You might also like

- Catalogo Escavadeira EC27CDocument433 pagesCatalogo Escavadeira EC27CNilton Junior Kern50% (2)

- SafeNet Financial Services Brochure PDFDocument7 pagesSafeNet Financial Services Brochure PDFBayCreativeNo ratings yet

- FIBAC 2019 - AnnualBenchmarking PDFDocument92 pagesFIBAC 2019 - AnnualBenchmarking PDFNirav ShahNo ratings yet

- 4-Investing in Lending Technology IT Spending in BankingDocument68 pages4-Investing in Lending Technology IT Spending in Bankingarrow.sk7No ratings yet

- Hong Kong: Travel Briefing For Transfer On Work PermitDocument24 pagesHong Kong: Travel Briefing For Transfer On Work PermitrajeshmsitNo ratings yet

- Legislative CasesDocument70 pagesLegislative CasesNiñaNo ratings yet

- Organised Versus Unorganised Retail in IndiaDocument11 pagesOrganised Versus Unorganised Retail in IndiaSharma Sumant0% (1)

- Yale ERC070-HG-8K ManualDocument52 pagesYale ERC070-HG-8K ManualAna GuevaraNo ratings yet

- Nitotile XS GroutDocument33 pagesNitotile XS GroutAhmad SamyNo ratings yet

- E Commerce - AkashDocument17 pagesE Commerce - AkashakashNo ratings yet

- Acme WidgetsDocument5 pagesAcme WidgetsBria DuncombeNo ratings yet

- 3rd April Current Affairs 2023Document12 pages3rd April Current Affairs 2023James Joy PNo ratings yet

- TripDocument1 pageTripEddie JonesNo ratings yet

- 2000-05 The Computer Paper - Ontario EditionDocument143 pages2000-05 The Computer Paper - Ontario Editionthecomputerpaper0% (1)

- Honeywell HIH5031Document8 pagesHoneywell HIH5031odavidson117No ratings yet

- Golden Tax - EBSDocument3 pagesGolden Tax - EBSVaraprasad Reddy KalluruNo ratings yet

- SOP To Be Adopted by FPOsDocument12 pagesSOP To Be Adopted by FPOssampathsamudralaNo ratings yet

- STL Live Projects, Inviting Nominations: Hi Prospective Project StlersDocument2 pagesSTL Live Projects, Inviting Nominations: Hi Prospective Project StlersRahulSamaddarNo ratings yet

- Entregable 2Document80 pagesEntregable 2Eric PattersonNo ratings yet

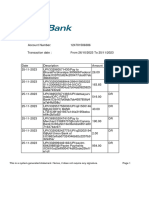

- OpTransactionHistory01 07 2020Document3 pagesOpTransactionHistory01 07 2020sekhar203512No ratings yet

- PolicyDocument4 pagesPolicyShri ShriNo ratings yet

- OC 94A - AddendumDocument1 pageOC 94A - AddendumGaurav YadavNo ratings yet

- Colorado's Homeschool Law Turns TwentyDocument27 pagesColorado's Homeschool Law Turns TwentyEducation Policy CenterNo ratings yet

- Transaction HistoryDocument40 pagesTransaction HistoryShafiq ShahrinNo ratings yet

- Airteltigo Sms Bundle Code - Google SearchDocument1 pageAirteltigo Sms Bundle Code - Google SearchAbigail BrownNo ratings yet

- FIN 401 Final Report BodyDocument9 pagesFIN 401 Final Report Body1711........100% (1)

- Commercial 3Document36 pagesCommercial 3vipl141094No ratings yet

- IPPB General Issurance GuideDocument20 pagesIPPB General Issurance Guideashok rajuNo ratings yet

- Setting Up SMS Sending and Receiving Using A USB GSM Dongle by ZTE - Selective IntellectDocument15 pagesSetting Up SMS Sending and Receiving Using A USB GSM Dongle by ZTE - Selective IntellectlordkurNo ratings yet

- Question 1Document114 pagesQuestion 1OneNo ratings yet

- Rabobank Statement of Facts PDFDocument42 pagesRabobank Statement of Facts PDFZerohedgeNo ratings yet

- Caribbean Utilities Company, Ltd. Caribbean Utilities Company, LTDDocument48 pagesCaribbean Utilities Company, Ltd. Caribbean Utilities Company, LTDHannahNo ratings yet

