You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- NPV & Payback Period: Question 2 Ul-Haq and Utley LimitedDocument7 pagesNPV & Payback Period: Question 2 Ul-Haq and Utley LimitedPui YanNo ratings yet

- Marketing Analysis Toolkit - Market Size and MarketDocument14 pagesMarketing Analysis Toolkit - Market Size and MarketMathewNo ratings yet

- Problem 27 1Document2 pagesProblem 27 1CodeSeeker50% (2)

- TOPIC Practice Questions: Question: MayDocument13 pagesTOPIC Practice Questions: Question: MayPines MacapagalNo ratings yet

- Third Merit List of BS CHEMISTRY Morning Fall 2011Document1 pageThird Merit List of BS CHEMISTRY Morning Fall 2011Tariq MinhasNo ratings yet

- The Euro-Asian International Schools and Colleges A Case StudyDocument7 pagesThe Euro-Asian International Schools and Colleges A Case Studynum_1No ratings yet

- CV - Asif Rehan 22.10Document2 pagesCV - Asif Rehan 22.10Tariq MinhasNo ratings yet

- AbstractDocument4 pagesAbstractnum_1No ratings yet

- The Profit and Loss Appropriation AccountDocument4 pagesThe Profit and Loss Appropriation AccountSarthak GuptaNo ratings yet

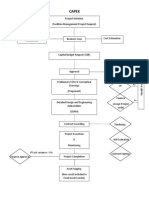

- CAPEXDocument1 pageCAPEXAmal KaNo ratings yet

- CGA Ordinance 2001Document5 pagesCGA Ordinance 2001Saeed Qadir BalochNo ratings yet

- Estimating Skills AACEIDocument27 pagesEstimating Skills AACEISL24980100% (5)

- Executive Summary A. IntroductionDocument6 pagesExecutive Summary A. IntroductionCatherine JoyceNo ratings yet

- EVM Gold CardDocument1 pageEVM Gold Cardwalmart007No ratings yet

- MGRL Corner 4e SM AISE 14Document36 pagesMGRL Corner 4e SM AISE 14vem arcayanNo ratings yet

- Eco Revision 22, 23 FebruaryDocument2 pagesEco Revision 22, 23 FebruarysilNo ratings yet

- Finance Process FlowDocument13 pagesFinance Process FlowHasan NasirNo ratings yet

- Historic St. Mary's City Commission: Audit ReportDocument14 pagesHistoric St. Mary's City Commission: Audit ReportBella N.No ratings yet

- Barangay Budget ExecutionDocument43 pagesBarangay Budget ExecutionNonielyn SabornidoNo ratings yet

- 08 Handout 1Document7 pages08 Handout 1Katelyn SungcangNo ratings yet

- Charmagne E. Eclavea: Manuel S. Enverga University Foundation Inc. (MSEUF) Bachelor of Science in Public AdministrationDocument2 pagesCharmagne E. Eclavea: Manuel S. Enverga University Foundation Inc. (MSEUF) Bachelor of Science in Public AdministrationPrances PelobelloNo ratings yet

- Plan Fiscal A Largo PlazoDocument7 pagesPlan Fiscal A Largo PlazoMetro Puerto RicoNo ratings yet

- Obamacare & GSEs - Key Players Trading HatsDocument51 pagesObamacare & GSEs - Key Players Trading HatsJoshua Rosner100% (4)

- The Savers-Spenders Theory of Fiscal Policy: by N. GDocument10 pagesThe Savers-Spenders Theory of Fiscal Policy: by N. Gmaba424No ratings yet

- Intro To MacroeconimicsDocument128 pagesIntro To MacroeconimicsVikas Kumar0% (1)

- AIS Ch2Document41 pagesAIS Ch2Abdii DhufeeraNo ratings yet

- Forecasts - The TestDocument3 pagesForecasts - The TestPatrykNo ratings yet

- Journal of Economics Development 5Document23 pagesJournal of Economics Development 5emilianocarpaNo ratings yet

- Fundamental and Technical Analysis of Bharti AirtelDocument10 pagesFundamental and Technical Analysis of Bharti AirtelGaurav SharmaNo ratings yet

- Metaphors To Solve Real World ProblemsDocument7 pagesMetaphors To Solve Real World Problemsapi-436793538No ratings yet

- Lecture 5Document39 pagesLecture 5Tiffany TsangNo ratings yet

- 06 Budgeting Theory 40Document4 pages06 Budgeting Theory 40Agnes DizonNo ratings yet

- Financial Management Important QuestionsDocument3 pagesFinancial Management Important QuestionsSaba TaherNo ratings yet

- Euroland Foods SA PDFDocument12 pagesEuroland Foods SA PDFPutu Aditya Pratama0% (1)