You might also like

- Practical Solutions To Global Business NegotiationsDocument31 pagesPractical Solutions To Global Business NegotiationsBusiness Expert Press25% (4)

- Building A Marketing Plan: A Complete GuideDocument20 pagesBuilding A Marketing Plan: A Complete GuideBusiness Expert Press75% (12)

- Managerial Economics: Concepts and PrinciplesDocument7 pagesManagerial Economics: Concepts and PrinciplesBusiness Expert Press75% (4)

- Basic Sales & Marketing Training - FariazDocument62 pagesBasic Sales & Marketing Training - FariazFariaz Morshed ChowdhuryNo ratings yet

- Strategic Marketing Planning For The Small To Medium-Sized BusinessDocument30 pagesStrategic Marketing Planning For The Small To Medium-Sized BusinessBusiness Expert Press90% (21)

- Understanding The Family BusinessDocument20 pagesUnderstanding The Family BusinessBusiness Expert Press100% (7)

- Handbook Customer Satisfaction Loyalty Measurement 3 Ch2Document8 pagesHandbook Customer Satisfaction Loyalty Measurement 3 Ch2meromikhaNo ratings yet

- Cross-Cultural Management: Veronica VeloDocument26 pagesCross-Cultural Management: Veronica VeloBusiness Expert Press88% (8)

- A Stakeholder Approach To Issues ManagementDocument18 pagesA Stakeholder Approach To Issues ManagementBusiness Expert PressNo ratings yet

- Top Market Strategy: Applying The 80/20 RuleDocument15 pagesTop Market Strategy: Applying The 80/20 RuleBusiness Expert Press100% (1)

- The Five Golden Rules of NegotiationDocument18 pagesThe Five Golden Rules of NegotiationBusiness Expert Press100% (1)

- Instructor Manual For Matching Supply With Demand 2eDocument13 pagesInstructor Manual For Matching Supply With Demand 2eKavin Ur Frnd50% (2)

- Korean Air Ebs Case StudyDocument5 pagesKorean Air Ebs Case StudykkkashNo ratings yet

- Accenture ECommerce POVDocument21 pagesAccenture ECommerce POVChristine Kariuki0% (1)

- Retail ManagementDocument31 pagesRetail ManagementSushmita BarlaNo ratings yet

- Assigned Topic IN ELECT303 M ": AnufacturerDocument20 pagesAssigned Topic IN ELECT303 M ": Anufacturermary ann angeline marinayNo ratings yet

- Lecture 2 (B) - The Customer Journey (2020)Document21 pagesLecture 2 (B) - The Customer Journey (2020)John SmithNo ratings yet

- Managing Customer Experience: Khalid Bin Muhammad Institute of Business ManagementDocument27 pagesManaging Customer Experience: Khalid Bin Muhammad Institute of Business ManagementMubaraka QuaidNo ratings yet

- Customer Interaction ManagementDocument4 pagesCustomer Interaction ManagementAnkush AmbardarNo ratings yet

- Sales & Marketing Plan - CompletedDocument20 pagesSales & Marketing Plan - CompletedAna Nurul LailaNo ratings yet

- Chapter 10 - Price - The Online ValueDocument25 pagesChapter 10 - Price - The Online ValueUmang SaraogiNo ratings yet

- Customer DelightDocument4 pagesCustomer DelightSuhail KhanNo ratings yet

- Services Blueprinting - 10Document10 pagesServices Blueprinting - 10Vinay KalraNo ratings yet

- 4 Strategies To Help Improve Your Customer Service StandardsDocument5 pages4 Strategies To Help Improve Your Customer Service StandardssNo ratings yet

- Seven Steps To Exceptional Customer Service: Optimal Connections, LLCDocument11 pagesSeven Steps To Exceptional Customer Service: Optimal Connections, LLCGnana SekaranNo ratings yet

- Evolution of E-Commerce: An Asian Perspective Challenges of Today and Tomorrow!Document4 pagesEvolution of E-Commerce: An Asian Perspective Challenges of Today and Tomorrow!Radanu1No ratings yet

- Customer-Driven Online Engagement: Transitioning Into A BlueconomyDocument18 pagesCustomer-Driven Online Engagement: Transitioning Into A BlueconomyworkitrichmondNo ratings yet

- Customer Relationship ManagementDocument2 pagesCustomer Relationship ManagementDreamtech Press100% (1)

- Growth Marketers Guide To Customer Engagement AutomationDocument44 pagesGrowth Marketers Guide To Customer Engagement AutomationThanh Phuong NguyenNo ratings yet