- Home - Unique Identification Authority of India - Government of India PDFDocument3 pagesHome - Unique Identification Authority of India - Government of India PDFMadhanmohan AnnavaramNo ratings yet

- Sathi A Das 2003Document10 pagesSathi A Das 2003pain2905No ratings yet

- CRD42021275571 2Document5 pagesCRD42021275571 2Carmelo VillafrancaNo ratings yet

- Ticket - Piyush - Shimla To ChanbhaDocument2 pagesTicket - Piyush - Shimla To ChanbhaVijay RudreshNo ratings yet

- How To Ease A Covid-19 Lockdown - Fumbling For The Exit Strategy - The EconomistDocument4 pagesHow To Ease A Covid-19 Lockdown - Fumbling For The Exit Strategy - The EconomistAnonymous TDI8qdYNo ratings yet

- Sebi Circular MF Am CosDocument2 pagesSebi Circular MF Am Cos_lucky_No ratings yet

- 00 - About Elliptic IntegralsDocument2 pages00 - About Elliptic Integralsapi-238839028No ratings yet

- L-15. Start UpDocument12 pagesL-15. Start UpShubham BudhlakotiNo ratings yet

- BroadcomDocument3 pagesBroadcomvinothsanNo ratings yet

- Effects of E-Procurement On The Organizational Performance-1052Document22 pagesEffects of E-Procurement On The Organizational Performance-1052KevineNo ratings yet

- Bajaj Tiger CC MITC NewDocument12 pagesBajaj Tiger CC MITC NewMinatiNo ratings yet

- Tech Team JDDocument3 pagesTech Team JDtaposh.barmonNo ratings yet

- An Interim Report ON: Effects of Recession On The Investment Planning of The CustomersDocument19 pagesAn Interim Report ON: Effects of Recession On The Investment Planning of The CustomerskamleshvickyNo ratings yet

- UnlockedDocument29 pagesUnlockedAman SinghNo ratings yet

- 2023 25 11 22 15 26 Statement - 1700930726617Document16 pages2023 25 11 22 15 26 Statement - 1700930726617Vishwanath S MysoreNo ratings yet

- Smart Drive Privatecar Insurance Policy WordingDocument4 pagesSmart Drive Privatecar Insurance Policy WordingManu DevangNo ratings yet

- Articles Magazines Files 09 2016 Lighting Electronics 2 Spreads PDFDocument15 pagesArticles Magazines Files 09 2016 Lighting Electronics 2 Spreads PDFeyadNo ratings yet

- Page 1 / 9Document10 pagesPage 1 / 9Ion CovanjiNo ratings yet

- Hamza 2018 J. Phys. Conf. Ser. 1123 012063Document10 pagesHamza 2018 J. Phys. Conf. Ser. 1123 012063Sanjay singhNo ratings yet

- Your The FPV Store You Deserve Order Has Been Received! - Flotanomers@gmail - Com - GmailDocument2 pagesYour The FPV Store You Deserve Order Has Been Received! - Flotanomers@gmail - Com - Gmailpratham kbNo ratings yet

- User's Manual: GB NL F E D IDocument21 pagesUser's Manual: GB NL F E D IFlorea NicolaeNo ratings yet

- Loan Policy N MimsDocument46 pagesLoan Policy N Mimsnehamittal03No ratings yet

- Force Majeure, Frustration and Impossibility: Smaran Shetty and Pranav BudihalDocument51 pagesForce Majeure, Frustration and Impossibility: Smaran Shetty and Pranav Budihaluma mishraNo ratings yet

- Peter Giese, J. Behrmann (Auth.), P. Giese, J. Behrmann (Eds.) - Active Continental Margins - Present and Past-Springer-Verlag Berlin Heidelberg (1994)Document249 pagesPeter Giese, J. Behrmann (Auth.), P. Giese, J. Behrmann (Eds.) - Active Continental Margins - Present and Past-Springer-Verlag Berlin Heidelberg (1994)KHIRI KHALFNo ratings yet

- TEST EXP-converted - 1Document1 pageTEST EXP-converted - 1subratkumarhotaskhNo ratings yet

- How To Duplicated LDocument2 pagesHow To Duplicated LShinchan NoharaNo ratings yet

- Exclusive XAT-2023 (GK Compendium)Document48 pagesExclusive XAT-2023 (GK Compendium)Arpit SinghNo ratings yet

