

- US Internal Revenue Service: f1065 - 1996Document4 pagesUS Internal Revenue Service: f1065 - 1996IRSNo ratings yet

- US Internal Revenue Service: f1065 - 1997Document4 pagesUS Internal Revenue Service: f1065 - 1997IRSNo ratings yet

- US Internal Revenue Service: f1065 - 2000Document4 pagesUS Internal Revenue Service: f1065 - 2000IRSNo ratings yet

- U.S. Real Estate Mortgage Investment Conduit (REMIC) Income Tax ReturnDocument4 pagesU.S. Real Estate Mortgage Investment Conduit (REMIC) Income Tax ReturnIRSNo ratings yet

- US Internal Revenue Service: f1066 - 1991Document4 pagesUS Internal Revenue Service: f1066 - 1991IRSNo ratings yet

- US Internal Revenue Service: F1120a - 2005Document2 pagesUS Internal Revenue Service: F1120a - 2005IRSNo ratings yet

- US Internal Revenue Service: f1120pc - 1996Document8 pagesUS Internal Revenue Service: f1120pc - 1996IRSNo ratings yet

- Corporation Application For Tentative Refund: Sign HereDocument1 pageCorporation Application For Tentative Refund: Sign HereIRSNo ratings yet

- US Internal Revenue Service: f990t - 1994Document4 pagesUS Internal Revenue Service: f990t - 1994IRSNo ratings yet

- 2010 Blank IRS Form 1065Document5 pages2010 Blank IRS Form 1065Nick PechaNo ratings yet

- US Internal Revenue Service: F1120ric - 2004Document4 pagesUS Internal Revenue Service: F1120ric - 2004IRSNo ratings yet

- U.S. Corporation Income Tax Return: Sign HereDocument4 pagesU.S. Corporation Income Tax Return: Sign HeresweetchaeNo ratings yet

- US Internal Revenue Service: f1120pc - 1999Document8 pagesUS Internal Revenue Service: f1120pc - 1999IRSNo ratings yet

- Excel Files Individuals AopDocument8 pagesExcel Files Individuals Aopapi-3700469No ratings yet

- US Internal Revenue Service: f1041qft - 1999Document4 pagesUS Internal Revenue Service: f1041qft - 1999IRSNo ratings yet

- US Internal Revenue Service: f941 - 2000Document4 pagesUS Internal Revenue Service: f941 - 2000IRSNo ratings yet

- US Internal Revenue Service: f1120pc - 1993Document8 pagesUS Internal Revenue Service: f1120pc - 1993IRSNo ratings yet

- US Internal Revenue Service: f941 - 2003Document4 pagesUS Internal Revenue Service: f941 - 2003IRSNo ratings yet

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- Holocaust Ed LRB 2308 P 4Document4 pagesHolocaust Ed LRB 2308 P 4Webster MilwaukeeNo ratings yet

- Usa V Ernst Et Al - Pacer 1-1Document24 pagesUsa V Ernst Et Al - Pacer 1-1FOX 61 WebstaffNo ratings yet

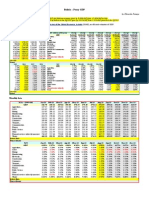

- Bolivia - Proxy GDPDocument1 pageBolivia - Proxy GDPEduardo PetazzeNo ratings yet

- Tada - Inspector of Factories LicenseDocument2 pagesTada - Inspector of Factories Licensecast techNo ratings yet

- Contemporary Period in The PhilippinesDocument2 pagesContemporary Period in The PhilippinesFRosales, Althea G.No ratings yet

- Military Review August 1967Document116 pagesMilitary Review August 1967mikle97No ratings yet

- The Doctrine of EclipseDocument12 pagesThe Doctrine of EclipseKanika Srivastava33% (3)

- Why 13s Should VoteDocument2 pagesWhy 13s Should VoteKathy ThachNo ratings yet

- (WMW) Misaalefua v. United States Postal Service - Document No. 4Document5 pages(WMW) Misaalefua v. United States Postal Service - Document No. 4Justia.comNo ratings yet

- Garafil vs. Office of The PresidentDocument43 pagesGarafil vs. Office of The PresidentMark Joseph Altura YontingNo ratings yet

- Ch-8. Internal Economies of Scale and Trade (Krugman)Document12 pagesCh-8. Internal Economies of Scale and Trade (Krugman)দুর্বার নকিবNo ratings yet

- Shtit June 2010 No 10Document60 pagesShtit June 2010 No 10balkanmonitorNo ratings yet

- PADILLA JR Vs COMELECDocument1 pagePADILLA JR Vs COMELECVonNo ratings yet

- SEIP Trainee Admission FormDocument2 pagesSEIP Trainee Admission FormRj IsratNo ratings yet

- Yesterday's Pending Mail and Telephonic Follow UpDocument8 pagesYesterday's Pending Mail and Telephonic Follow UpSingh AnupNo ratings yet

- Jurisprudence June 2016Document11 pagesJurisprudence June 2016Trishia Fernandez GarciaNo ratings yet

- Lagrosas V Brsitol Myers (GR 168637)Document2 pagesLagrosas V Brsitol Myers (GR 168637)Verlie FajardoNo ratings yet

- Raymond Corporate GovernanceDocument10 pagesRaymond Corporate GovernanceFoRam KapzNo ratings yet

- Pakistans Nine LivesDocument3 pagesPakistans Nine LivesAqsa NoorNo ratings yet

- Lakemont Shores POA Bylaws As of 2005Document11 pagesLakemont Shores POA Bylaws As of 2005PAAWS2No ratings yet

- Diversion of Corporate Opportunity CaseDocument2 pagesDiversion of Corporate Opportunity Casetsang hoyiNo ratings yet

- Ind Assignment 2 Imr451 PDFDocument15 pagesInd Assignment 2 Imr451 PDFSaiful Qaza0% (1)

- 4th Session National Assembly SecretariatDocument16 pages4th Session National Assembly SecretariatChoudhary Azhar YounasNo ratings yet

- Vaibhav Steel Corporation W.P.1735 of 2013 Dt.26.11.2013Document7 pagesVaibhav Steel Corporation W.P.1735 of 2013 Dt.26.11.2013sweetuhemuNo ratings yet