- Sales Promotion PlanDocument10 pagesSales Promotion PlanAnjenetteCoronelBarraNo ratings yet

- Sample Company Profile For Cleaning Supplies Business PDFDocument18 pagesSample Company Profile For Cleaning Supplies Business PDFY.P SuastikaNo ratings yet

- STP Market Segmentation Targeting PositioningDocument33 pagesSTP Market Segmentation Targeting PositioningMrugesh Pawar100% (1)

- Name: Index No.: Course - Advanced Diploma in Company Administration and Secretarial Proficiency Module - Customer Care ManagementDocument12 pagesName: Index No.: Course - Advanced Diploma in Company Administration and Secretarial Proficiency Module - Customer Care ManagementRizwan AniseNo ratings yet

- Business Plan 4000 Chinese Tea HouseDocument18 pagesBusiness Plan 4000 Chinese Tea HouseLu XiyunNo ratings yet

- Onny Oktami Samosir 歐霓: 05218224 International Master Business Administration NkfustDocument19 pagesOnny Oktami Samosir 歐霓: 05218224 International Master Business Administration NkfustDiah Novita A PNo ratings yet

- Revenue Management of Food and Beverages Services Group 7 ReportingDocument29 pagesRevenue Management of Food and Beverages Services Group 7 ReportingAnthony Flores100% (1)

- Chapter2-Building and Sustaining Relationships in Gomez ElaizaDocument37 pagesChapter2-Building and Sustaining Relationships in Gomez ElaizaSteph MendiolaNo ratings yet

- HRMDocument24 pagesHRMHetvi GadaNo ratings yet

- Business Plan of A RestaurantDocument24 pagesBusiness Plan of A RestaurantManoranjan Kumar MahtoNo ratings yet

- Customer ExperienceDocument9 pagesCustomer ExperienceRahul GargNo ratings yet

- Star BucksDocument20 pagesStar BucksgeonecideNo ratings yet

- Type The Document TitleDocument15 pagesType The Document TitleAaron Coelho100% (2)

- SOP PresentationDocument20 pagesSOP PresentationventiNo ratings yet

- Business StrategyDocument14 pagesBusiness StrategyDeepak GidwaniNo ratings yet

- Sales and MarketingDocument19 pagesSales and Marketingamar keyzNo ratings yet

- CRM NotesDocument36 pagesCRM NotesJai JohnNo ratings yet

- Title-Gift Shop 2. Aims and ObjectivesDocument8 pagesTitle-Gift Shop 2. Aims and ObjectivesSalman RazaNo ratings yet

- Digital Marketing Finalll-CompressedDocument23 pagesDigital Marketing Finalll-CompressedMayar AlFawiNo ratings yet

- Final Project Performance EnhancementDocument55 pagesFinal Project Performance EnhancementNikhil ShrivastavaNo ratings yet

- Content Marketing: Cheat SheetDocument1 pageContent Marketing: Cheat SheetHarryNo ratings yet

- Customer Relations in BusinessDocument13 pagesCustomer Relations in BusinessmikeNo ratings yet

- Restaurant Inventory: Restaurant Key Product Usage ReportDocument2 pagesRestaurant Inventory: Restaurant Key Product Usage ReportMartin CTNo ratings yet

- Upserve 1 PDFDocument39 pagesUpserve 1 PDFCarlos DungcaNo ratings yet

- How To Write A Business Proposal That Drives Action - GrammarlyDocument12 pagesHow To Write A Business Proposal That Drives Action - GrammarlyIbitoye IdowuNo ratings yet

- Bawai's Group of RestaurantDocument14 pagesBawai's Group of RestaurantMarc Jason Cruz Delomen100% (1)

- The Robert Donato Approach to Enhancing Customer Service and Cultivating RelationshipsFrom EverandThe Robert Donato Approach to Enhancing Customer Service and Cultivating RelationshipsNo ratings yet

- 111.perfect Franchise MB Presentation Eng Forum 3Document51 pages111.perfect Franchise MB Presentation Eng Forum 3TanitaNo ratings yet

- Forrester - Retail Revenue ManagementDocument20 pagesForrester - Retail Revenue ManagementPaul DeleuzeNo ratings yet

- EMC Customer Support GuideDocument26 pagesEMC Customer Support GuideTrydious MaximusNo ratings yet

- Event Manager 1: Job SummaryDocument10 pagesEvent Manager 1: Job Summaryvivek sharmaNo ratings yet

