You might also like

- Axis Bank Analyst 08 09Document34 pagesAxis Bank Analyst 08 09goyalabhiNo ratings yet

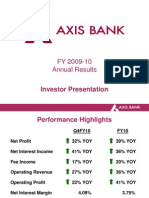

- FY 2009-10 Annual Results: Investor PresentationDocument34 pagesFY 2009-10 Annual Results: Investor PresentationDujesh KardamNo ratings yet

- Depreciation Drilling Rigs Esv2008Document108 pagesDepreciation Drilling Rigs Esv2008corsini999No ratings yet

- Discounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No FormulasDocument2 pagesDiscounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No Formulasrito2005No ratings yet

- SPS Sample ReportsDocument61 pagesSPS Sample Reportsphong.parkerdistributorNo ratings yet

- Atlas HondaDocument15 pagesAtlas HondaQasim AkramNo ratings yet

- Case 1 MarriottDocument14 pagesCase 1 Marriotthimanshu sagar100% (1)

- Annual ReportDocument156 pagesAnnual ReportTan Chee LeongNo ratings yet

- Combined Valuing Yahoo in 2013Document12 pagesCombined Valuing Yahoo in 2013Þorgeir DavíðssonNo ratings yet

- Britannia IndustriesDocument12 pagesBritannia Industriesmundadaharsh1No ratings yet

- Income Statemen-WPS OfficeDocument2 pagesIncome Statemen-WPS OfficeGuudax YareNo ratings yet

- 10 - Year - History 1990-2000Document1 page10 - Year - History 1990-2000catherineposadasNo ratings yet

- Pakistan State Oil Company Limited (Pso)Document6 pagesPakistan State Oil Company Limited (Pso)Maaz HanifNo ratings yet

- BSRM PresentationDocument4 pagesBSRM PresentationMostafa Noman DeepNo ratings yet

- BIOCON Ratio AnalysisDocument3 pagesBIOCON Ratio AnalysisVinuNo ratings yet

- Chapter 5 - Forecasting Chapter 5 BEDocument26 pagesChapter 5 - Forecasting Chapter 5 BEFadhila Nurfida HanifNo ratings yet

- Income Statement Template: Strictly ConfidentialDocument9 pagesIncome Statement Template: Strictly ConfidentialAnthony BenavidesNo ratings yet

- Ar 2014Document162 pagesAr 2014kokueiNo ratings yet

- Purchases / Average Payables Revenue / Average Total AssetsDocument7 pagesPurchases / Average Payables Revenue / Average Total AssetstannuNo ratings yet

- Review: Ten Year (Standalone)Document10 pagesReview: Ten Year (Standalone)maruthi631No ratings yet

- Xls179 Xls EngDocument3 pagesXls179 Xls EngIleannaNo ratings yet

- SL AR09 (Pg60to61)Document2 pagesSL AR09 (Pg60to61)omar471No ratings yet

- CL EducateDocument7 pagesCL EducateRicha SinghNo ratings yet

- Colgate Palmolive - DCF Valuation Model - Latest - Anurag 2Document44 pagesColgate Palmolive - DCF Valuation Model - Latest - Anurag 2Anrag Tiwari100% (1)

- Alro SA (ALR RO) - Adj HighlightsDocument147 pagesAlro SA (ALR RO) - Adj HighlightsAlexLupescuNo ratings yet

- Amtek Ratios 1Document18 pagesAmtek Ratios 1Dr Sakshi SharmaNo ratings yet

- P&L Profits and LostDocument12 pagesP&L Profits and LostMarcelo RodaoNo ratings yet

- Texas Roadhouse Published DataDocument2 pagesTexas Roadhouse Published DataKnagarNo ratings yet

- Caso TeuerDocument46 pagesCaso Teuerjoaquin bullNo ratings yet

- S9 - XLS069-XLS-ENG MarriottDocument12 pagesS9 - XLS069-XLS-ENG MarriottCarlosNo ratings yet

- Axiata Data Financials 4Q21bDocument11 pagesAxiata Data Financials 4Q21bhimu_050918No ratings yet

- DCF Valuation Pre Merger Southern Union CompanyDocument20 pagesDCF Valuation Pre Merger Southern Union CompanyIvan AlimirzoevNo ratings yet