- Most Important Terms and ConditionsDocument7 pagesMost Important Terms and ConditionsSignupNo ratings yet

- Citi Rewards Card ChargesDocument7 pagesCiti Rewards Card ChargesLokesh SuranaNo ratings yet

- Project On Mahindra BoleroDocument35 pagesProject On Mahindra BoleroViPul75% (8)

- WellaPlex Technical 2017Document2 pagesWellaPlex Technical 2017Rinita BhattacharyaNo ratings yet

- Lecture 1 Electrolyte ImbalanceDocument15 pagesLecture 1 Electrolyte ImbalanceSajib Chandra RoyNo ratings yet

- Master Data FileDocument58 pagesMaster Data Fileinfo.glcom5161No ratings yet

- Wps For Carbon Steel THK 7.11 GtawDocument1 pageWps For Carbon Steel THK 7.11 GtawAli MoosaviNo ratings yet

- Studies - Number and Algebra P1Document45 pagesStudies - Number and Algebra P1nathan.kimNo ratings yet

- Technical DescriptionDocument2 pagesTechnical Descriptioncocis_alexandru04995No ratings yet

- Nuttall Gear CatalogDocument275 pagesNuttall Gear Catalogjose huertasNo ratings yet

- Note Hand-Soldering eDocument8 pagesNote Hand-Soldering emicpreampNo ratings yet

- Work Permits New Guideline Amendments 2021 23.11.2021Document7 pagesWork Permits New Guideline Amendments 2021 23.11.2021Sabrina BrathwaiteNo ratings yet

- Preliminary Examination The Contemporary WorldDocument2 pagesPreliminary Examination The Contemporary WorldJane M100% (1)

- History of Old English GrammarDocument9 pagesHistory of Old English GrammarAla CzerwinskaNo ratings yet

- Bobcat E34 - E35Z Brochure - Adare MachineryDocument8 pagesBobcat E34 - E35Z Brochure - Adare MachineryNERDZONE TVNo ratings yet

- Face Detection and Recognition Using Opencv and PythonDocument3 pagesFace Detection and Recognition Using Opencv and PythonGeo SeptianNo ratings yet

- ADMT Guide: Migrating and Restructuring Active Directory DomainsDocument263 pagesADMT Guide: Migrating and Restructuring Active Directory DomainshtoomaweNo ratings yet

- Sweat Equity SharesDocument8 pagesSweat Equity SharesPratik RankaNo ratings yet

- Technology ForecastingDocument38 pagesTechnology ForecastingSourabh TandonNo ratings yet

- Sinamics g120p Cabinet Catalog d35 en 2018Document246 pagesSinamics g120p Cabinet Catalog d35 en 2018Edgar Lecona MNo ratings yet

- Sidomuncul20190313064235169 1 PDFDocument298 pagesSidomuncul20190313064235169 1 PDFDian AnnisaNo ratings yet

- Types of Intermolecular ForcesDocument34 pagesTypes of Intermolecular ForcesRuschan JaraNo ratings yet

- FM Testbank-Ch18Document9 pagesFM Testbank-Ch18David LarryNo ratings yet

- Annex A - Scope of WorkDocument4 pagesAnnex A - Scope of Workمهيب سعيد الشميريNo ratings yet

- Salwico CS4000 Fire Detection System: Consilium Marine ABDocument38 pagesSalwico CS4000 Fire Detection System: Consilium Marine ABJexean SañoNo ratings yet

- PixiiDocument3 pagesPixiiFoxNo ratings yet

- The Impact of Personnel Behaviour in Clean RoomDocument59 pagesThe Impact of Personnel Behaviour in Clean Roomisrael afolayan mayomiNo ratings yet

- Learning Module - Joints, Taps and SplicesDocument9 pagesLearning Module - Joints, Taps and SplicesCarlo Cartagenas100% (1)

- Characteristics of Trochoids and Their Application To Determining Gear Teeth Fillet ShapesDocument14 pagesCharacteristics of Trochoids and Their Application To Determining Gear Teeth Fillet ShapesJohn FelemegkasNo ratings yet

- Ericsson For Sale From Powerstorm 4SA03071242Document8 pagesEricsson For Sale From Powerstorm 4SA03071242wd3esaNo ratings yet

- The Chulalongkorn Centenary ParkDocument6 pagesThe Chulalongkorn Centenary ParkJack FooNo ratings yet