- Retail MGTDocument29 pagesRetail MGTKasiraman RamanujamNo ratings yet

- Food & Beverages Management Assignment Amity UniversityDocument15 pagesFood & Beverages Management Assignment Amity UniversityArvind Dawar100% (1)

- Segmentation Is at The Heart of Marketing Strategy'Document3 pagesSegmentation Is at The Heart of Marketing Strategy'Shalini RastogiNo ratings yet

- Service Gap ModelDocument11 pagesService Gap ModelSrinu ReddyNo ratings yet

- Service Quality in Marketing Hotels & ResortsDocument8 pagesService Quality in Marketing Hotels & ResortsIFa SHaNo ratings yet

- File1pages From CHAPTER 8 - FOOD AND BEVERAGE FUNCTION PLANNINGDocument4 pagesFile1pages From CHAPTER 8 - FOOD AND BEVERAGE FUNCTION PLANNINGTeddy KrisdiyantoNo ratings yet

- Marketing Tactics (How We Will Target Audience)Document2 pagesMarketing Tactics (How We Will Target Audience)Madiha ShoukatNo ratings yet

- The E-Marketing Plan: Erina Widianti Florine Berlian Hasriani Puspitasari Maurent Chandra Yola ArtameviaDocument15 pagesThe E-Marketing Plan: Erina Widianti Florine Berlian Hasriani Puspitasari Maurent Chandra Yola ArtameviaVallen Chandra100% (1)

- Online Customer Engagement ManagementDocument12 pagesOnline Customer Engagement ManagementEric PrenenNo ratings yet

- Strategic Cost AnalysisDocument24 pagesStrategic Cost AnalysisBusiness Expert Press100% (10)

- Working With Economic Indicators: Interpretation and SourcesDocument9 pagesWorking With Economic Indicators: Interpretation and SourcesBusiness Expert Press0% (1)

- Managing Commodity Price Risk: A Supply Chain PerspectiveDocument9 pagesManaging Commodity Price Risk: A Supply Chain PerspectiveBusiness Expert Press50% (2)

- Leading and Managing The Lean Management ProcessDocument14 pagesLeading and Managing The Lean Management ProcessBusiness Expert PressNo ratings yet

- Successful Cross-Cultural Management: A Guide For International ManagersDocument19 pagesSuccessful Cross-Cultural Management: A Guide For International ManagersBusiness Expert Press100% (13)

- Conversations About Job Performance: A Communication Perspective On The Appraisal ProcessDocument20 pagesConversations About Job Performance: A Communication Perspective On The Appraisal ProcessBusiness Expert PressNo ratings yet

- Successful Organizational Transformation: The Five Critical ElementsDocument8 pagesSuccessful Organizational Transformation: The Five Critical ElementsBusiness Expert Press75% (4)

- Supply Chain Information TechnologyDocument23 pagesSupply Chain Information TechnologyBusiness Expert Press100% (22)

- Setting Performance TargetsDocument12 pagesSetting Performance TargetsBusiness Expert Press100% (2)

- The Inscrutable Shopper: Consumer Resistance in RetailDocument17 pagesThe Inscrutable Shopper: Consumer Resistance in RetailBusiness Expert PressNo ratings yet

- Supply Chain Risk Management: Tools For AnalysisDocument11 pagesSupply Chain Risk Management: Tools For AnalysisBusiness Expert Press33% (3)

- Tracing The Roots of Globalization and Business PrinciplesDocument36 pagesTracing The Roots of Globalization and Business PrinciplesBusiness Expert PressNo ratings yet

- Better Business Decisions Using Cost ModelingDocument17 pagesBetter Business Decisions Using Cost ModelingBusiness Expert Press100% (1)

- The Family in Business: The Dynamics of The Family Owned FirmDocument25 pagesThe Family in Business: The Dynamics of The Family Owned FirmBusiness Expert Press50% (2)

- Working With Sample Data: Exploration and InferenceDocument16 pagesWorking With Sample Data: Exploration and InferenceBusiness Expert PressNo ratings yet

- Top Management Teams: How To Be Effective Inside and Outside The BoardroomDocument12 pagesTop Management Teams: How To Be Effective Inside and Outside The BoardroomBusiness Expert Press100% (1)

- Business Applications of Multiple RegressionDocument48 pagesBusiness Applications of Multiple RegressionBusiness Expert Press50% (4)

- Designing The Networked OrganizationDocument16 pagesDesigning The Networked OrganizationBusiness Expert Press0% (1)