- Harley-Davidson, Inc. (HOG) Stock Financials - Annual Income StatementDocument5 pagesHarley-Davidson, Inc. (HOG) Stock Financials - Annual Income StatementThe Baby BossNo ratings yet

- 2019 Q4 Financial Statement ENDocument17 pages2019 Q4 Financial Statement ENPinkky GithaNo ratings yet

- Hyundai Construction Equipment (IR 4Q20)Document17 pagesHyundai Construction Equipment (IR 4Q20)girish_patkiNo ratings yet

- Tata Motors Dupont and Altman Z-Score AnalysisDocument4 pagesTata Motors Dupont and Altman Z-Score AnalysisLAKHAN TRIVEDINo ratings yet

- Sapm AssignmentDocument4 pagesSapm Assignment401-030 B. Harika bcom regNo ratings yet

- Rosetta Stone IPODocument5 pagesRosetta Stone IPOFatima Ansari d/o Muhammad AshrafNo ratings yet

- Annual Trading Report: Strictly ConfidentialDocument3 pagesAnnual Trading Report: Strictly ConfidentialMunazza FawadNo ratings yet

- Ten Year Review - Standalone: Asian Paints LimitedDocument10 pagesTen Year Review - Standalone: Asian Paints Limitedmaruthi631No ratings yet

- CFI Income Statement TemplateDocument9 pagesCFI Income Statement Templatedhrivsitlani29No ratings yet

- Marriott (2) ..Document13 pagesMarriott (2) ..veninsssssNo ratings yet

- NYSF Walmart Templatev2Document49 pagesNYSF Walmart Templatev2Avinash Ganesan100% (1)

- Tugas Pertemuan 10 - Sopianti (1730611006)Document12 pagesTugas Pertemuan 10 - Sopianti (1730611006)sopiantiNo ratings yet

- Performance ReportDocument24 pagesPerformance ReportJuan VegaNo ratings yet

- Weekends TareaDocument9 pagesWeekends Tareasergio ramozNo ratings yet

- AmcDocument19 pagesAmcTimothy RenardusNo ratings yet

- Adani PortsDocument24 pagesAdani PortsManisha JhunjhunwalaNo ratings yet

- SWM Annual Report 2016Document66 pagesSWM Annual Report 2016shallynna_mNo ratings yet

- Cost of Capital - NikeDocument6 pagesCost of Capital - NikeAditi KhaitanNo ratings yet

- Financial Statement ANalysis of National Foods Limited Pakistan From 2005-2009Document97 pagesFinancial Statement ANalysis of National Foods Limited Pakistan From 2005-2009shahid Ali88% (8)

- Adidas/Reebok Merger: Collin Shaw Kelly Truesdale Michael Rockette Benedikte Schmidt SaravanansadaiyappanDocument27 pagesAdidas/Reebok Merger: Collin Shaw Kelly Truesdale Michael Rockette Benedikte Schmidt SaravanansadaiyappanUdipta DasNo ratings yet

- 新城发展2022年中期业绩PPT 0830v1Document39 pages新城发展2022年中期业绩PPT 0830v1Muska ChiuNo ratings yet

- Peng Plasma Solutions Tables PDFDocument12 pagesPeng Plasma Solutions Tables PDFDanielle WalkerNo ratings yet

- Key Performance Indicators (Kpis) : FormulaeDocument4 pagesKey Performance Indicators (Kpis) : FormulaeAfshan AhmedNo ratings yet

- Analisa Revenue Cabang & Depo SBY - Ytd 2021Document52 pagesAnalisa Revenue Cabang & Depo SBY - Ytd 2021sholehudinNo ratings yet

- Investor Presentation 30.09.2023Document30 pagesInvestor Presentation 30.09.2023amitsbhatiNo ratings yet

- Math Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesFrom EverandMath Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesRating: 5 out of 5 stars5/5 (3)

- Del Rosario-Igtiben V RepublicDocument1 pageDel Rosario-Igtiben V RepublicGel TolentinoNo ratings yet

- Review - Phippine Arch Post WarDocument34 pagesReview - Phippine Arch Post WariloilocityNo ratings yet

- 16+ Zip Oyster Photocard Terms and ConditionsDocument9 pages16+ Zip Oyster Photocard Terms and ConditionsTTMo1No ratings yet

- Excerpt From The Mystery of Marriage New Rome Press PDFDocument16 pagesExcerpt From The Mystery of Marriage New Rome Press PDFSancta Maria ServusNo ratings yet

- A Theoretical Study of The Constitutional Amendment Process of BangladeshDocument58 pagesA Theoretical Study of The Constitutional Amendment Process of BangladeshMohammad Safirul HasanNo ratings yet

- Apwh Wwi & Wwii WebquestDocument4 pagesApwh Wwi & Wwii WebquestNahom musieNo ratings yet

- No Dues CertificateDocument2 pagesNo Dues CertificateSatyajit BanerjeeNo ratings yet

- Commercial Cards Add A Cardholder FormDocument3 pagesCommercial Cards Add A Cardholder FormsureNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument4 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancepavans25No ratings yet

- Model Consortium Agreement For APPROVALDocument34 pagesModel Consortium Agreement For APPROVALSoiab KhanNo ratings yet

- A Spy Among FriendsDocument11 pagesA Spy Among Friendselmraksi30No ratings yet

- Right Wing TerrorismDocument28 pagesRight Wing TerrorismPúblico DiarioNo ratings yet

- Letter From SMEIA To British PMDocument4 pagesLetter From SMEIA To British PMpandersonpllcNo ratings yet

- 409-Prohibiting Harassment Intimidation or Bullying Cyberbullying Sexting Sexual Harassment StudentsDocument8 pages409-Prohibiting Harassment Intimidation or Bullying Cyberbullying Sexting Sexual Harassment Studentsapi-273340621No ratings yet

- Rizzo v. Goode, 423 U.S. 362 (1976)Document19 pagesRizzo v. Goode, 423 U.S. 362 (1976)Scribd Government DocsNo ratings yet

- With Romulad Twardowski Prize: Warsaw 15 - 17 November 2019Document2 pagesWith Romulad Twardowski Prize: Warsaw 15 - 17 November 2019Eka KurniawanNo ratings yet

- PFRS 3 Business CombinationDocument3 pagesPFRS 3 Business CombinationRay Allen UyNo ratings yet

- Evolution of Hotel Management Agreements and Rise of Alternative AgreementsDocument14 pagesEvolution of Hotel Management Agreements and Rise of Alternative AgreementsSharif Fayiz AbushaikhaNo ratings yet

- Third Party Certification of ServingDocument4 pagesThird Party Certification of ServingBenNo ratings yet

- 01 Internal Auditing Technique Rev. 05 12 09 2018Document40 pages01 Internal Auditing Technique Rev. 05 12 09 2018Syed Maroof AliNo ratings yet

- Civil Advance Hearing Petition Model 26th November2008Document6 pagesCivil Advance Hearing Petition Model 26th November2008lakshmi100% (2)

- Manitowoc 4600 S4 Parts Manual PDFDocument108 pagesManitowoc 4600 S4 Parts Manual PDFnamduong36850% (2)

- 48V DC - DC Converter - Mild Hybrid DC - DC Converter - EatonDocument3 pages48V DC - DC Converter - Mild Hybrid DC - DC Converter - EatonShubham KaklijNo ratings yet

- DBP VS CaDocument55 pagesDBP VS CasamanthaNo ratings yet

- Arcelor MittalDocument4 pagesArcelor Mittalnispo100% (1)

- HSE Policy Statement, SchlumbergerDocument1 pageHSE Policy Statement, SchlumbergerProf C.S.PurushothamanNo ratings yet

- 10 Overseas Bank Vs CA & Tapia PDFDocument10 pages10 Overseas Bank Vs CA & Tapia PDFNicoleAngeliqueNo ratings yet

- Revision Guide For AMD Athlon 64 and AMD Opteron Processors: Publication # Revision: Issue DateDocument85 pagesRevision Guide For AMD Athlon 64 and AMD Opteron Processors: Publication # Revision: Issue DateSajith Ranjeewa SenevirathneNo ratings yet

- 20 ObliconDocument3 pages20 ObliconQuiqui100% (2)

- Digest - Arigo Vs SwiftDocument2 pagesDigest - Arigo Vs SwiftPing KyNo ratings yet