- Design, Analysis, and Optimization of Supply Chains: A System Dynamics ApproachDocument21 pagesDesign, Analysis, and Optimization of Supply Chains: A System Dynamics ApproachBusiness Expert Press100% (1)

- Effective Financial Management: The Cornerstone For SuccessDocument17 pagesEffective Financial Management: The Cornerstone For SuccessBusiness Expert PressNo ratings yet

- Revenue Management: A Path To Increased ProfitsDocument13 pagesRevenue Management: A Path To Increased ProfitsBusiness Expert Press100% (2)

- Chopra Meindl SCM-5-10Document6 pagesChopra Meindl SCM-5-10SalmanNo ratings yet

- Chapter 11 PDFDocument3 pagesChapter 11 PDFGajanan Shirke AuthorNo ratings yet

- What Is Oracle Revenue Management CloudDocument4 pagesWhat Is Oracle Revenue Management CloudSriram KalidossNo ratings yet

- Practice Test 1: ListeningDocument25 pagesPractice Test 1: ListeningHoàng Thanh TâmNo ratings yet

- Module 5 STRATEGY AND THE MASTER BUDGETDocument20 pagesModule 5 STRATEGY AND THE MASTER BUDGETitsdaloveshot naNANAnanaNo ratings yet

- Revenue ManagementDocument15 pagesRevenue ManagementShilpy YadavNo ratings yet

- D. Shift Work To Slack Periods: A. ThroughputDocument3 pagesD. Shift Work To Slack Periods: A. ThroughputTk KimNo ratings yet

- Oracle Communication StrategyDocument42 pagesOracle Communication Strategyravi.janakiraman9693100% (1)

- Data Sheet SAP Hybris Billing enDocument2 pagesData Sheet SAP Hybris Billing enSam KolNo ratings yet

- Summarized ReviewerDocument13 pagesSummarized Reviewermalen zubietaNo ratings yet

- HW 15-2 Task Budget Prep MCQ StudDocument5 pagesHW 15-2 Task Budget Prep MCQ StudКсения НиколоваNo ratings yet

- Day 3 BusfinDocument24 pagesDay 3 BusfinAlexa SalvadorNo ratings yet

- An Overview of Revenue ManagementDocument22 pagesAn Overview of Revenue ManagementThefoodiesway100% (1)

- Sales MeetingDocument8 pagesSales Meetingapi-401048604No ratings yet

- Real Earnings Management and Firm Value: Examination of Costs of Real Earnings ManagementDocument23 pagesReal Earnings Management and Firm Value: Examination of Costs of Real Earnings ManagementatikaNo ratings yet

- M9116 Case Study REVENUE RESIT PDFDocument4 pagesM9116 Case Study REVENUE RESIT PDFMohammedNo ratings yet

- Service MarketingDocument24 pagesService MarketingacspandayNo ratings yet

- Review of Related LiteratureDocument5 pagesReview of Related LiteratureKevin B. Pepito0% (1)

- What's New in R12 For SupplyChain - MOAUG - v2Document82 pagesWhat's New in R12 For SupplyChain - MOAUG - v2oneeb350No ratings yet

- Busfin 6 Budget-PlanDocument16 pagesBusfin 6 Budget-PlanHazel CabreraNo ratings yet

- MODULE 4 Profit Planning - BudgetingDocument30 pagesMODULE 4 Profit Planning - BudgetingNil Justeen GarciaNo ratings yet

- Instructor's ManualDocument13 pagesInstructor's ManualM MNo ratings yet

- Dissertation Topics AviationDocument5 pagesDissertation Topics AviationFindSomeoneToWriteMyPaperCanada100% (1)

- 1z0 1059 DemoDocument5 pages1z0 1059 DemoGideon chrisNo ratings yet

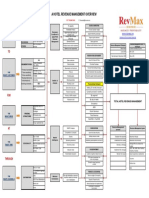

- A Hotel Revenue Management Overview - v4Document1 pageA Hotel Revenue Management Overview - v4Tó GonçalvesNo ratings yet

- Advanced Linear Programming Applications: Multiple ChoiceDocument10 pagesAdvanced Linear Programming Applications: Multiple ChoiceMarwa HassanNo ratings yet

- Breaking Down Willingness-to-Pay in RM: An Overview To PROS Methodology and ApproachDocument12 pagesBreaking Down Willingness-to-Pay in RM: An Overview To PROS Methodology and Approachrichi19975No ratings yet

- Mahrukh Sher Ali 62202 (Assignment 04)Document4 pagesMahrukh Sher Ali 62202 (Assignment 04)wahajNo ratings yet